How Station Access, APMC, Infotech Park and Mall Footfall Shape Vashi Property Demand

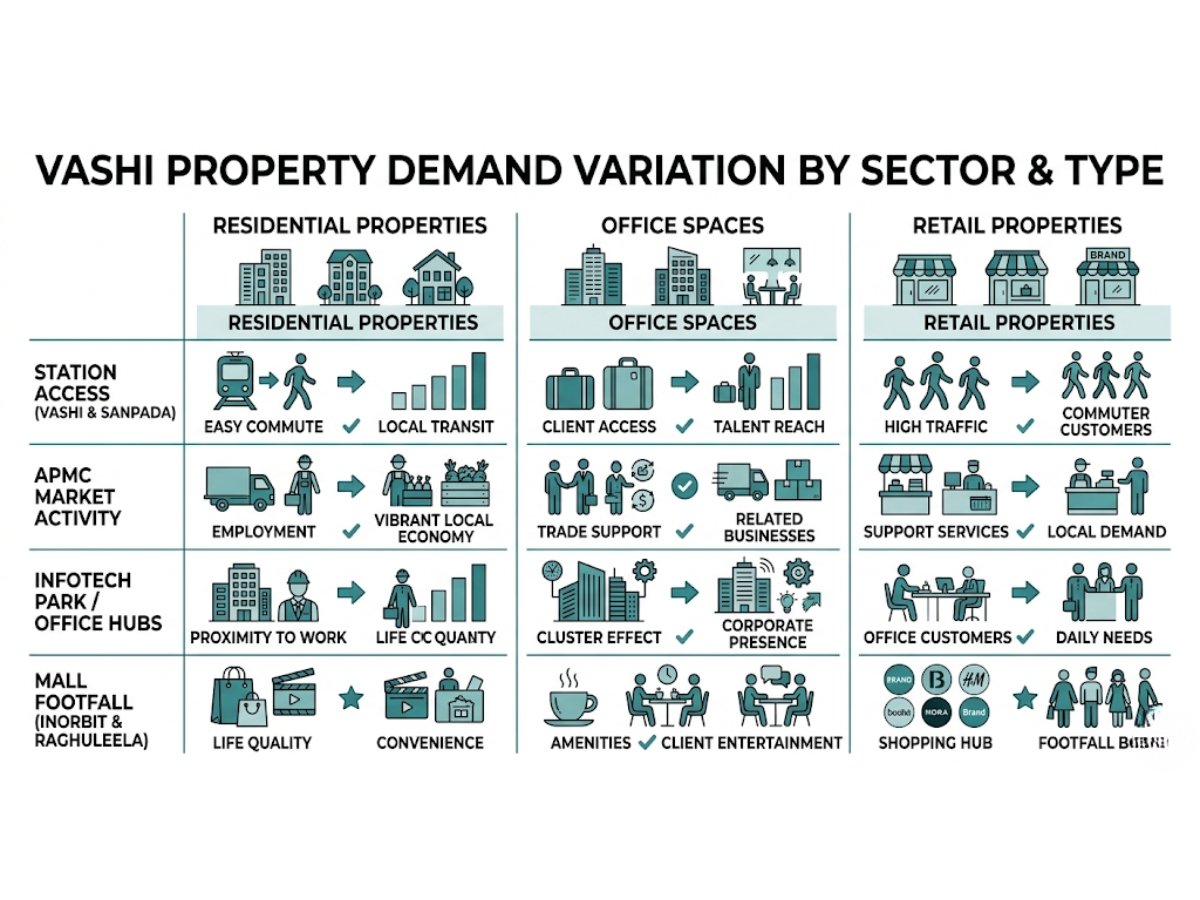

Vashi demand is strong, but it is not uniform. Station access usually supports commuter-led residential and office demand, APMC supports trade and service-linked commercial demand, Infotech Park supports formal office demand, and mall footfall helps selective retail and visibility-based demand. But these drivers do not help every sector, building, or property type equally. In Vashi, the right conclusion depends on what you are buying: a flat, an office, a shop, or a trade-linked commercial asset.

Vashi is one of those Navi Mumbai nodes where the surface story is too simple. People say it is prime, mature, expensive, well-connected. All true. But that still does not tell a buyer what they actually need to know. A family looking for a peaceful home, a landlord chasing stable rent, a small office buyer, and a retail investor will not read the same Vashi map in the same way.

That is exactly why this topic matters. In Vashi, demand is not created by one broad “location advantage.” It is created by different urban engines working in different pockets. The station creates one type of pull. APMC creates another. The office corridor around Infotech Park and Sector 30A creates another. And mall-led footfall creates yet another. Sometimes these engines overlap and push prices higher. Sometimes they create friction that actually hurts the wrong kind of buyer.

To understand how these demand drivers shape the node overall, Vashi Commercial Property Guide is worth reading too

What actually drives Vashi demand, and why the answer changes by sector, building, and property type

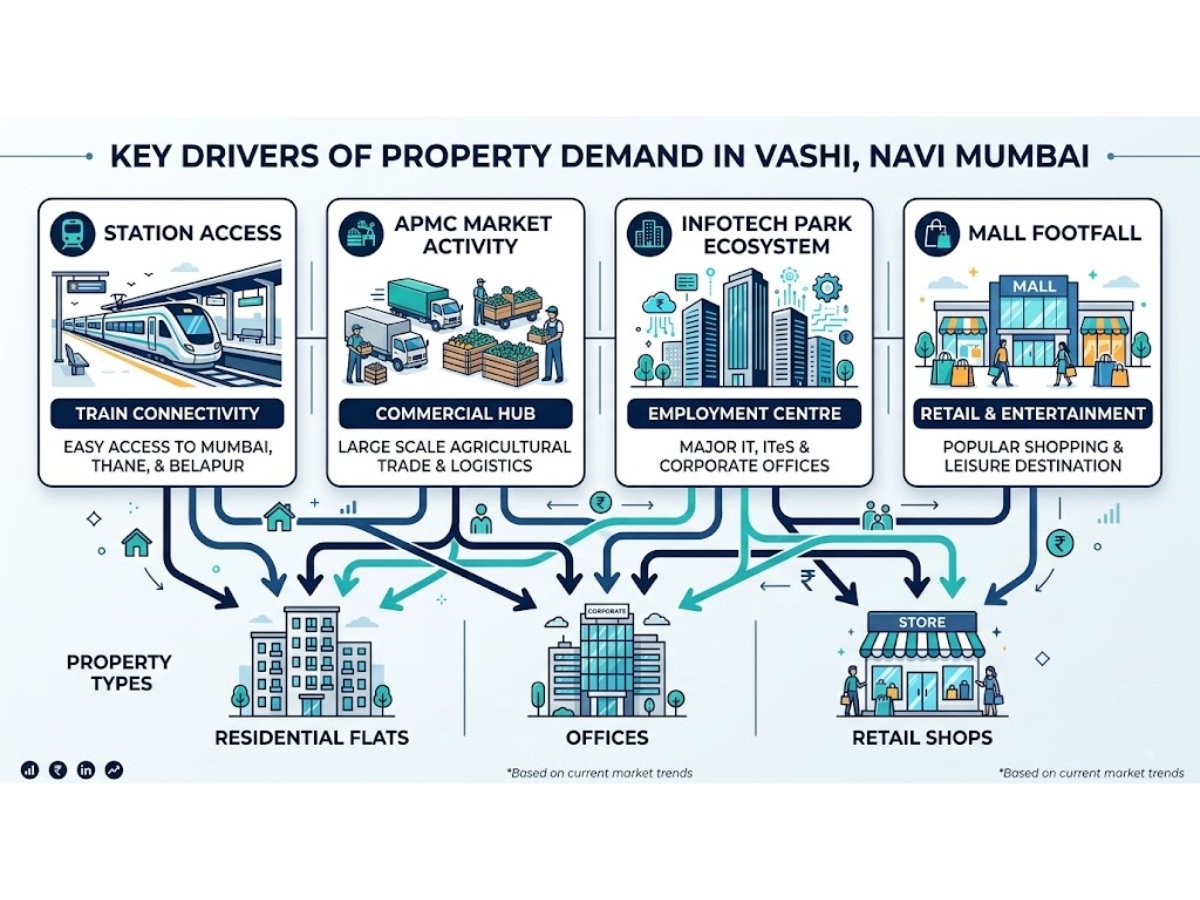

The easiest mistake in Vashi is treating the whole node as one single market. It is not. The practical value of a property depends on what kind of daily movement supports it and what kind of friction comes with that movement.

Some pockets are driven by commuter convenience. Some by wholesale trade and truck movement. Some by office staff mobility and corporate image. Some by weekend retail crowd and visibility. That is why Vashi can show a wide 2025/2026 residential capital band of roughly ₹16,000 to ₹31,450 per sq. ft. depending on sector, building condition, access, and micro-location logic. The same fragmentation is even sharper in commercial real estate, where office rents and shop rents follow very different demand patterns.

| Demand driver | What it mainly supports | Best fit property types | Main caution |

|---|---|---|---|

| Vashi station access | Daily commuter movement, walkability, office usability | Flats for working households, offices, clinics, service businesses | Map distance is not equal to real walkability |

| APMC activity | Trade, transport, storage, labour and support services | Warehousing support, B2B offices, trade-linked shops | Noise, trucks, dust, poor family livability |

| Infotech Park and Grade-A office ecosystem | Corporate occupancy, staff convenience, office absorption | Grade-A offices, strata offices, business suites | Older stock without parking can lose relevance |

| Mall footfall | Retail visibility, food and beverage movement, brand exposure | Shops, showrooms, F&B units | Weekend congestion can hurt residential appeal |

This is the real frame. A property in Vashi does not become strong simply because it is in Vashi. It becomes strong when its use matches the demand engine around it.

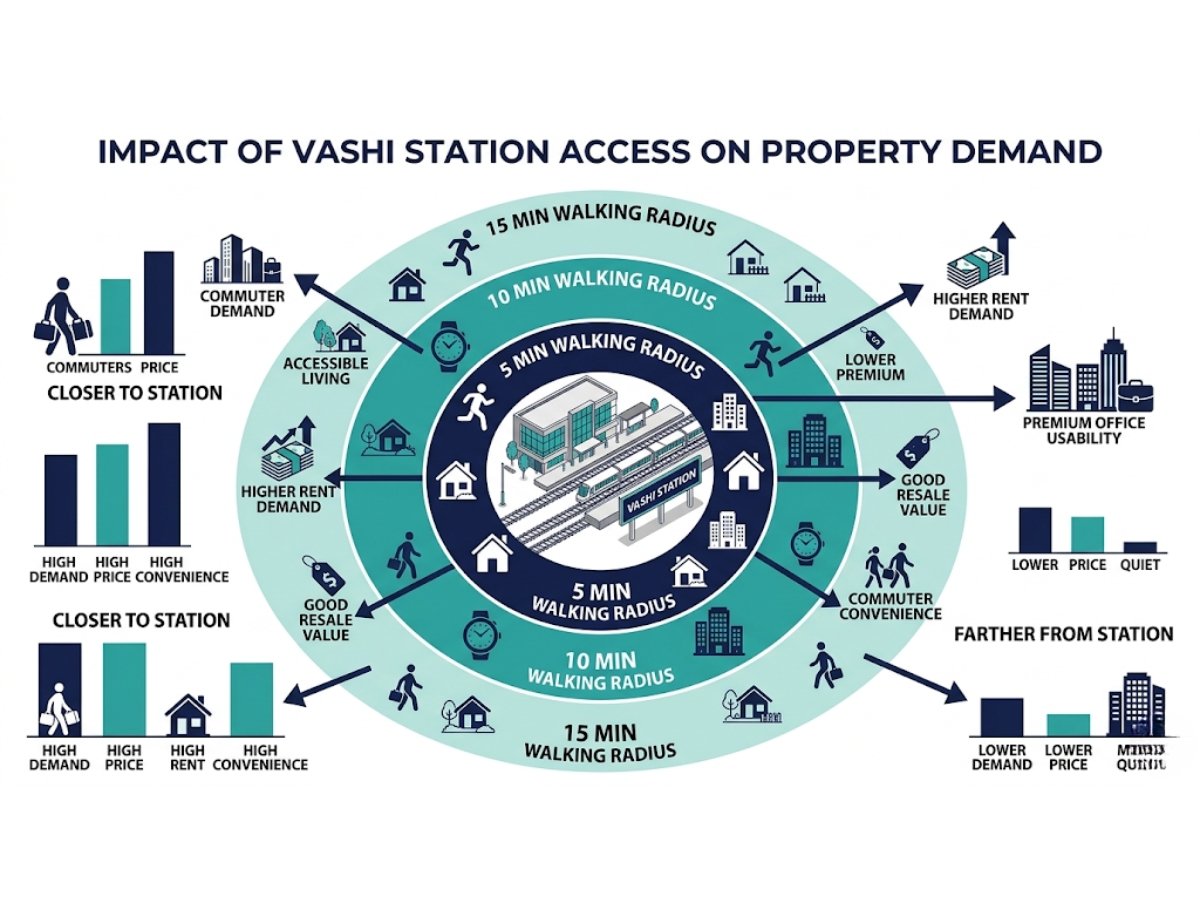

How much does station access really matter in Vashi property demand?

Station access matters a lot in Vashi, probably more than many buyers first realize. It is one of the clearest drivers of both residential rental strength and office usefulness.

The practical reason is simple. Walkability to Vashi station cuts daily dependency on autos, reduces time uncertainty, and improves the liveability of the location for working people. In a mature node where many occupiers are commuters, that translates directly into pricing power. Based on the 2025/2026 market pattern in the dossier, properties within roughly a 10 to 15-minute walking radius of the station can command a capital premium of around 10% to 12%. On the rental side, the same walkability can allow landlords to extract roughly ₹8,000 to ₹15,000 extra per month compared with deeper internal sectors.

Station access helps residential demand, but only where the daily commute advantage is real

For a flat buyer or landlord, station access works best when the route is actually usable on foot. This matters more than people think. A flat may look close on a map, but if the daily path involves traffic-heavy roads, poor crossings, or long last-mile dependence, the station advantage weakens quickly.

That is why “near station” should never be read casually. In Vashi, real walkability is different from radial distance. Properties that genuinely save daily commuting time do better with tenants and resale interest than properties that are technically nearby but operationally inconvenient.

Station access helps office demand differently from shop demand

For office users, station access is even more direct. Staff commute matters. Client access matters. Business timing matters. This is one reason why the station ecosystem, including the office corridor above and around it, has remained so important.

For shops, however, station access alone is not enough. Retail depends not only on commuters but also on frontage, parking, stopping ability, and surrounding catchment. A shop in a station-connected belt can still underperform if customers cannot park or access it comfortably.

Practical comparison: station-side Vashi usually helps offices and rental flats faster than it helps every retail unit. For shops, visibility plus parking plus access quality matter more than station proximity alone.

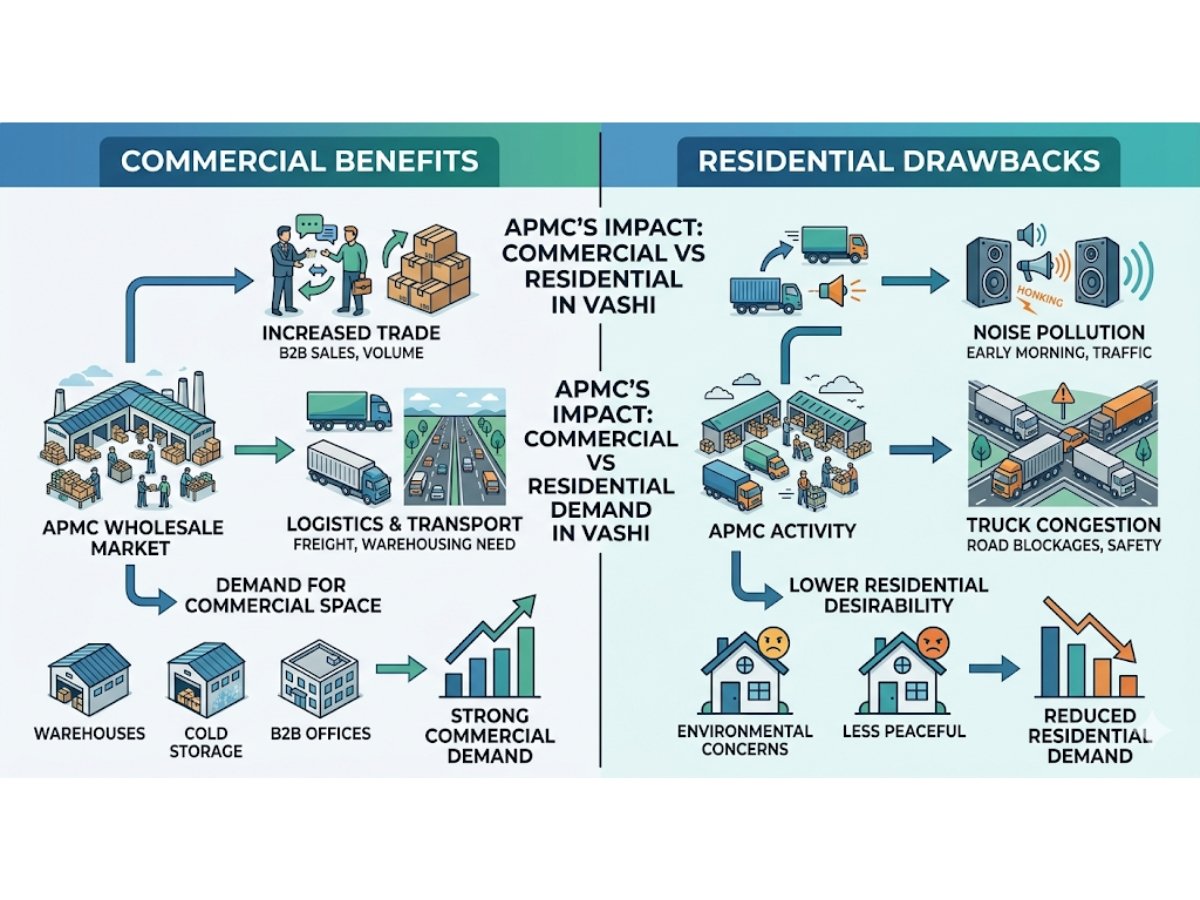

Why APMC strengthens some parts of Vashi far more than others

APMC is one of the biggest economic engines in Vashi, but it creates a very specific type of demand. This is where many buyers get confused.

The APMC market spreads across a very large wholesale ecosystem in Sector 19 and remains deeply important to trade activity. The dossier notes movement of roughly 15,000 to 20,000 trucks daily and also notes official confirmation that APMC is not being shifted out of Vashi, but is planned for in-situ redevelopment. That means the trade engine here is not temporary gossip. It is a continuing structural force.

APMC creates trade, transport, labour, and service movement, not the same kind of demand as family housing

This distinction is critical. APMC-linked movement supports transport operators, traders, loading-unloading activity, support staff, eateries, warehouses, B2B offices, and logistics-related services. That is commercially powerful. But it is not the same thing as family-friendly residential demand.

Around trade-heavy belts, the same strength that helps commerce can damage residential comfort. Heavy vehicle staging, dust, noise, road pressure, and gate congestion change the day-to-day experience of the area. The dossier is especially clear that the truck parking stress around Sector 19 has worsened after the old truck terminal land was repurposed, causing spillover pressure onto surrounding roads.

Which property types gain most from APMC-linked activity

The biggest winners from APMC are usually:

- trade offices

- logistics-linked commercial units

- storage-support businesses

- B2B service businesses

- worker-oriented food and convenience businesses

The wrong fit here is a buyer chasing calm residential life just because the area is economically active.

Example: A commercial investor may like Sector 19 precisely because movement is constant and trade demand is sticky. A residential end user may dislike the same area for the exact same reason.

That is the real Vashi lesson. Commercial utility and residential livability are not automatically aligned.

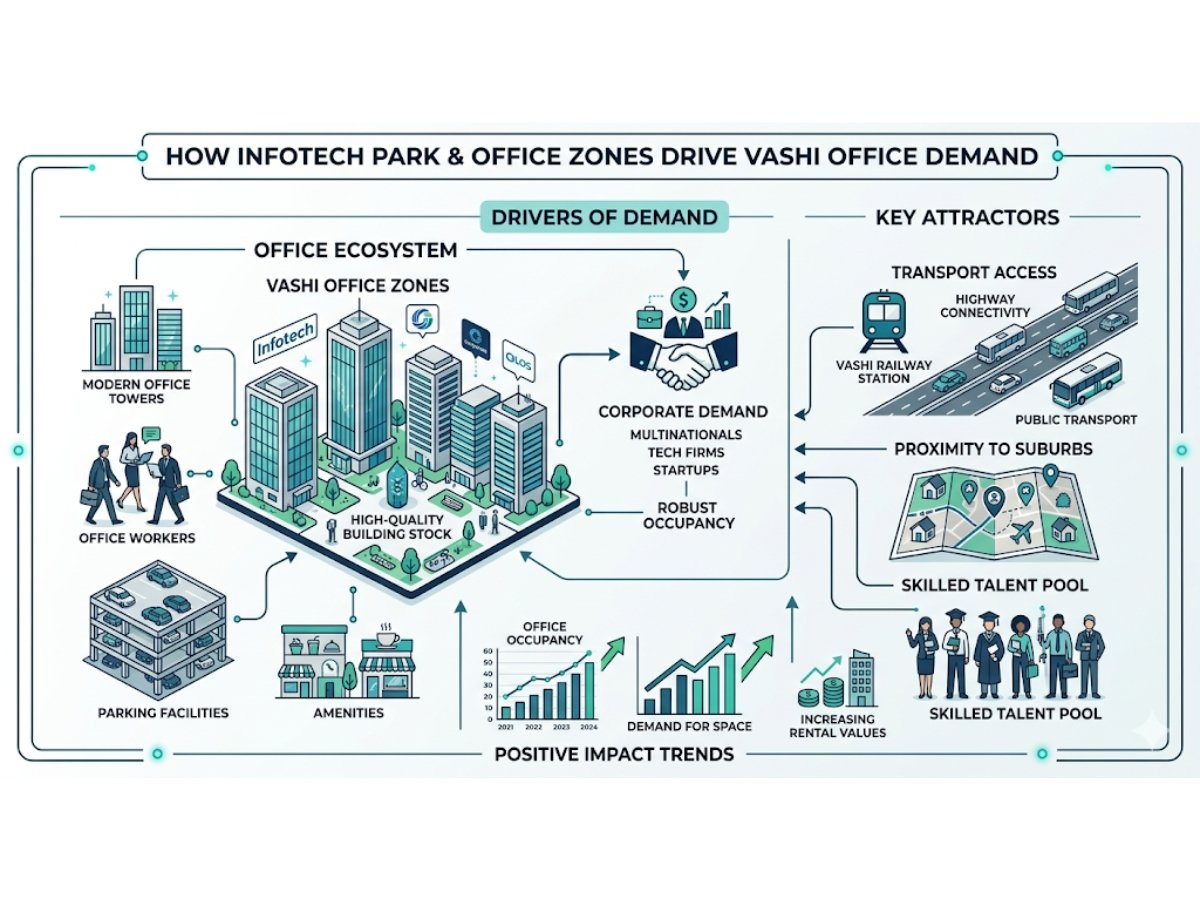

Does Infotech Park still shape serious office demand in Vashi?

Yes, but not in the old, narrow way people sometimes assume. Infotech Park still matters, but today its influence extends into the wider office ecosystem rather than remaining limited to one legacy building.

The station-linked International Infotech Park helped establish Vashi’s formal office identity long ago. But the 2025 office story is bigger. Office vacancy, which used to be far higher in the 2016 to 2020 period, has compressed sharply into roughly the 10% to 16.4% range by 2025 according to the dossier. That is a serious improvement, not a cosmetic one.

The reason is not just nostalgia or local branding. It is actual occupier logic. IT/ITES firms, business services, and GCC-type expansion are using Navi Mumbai for cost advantage, staff access, and better value compared with core Mumbai office markets.

Office users care about access, parking, building image, and staff convenience together

This is where Vashi’s office demand has changed. A decent office location today is not just about a known address. It is about a complete usability package:

- station connectivity

- enough parking

- clean building image

- workable floor plates

- staff convenience

- smoother client access

That is why the market has moved beyond just legacy stock. Demand has spilled into newer Grade-A towers like Cyber One and into modern commercial developments around Sector 30A and similar belts. Indicative office rents of around ₹80 to ₹140 per sq. ft. per month and yields in the 6% to 9% range make commercial office demand mathematically stronger than standard residential rental returns in many cases.

Where Infotech Park influence is strongest and where buyers overestimate it

The strongest office logic sits where station access and modern office product overlap. That is why Sector 30A stands out so much. It benefits from commuter access, office ecosystem depth, and a stronger corporate presentation value.

Where buyers go wrong is assuming any older office stock in Vashi will automatically ride this wave. It may not. Buildings without proper parking, weak maintenance, outdated layouts, or inferior presentation can struggle even in a strong node.

So yes, Infotech Park still matters, but today the real winner is not merely “office near old business zone.” It is modern office stock aligned with present-day occupier standards.

Mall footfall looks powerful, but what kind of property demand does it actually create?

Mall footfall does create demand, but it creates a selective kind of demand. This is another area where buyers often overread the signal.

In Vashi, Inorbit Mall remains a strong anchor with weekday footfall reportedly around 18,000 to 20,000 and weekend movement rising up to roughly 30,000. That helps surrounding retail visibility. For food, casual shopping, branded outlets, and some frontage-led businesses, this matters a lot.

But mall adjacency is not a universal property upgrade.

Retail visibility demand versus residential livability demand

For a shop or restaurant, being near a strong mall can help brand visibility, impulse movement, and customer awareness. For a nearby flat, however, the same footfall can bring traffic, noise, congestion, and slower local movement, especially on weekends.

This is why “near mall” should be read differently depending on the asset class.

| Factor | Helps retail/commercial? | Helps residential? |

|---|---|---|

| Strong daily footfall | Usually yes | Not always |

| Weekend crowd movement | Often yes for F&B and shops | Often no due to congestion |

| Brand visibility | Strong positive | Limited value |

| Traffic and parking stress | Manageable only if asset has proper support | Can reduce comfort and ease |

| Noise and constant public movement | Can help sales | Can hurt family appeal |

Why mall adjacency helps some businesses but does not automatically improve every nearby asset

Vashi’s own retail history proves this. The node has not moved in a straight line from one successful mall to another. Instead, it has become more polarized. Inorbit has held relevance, while older retail centres have weakened badly. Center One has already moved into redevelopment-led transformation, and Raghuleela’s decline and redevelopment direction show the same larger shift. This is a big local signal.

The signal is this: retail demand is consolidating into stronger formats, while obsolete mall stock is getting replaced by more viable commercial office or mixed-use projects. So when a buyer says, “There is a mall nearby, so the property must appreciate,” that is incomplete thinking. The real question is: what kind of mall, what kind of movement, and which asset class are we talking about?

Which parts of Vashi benefit from one demand engine, and which benefit from overlap?

In Vashi, the best-performing micro-markets are usually not driven by one single factor. They are driven by overlap. That overlap creates stronger demand, faster leasing, and better resilience.

| Micro-location | Primary demand engines | What it usually means |

|---|---|---|

| Sector 30 / 30A | Station + office ecosystem + Inorbit-led visibility | Strong for Grade-A offices, transit-linked commercial activity, selective retail |

| Sector 17 | Legacy commercial visibility + established market movement | Strong commercial recall, but parking and congestion are major filters |

| Sector 19 | APMC + logistics + trade activity | Excellent for trade-linked commercial use, weak for peaceful family residential use |

| Sectors 9, 14, 28 | Established residential ecosystem + internal quieter character | Better fit for residential buyers who want Vashi without constant commercial abrasion |

This is the practical map most buyers need. Sector 30A benefits from overlap. Sector 19 benefits from trade dominance. Sector 17 benefits from visibility and legacy business pull. Inner residential sectors benefit from separation from the heaviest commercial friction.

Residential, office, and retail buyers should not read Vashi demand in the same way

A strong Vashi location for one buyer can be the wrong Vashi location for another.

For a flat buyer, the real questions are quieter roads, building age, redevelopment potential, daily convenience, and distance from high-friction commercial activity. A cheaper older CIDCO-style option may look attractive at first, but the hidden capex can be serious. The dossier rightly notes that older stock can require roughly ₹10 lakh to ₹25 lakh in upgrades depending on condition.

For an office buyer, the lens is different. Staff access, building image, maintenance quality, and parking discipline matter a lot. A building that is “well located” but operationally messy may not attract strong office occupiers.

For a shop buyer, the right questions are frontage, visibility, stopping ability, and compliance with parking realities. In some Vashi belts, commercial movement is strong but parking is so poor that customer convenience suffers.

This is why product-fit matters more than broad Vashi hype.

When does strong movement in Vashi not translate into strong property quality?

Quite often, actually. Busy roads and visible activity can create a false impression of strength.

A residential building on a crowded mixed-use stretch may see movement all day, but that does not automatically make it better for end users. Noise, dust, slower exits, poor gate discipline, and traffic pressure can reduce family appeal.

The same logic applies commercially. A shop on a busy stretch with poor parking may look attractive on paper, but if customers fear towing, blocking, or access hassle, the theoretical visibility loses value.

Quick caution checklist before trusting “high demand” in Vashi

- Is the property genuinely walkable, or only map-close?

- Does the building have usable parking, not assumed street parking?

- Is the road activity helping your asset class or hurting it?

- Are you buying near APMC for trade logic or accidentally for family living?

- Is the building old enough to require major capex soon?

- Is the nearby mall or market still a live draw, or just an old name?

This is where many generic articles fail. They confuse movement with quality. But in Vashi, density without support infrastructure can become friction very fast.

You may also want to read Best Commercial Sectors in Vashi to see where this demand shows up most clearly.

How should a buyer or investor read Vashi demand before making a purchase decision?

The smartest way is to read Vashi through a practical filter, not through a brand-name filter.

First, check whether the property’s use matches the area’s main demand engine. A trade-heavy pocket should be judged like a trade-heavy pocket, not like a residential enclave.

Second, verify parking reality. This has become more important in Vashi because parking pressure can directly affect commercial usability and customer comfort.

Third, inspect at the right time. Visit station-side locations during commuter rush. Visit APMC-linked belts when truck movement is active. Visit mall-adjacent roads on weekends. Vashi changes sharply by time of day.

Fourth, read older stock carefully. The leasehold-to-freehold policy shift is a major local valuation factor for some older properties, especially where it improves resale ease and redevelopment attractiveness. But that does not erase building-age issues.

Fifth, calculate true entry cost. A lower base price can be misleading if immediate repair, parking, layout correction, or internal upgrading is unavoidable.

Final verdict: the strongest Vashi demand comes where access, usability, and purpose align

Vashi remains one of Navi Mumbai’s most functional and premium real estate nodes, but its strength comes from present-day utility, not from vague “prime location” branding. Station access supports commuter-led flats and office demand. APMC supports trade-heavy commercial demand. Infotech Park and the wider office corridor support serious corporate occupancy. Mall footfall supports selective retail, not every nearby asset.

The real rule is simple. Buy in Vashi only when the property type matches the demand engine around it and when the surrounding friction does not cancel out the benefit. That is why a Grade-A office in Sector 30A can make excellent sense, a trade office near APMC can be commercially logical, and a quieter internal residential pocket may still be a better home than a more visible but more chaotic address.

FAQs

Frequently Asked Questions