Who Should Buy Commercial Space in Vashi? Best Fit Buyers, Risks and Ground Reality

Commercial space in Vashi usually makes sense for established self-use professionals, visibility-dependent retailers, trade-linked operators, and selective long-hold investors with strong holding power. It usually does not make sense for undercapitalized buyers, blind yield chasers, or businesses that need giant modern campus-style office setups. In Vashi, the right buyer is decided less by the area’s prestige and more by sector fit, parking reality, building age, tax burden, and whether the space will actually work for your business or tenant.

Vashi is one of the oldest and most mature commercial markets in Navi Mumbai. That maturity is its strength, but it is also the reason buyers need to be careful. This is not a “buy anything in a prime location and it will work” market. It is a selective market. A strong unit in the right belt can perform very well for years. A bad unit in the wrong lane can stay weak, vacant, or capex-heavy even though the pin code sounds impressive.

That is why the real question is not whether Vashi is good. The real question is whether you are the right kind of buyer for Vashi.

For broader local clarity before taking that call, Vashi Commercial Property Guide is worth reading as well.

Who is Vashi commercial space actually a good fit for?

Vashi commercial property is usually a strong fit for buyers who need immediate business utility, can handle a premium entry cost, and understand that one Vashi pocket is not the same as another. It is strongest for self-use buyers who want long-term operational stability, and for businesses that benefit from visibility, station access, or trade connectivity.

Here is the quick answer first:

| Buyer Profile | Best Asset Type | Best Vashi Micro-Market | Suitability |

|---|---|---|---|

| CA, lawyer, consultant, agency, clinic | 300 to 600 sq. ft. office | Sector 17 or selected Sector 19 pockets | Strong fit |

| Tech startup, BPO, branch office, BFSI team | Modern office | Sector 30 or 30A | Strong fit |

| Boutique retail, jewellery, electronics, premium service brand | High-visibility shop | Sector 17 main stretches or strong main-road frontage | Strong but selective fit |

| Agri-trade, logistics, commodity-linked business | Trade office / utility commercial space | APMC belt, Sector 19 | Strong fit |

| Pre-leased conservative investor | Stabilized office with credible tenant | Sector 30 / 30A | Selective fit |

| Large MNC seeking 50,000+ sq. ft. campus-style space | Large integrated IT office | Avoid Vashi, look at Airoli / Mahape style markets | Weak fit |

| Low-ticket investor hoping for quick tenanting | Budget interior shop / gala | Most low-visibility pockets | Weak fit |

What makes Vashi attractive is not just connectivity. It is the fact that the business ecosystem is already active. There is customer movement, office movement, residential catchment, transport connectivity, and commercial memory. Many businesses do not want to wait five years for an emerging node to mature. Vashi solves that problem.

But the same maturity also means high prices, aggressive municipal tax impact on commercial ownership, and a lot of ageing stock. So Vashi suits buyers who want usefulness and permanence, not cheap entry.

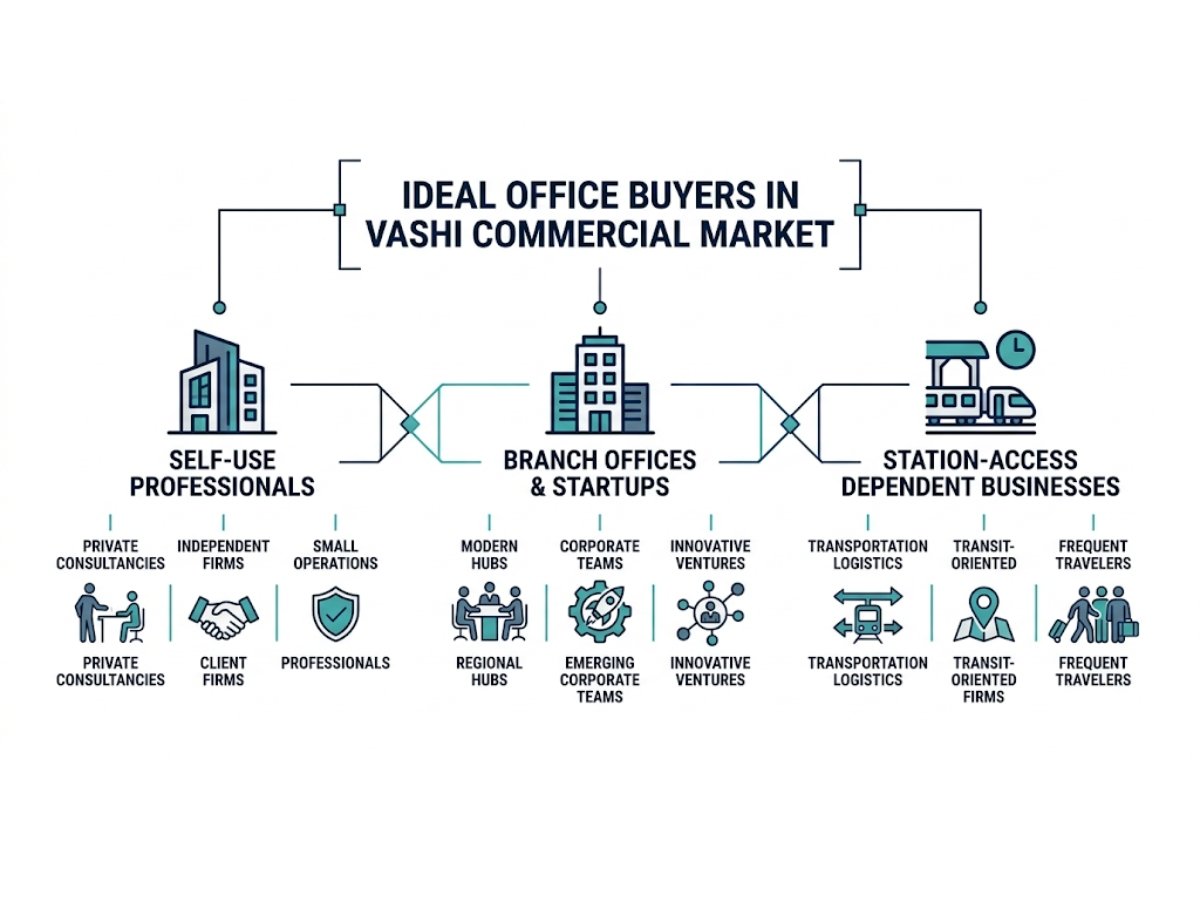

Which type of buyer usually does best with an office in Vashi?

Office buyers do well in Vashi when they need access, familiarity, and a functioning business ecosystem more than they need a giant new-age corporate campus. This is why Vashi continues to work for professional offices, branch offices, service firms, and medium-scale operational setups.

Self-use professionals and service firms

This is one of the strongest buyer categories for Vashi. Chartered accountants, lawyers, insurance offices, consultants, architects, wealth managers, doctors, diagnostic setups, training firms, and agencies often do well here because Vashi gives them a known address with established footfall and easy city access.

For this kind of buyer, ownership can be smarter than leasing if the business is already stable. Why? Because the unit becomes an operational base, not just an investment. You reduce lease uncertainty, protect your fit-out cost, and build long-term location stability.

In practical terms, a 300 to 600 sq. ft. office in the right Vashi building can make much more sense for a serious self-use professional than a larger but weaker office in an immature market.

Companies that need station-linked accessibility, not campus-style space

Sector 30 and 30A are usually better for buyers who want more corporate-style office stock and stronger railway access. This matters for businesses that depend on employee commuting, client meetings, or a more formal commercial environment.

This is where Vashi works for branch offices, BPO-style setups, backend teams, regional headquarters, and firms that need 500 to 2,000 sq. ft. operational space. They are paying for location efficiency and ecosystem maturity, not for giant floor plates or integrated campus infrastructure.

This is also where readers need to be realistic. A company that truly needs massive IT campus-grade infrastructure, very large contiguous plates, or large-scale MNC-style occupancy is usually not a natural Vashi fit. In Navi Mumbai, that kind of requirement pushes naturally toward Airoli or Mahape corridors, not Vashi.

Buyers who value ready business ecosystems over new glass-tower fantasy

Some buyers chase “new building” too blindly. In Vashi, that can be a mistake. A well-located older office in the right belt can still outperform a prettier but less practical space. What matters is the building’s maintenance, access, client comfort, lift quality, parking situation, and whether the space actually suits the business.

That said, older stock comes with risk. If you buy a bare-shell office in an ageing building just because the price looks slightly attractive, you may end up spending heavily on interiors, air-conditioning, façade correction, electrical upgrades, or society repair contributions. In some cases, that extra outflow can change the entire investment logic.

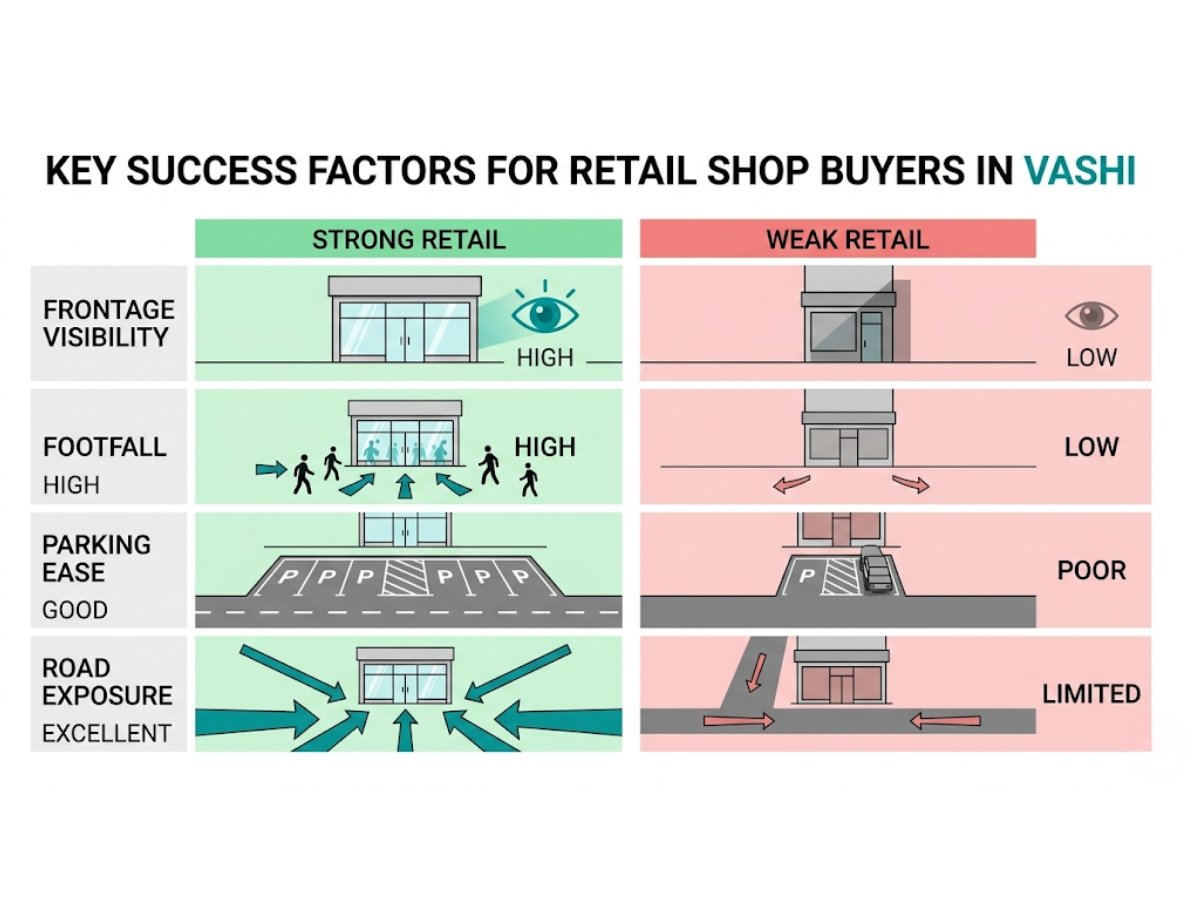

Which type of buyer usually does best with a shop or visible retail unit in Vashi?

Retail buying in Vashi is much harsher than office buying. It can work very well, but only if visibility, frontage, and parking logic are right. Shop buyers are not buying just carpet area. They are buying attention, convenience, repeatability, and street-level conversion.

Businesses that depend on frontage, walk-ins, and repeat local footfall

A strong Vashi shop can work for jewellery, premium electronics, boutique fashion, branded service outlets, cosmetic clinics, speciality food formats, and other businesses where visibility matters. The location itself becomes part of the business model.

This is why good retail frontage in Vashi can command very steep rates. In the stronger stretches of the market, ground-floor main-road visibility is not priced like a normal commercial box. It is priced like an earning surface.

But that only works if the business actually benefits from that frontage. If your customer acquisition model does not depend on walk-ins or street trust, paying a huge premium for visible retail may be a waste.

Buyers who understand that not every “main road” unit is equally valuable

This is where many people go wrong. They hear “Vashi shop,” “main road,” or “prime sector,” and assume the unit will automatically attract a premium tenant or premium customer. That is not how it works on the ground.

In Vashi retail, three shops in the same building can behave very differently. One may face active movement. One may have poor stopping convenience. One may be visually blocked. One may suffer because customers have nowhere to park without stress.

The Sector 17 parking problem is a real decision factor here. High-density commercial movement, traffic congestion, and towing pressure can hurt retail performance if the building has poor parking support. If your customer is likely to arrive by car and cannot stop comfortably, that matters. In some businesses, it matters a lot.

So a budget retail unit in an interior lane or weak flank location is not “cheap entry into Vashi.” It is often an expensive mistake.

Who should buy in Sector 17, who fits the APMC belt, and who belongs in Sector 30 or 30A?

This is the most important local filter in the whole discussion. Vashi is not one commercial market. It is a cluster of very different commercial behaviors.

| Micro-Market | What Usually Works Here | Who It Suits Best | What Buyers Must Watch |

|---|---|---|---|

| Sector 17 | High-street retail, legacy office, mixed-use commercial | Consultants, clinics, boutique retail, client-facing service businesses | Parking stress, ageing buildings, maintenance, exact frontage quality |

| APMC / Sector 19 | Trade office, wholesale-linked utility spaces, logistics support | Transporters, agri-trade firms, commodity operators, supply-chain linked users | Industrial environment, business-type mismatch, utility-first rather than prestige-first appeal |

| Sector 30 / 30A | Corporate office, station-adjacent office use, Grade-A style commercial | Branch offices, startups, BFSI teams, BPOs, formal offices | Ticket size, building quality, rent-to-price ratio, tenant covenant quality |

Sector 17 fit

Sector 17 is one of the most recognized commercial belts in Vashi, but it is not for everybody. It is strongest for client-facing businesses that benefit from a known address, established movement, and proximity to dense surrounding residential catchment.

A consultant, cosmetic clinic, legal office, financial advisory office, or boutique retailer can make sense here if the exact building and access work. What matters is not just the sector name. It is whether the exact unit has the practical qualities that support repeat business.

It is also one of the belts where old-stock friction is very real. You have to assess lifts, façade age, parking, maintenance quality, common areas, and possible repair burden very carefully.

APMC-side fit

The APMC belt works best for businesses that are linked to wholesale flow, trade movement, supply chains, logistics, commodity operations, and transport utility. This is a very different commercial logic from premium high-street or corporate office space.

An agri-logistics firm, grain merchant, transport operator, trade-focused service professional, or wholesale-linked support business may find this belt highly practical. But a premium lifestyle consultancy or a prestige-seeking software business placed here may be fundamentally misaligned.

This is one of the clearest examples of why Vashi has to be read by micro-market, not by brand value.

Sector 30 and 30A fit

Sector 30 and 30A are generally stronger for office buyers who want a more formal commercial environment and better station-linked convenience. Buyers who depend on employee commuting, meetings, and structured office identity often prefer these pockets.

This is where pre-leased office investing can also make more sense, provided the building quality and tenant profile are strong. Still, even here, the buyer has to do proper math. A good-looking office tower is not the same thing as a good investment if entry cost is too high or net yield gets compressed by taxes and holding costs.

You may also want to read Shop vs Office Investment in Vashi if you are still comparing visibility-driven assets with office-led demand.

Which buyers should stay cautious or avoid buying commercial space in Vashi?

Some buyers like the Vashi name for the wrong reasons. That is where mistakes happen.

Small investors chasing brochure yield

This is one of the biggest mismatch categories. A lot of buyers see headline commercial yields and assume Vashi will produce easy rental income. But gross yield and net yield are not the same thing.

Commercial property tax in NMMC is harsh compared to residential property. Maintenance can also be high, especially in older commercial buildings. If your purchase logic depends on thin-margin rental math, Vashi can disappoint you very quickly.

Buyers who underestimate old-stock friction

Many Vashi commercial buildings are old. Some still work well because the location is strong and the building has been maintained properly. Others carry hidden capex pressure.

If you buy old stock without checking structural condition, society repair burden, waterproofing needs, lift modernization, façade deterioration, or major fit-out cost, the actual purchase cost can rise sharply after registration. In legacy stock, a lower purchase price does not always mean a better deal.

Businesses needing large-format modern office layouts

A business that needs huge contiguous floor plates, integrated campus features, large employee facilities, or large-scale IT infrastructure is usually forcing the wrong market if it chooses Vashi.

Vashi is strong for regional, professional, branch, and medium-scale office use. It is not the obvious first choice for giant, campus-style occupiers.

Retail buyers assuming every unit will get premium tenants

This is another common mistake. In Vashi retail, visibility quality is not equal across buildings, roads, or floors. A weaker retail unit can remain vacant or attract only lower-quality tenant demand.

A budget buyer hoping to buy a cheap retail gala and get premium rent only because the address says Vashi is taking a real risk.

A reality check on tax before you buy

This is one of the most ignored parts of Vashi commercial investing, and it can completely change the numbers.

NMMC commercial property tax is applied at 68.33% of the property’s rateable value, while residential property is taxed at a much lower rate. In simple terms, rateable value is based on expected annual rent minus a statutory deduction. That means commercial owners cannot casually use gross rent to calculate returns.

Example of why this matters

Suppose a commercial unit is expected to earn ₹1,00,000 per month in rent.

- Annual rent = ₹12,00,000

- Less 10% statutory deduction = ₹10,80,000 rateable value

- Commercial tax at 68.33% of rateable value = roughly ₹7,37,964 annually

That tax impact is serious. Even if the final number varies depending on assessment details, the basic lesson is clear: net yield math in Vashi can look much weaker after municipal reality enters the picture.

This is why Vashi is usually better for buyers who want strategic self-use stability, or for investors who are financially strong enough to absorb municipal friction, not for beginners trying to squeeze easy passive yield from a thin-margin purchase.

Is Vashi better for self-use buyers or investors?

In most cases, Vashi is a stronger buy for self-use than for pure investment.

When self-use wins

Self-use wins when the business is already stable and expects to remain in the area for years. In that situation, buying can reduce lease instability, protect customized interiors, strengthen business identity, and anchor the operation in a proven commercial belt.

This matters even more in a market like Vashi where good units are not cheap and shifting later can be costly. If the business fits the location well, ownership can create long-term operational stability.

When investment works

Investment works best in Vashi for selective buyers, not casual buyers. The stronger investor profile here is usually a conservative HNI or experienced commercial buyer who is not depending on immediate fast appreciation or easy low-vacancy income.

Pre-leased, better-quality office assets in stronger office pockets may suit this kind of investor, especially if the tenant is credible and the building is operationally sound. But the investor still needs to evaluate taxes, maintenance, age, lease terms, and exit liquidity carefully.

When leasing first may be smarter than buying

For a newer business, or for a business still testing the Vashi market, leasing can be the smarter first move. That is because Vashi’s entry barrier is high, and commercial assets are not as liquid as residential flats.

If you are unsure whether the business will scale, or whether the exact micro-market will actually work for you, leasing first can reduce the risk of locking capital into the wrong format.

What kind of budget, holding power, and risk appetite does a Vashi buyer need?

A Vashi buyer needs more than just purchase capital. They need buffer capital.

As of early 2026, even a modest respectable office in a decent Vashi commercial setting can require a significant outlay. In practical terms, the buyer should not think only about the negotiated price. They should think about the full acquisition stack.

That usually includes:

- Stamp duty and registration costs

- CIDCO transfer-related costs where applicable on leasehold assets

- NMMC transfer or name-change charges

- Society NOC or internal transfer costs where applicable

- Interior corrections or full fit-out

- Vacancy buffer

- Repair reserve for old-stock surprises

In many cases, the real cost of acquisition can feel 10% to 15% higher than the headline deal value once all local frictions are included.

Buyers also need to understand that stamp duty valuation can differ based on building age and floor position. In Maharashtra, valuation mechanisms can factor in things like floor rise premium and depreciation, so not every office or shop gets taxed the same way in practice.

A good Vashi commercial buyer is not someone who can barely close the transaction. It is someone who can still breathe after the transaction.

What should a serious buyer verify before buying commercial space in Vashi?

In Vashi, due diligence is not a formality. It is part of the buying decision itself.

Use this checklist before you move ahead:

Vashi commercial due diligence checklist

- Verify the full ownership chain and past transfer history

- Confirm CIDCO transfer documentation is in order where the asset is leasehold

- Check whether any unearned income or transfer-related liability may arise

- Take zero-balance NMMC property tax proof from the seller

- Check society dues, sinking fund dues, repair burden, and NOC requirements

- For older buildings, review the latest structural audit report

- Ask whether the building has faced major waterproofing, lift, façade, or structural issues

- Confirm carpet area, sanctioned use, and exact commercial classification

- Check real parking reality, not just brochure parking claims

- Evaluate approach road, stopping ease, loading-unloading practicality where relevant

- For investment buys, verify current tenant quality, security deposit, escalation terms, and actual payment history

- For under-construction or newly registered commercial projects, use MahaRERA appropriately; for old resale stock, do not assume MahaRERA gives protection

One more important local point needs to be understood properly.

Commercial buyers should not assume the freehold benefit applies automatically

There has been a lot of market buzz around CIDCO’s freehold conversion policy. But the important distinction is that the recent conversion push is understood primarily in the residential context. Commercial buyers should not casually assume they are free from leasehold transfer rules, transfer fees, or possible future CIDCO-linked friction.

That assumption can damage the purchase math badly. If the commercial asset is under leasehold structure, the buyer must verify the current transfer process and liabilities carefully before closing the deal.

What are realistic buyer examples in Vashi, and which option suits each one?

Sometimes the easiest way to understand buyer fit is through real-style scenarios.

Example 1: The medical consultant

A specialized doctor wants a trusted, visible, client-facing setup close to dense residential catchment and known commercial movement. This buyer is usually a strong fit for a ground or first-floor commercial unit in the right part of Sector 17, provided parking and building condition are acceptable.

Example 2: The CA, lawyer, or advisory office

A professional services firm wants a permanent address, moderate office size, and client familiarity. A 300 to 600 sq. ft. office in Sector 17 or a suitable practical commercial building in a relevant belt can be a strong self-use buy.

Example 3: The agri-logistics or commodity-linked operator

This buyer needs proximity to actual trade movement, not corporate prestige. A utility-first office or trade-linked commercial base in the APMC belt makes far more sense than paying a premium for a polished but operationally irrelevant corporate tower.

Example 4: The conservative HNI investor

This buyer is not chasing aggressive appreciation. They want wealth preservation, a stable tenant, and fewer operational headaches. A selective pre-leased office in a better commercial building in Sector 30 or 30A may work, but only if the lease, tenant, maintenance, and net yield math are all strong.

Example 5: The low-ticket speculative investor

This buyer has a tight budget, hopes to enter Vashi retail cheaply, and expects easy rental income. This is usually a dangerous mismatch. In many cases, that budget only reaches weaker interior units with poor visibility and weak tenant demand. The risk of chronic vacancy is real.

So, who should actually buy commercial space in Vashi?

Commercial space in Vashi should usually be bought by people who already know why they need Vashi.

That includes established professionals who want to own their operating office, selective retailers whose business depends on premium frontage, trade-linked operators who need the right ecosystem, and financially strong investors who understand net yield compression, building-age risk, and holding-period discipline.

It usually should not be bought by beginners who are relying on fast rent, thin-margin returns, or the belief that any commercial property in an established node is automatically safe.

In simple words, Vashi is not a beginner’s shortcut market. It is a serious-use market.

Conclusion

Vashi commercial space is a strong buy only when the buyer profile, asset type, and micro-market are aligned properly. It works best for established self-use professionals, selective retailers, trade-linked operators, and experienced long-hold investors who can absorb tax, maintenance, and vacancy reality. It works poorly for speculative low-budget buyers, blind yield seekers, and businesses forcing the wrong use into the wrong sector.

So before asking whether Vashi is good, ask a harder and more useful question: Does this exact Vashi space fit my business model, budget, holding power, and operating reality? If the answer is yes, Vashi can still be one of Navi Mumbai’s most durable commercial buys. If not, the same market can become a very expensive lesson.

FAQs

Frequently Asked Questions