Airoli-Ghansoli Industrial Land and Tech-Infra Trend: What Is Actually Driving Demand?

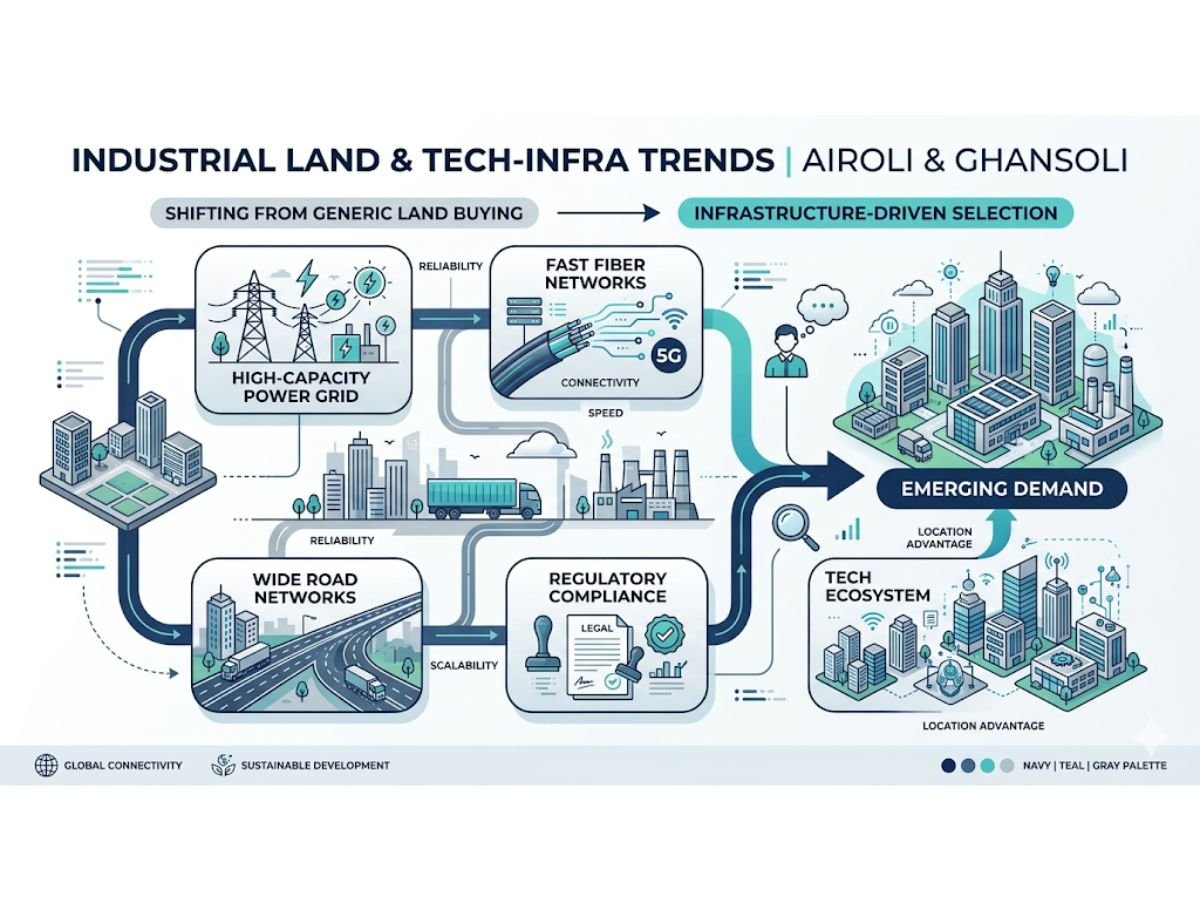

Airoli-Ghansoli is still a serious industrial and tech-infra corridor, but it is no longer one broad “buy anything and wait” market. Airoli usually works better where enterprise-tech ecosystems, stable office demand, and polished occupier environments matter. Ghansoli usually works better where larger-format infra, backend tech, or data-linked demand matters. The real trend in 2026 is selective value concentration around power, road width, fiber readiness, compliance, and actual usability, not generic land appreciation.

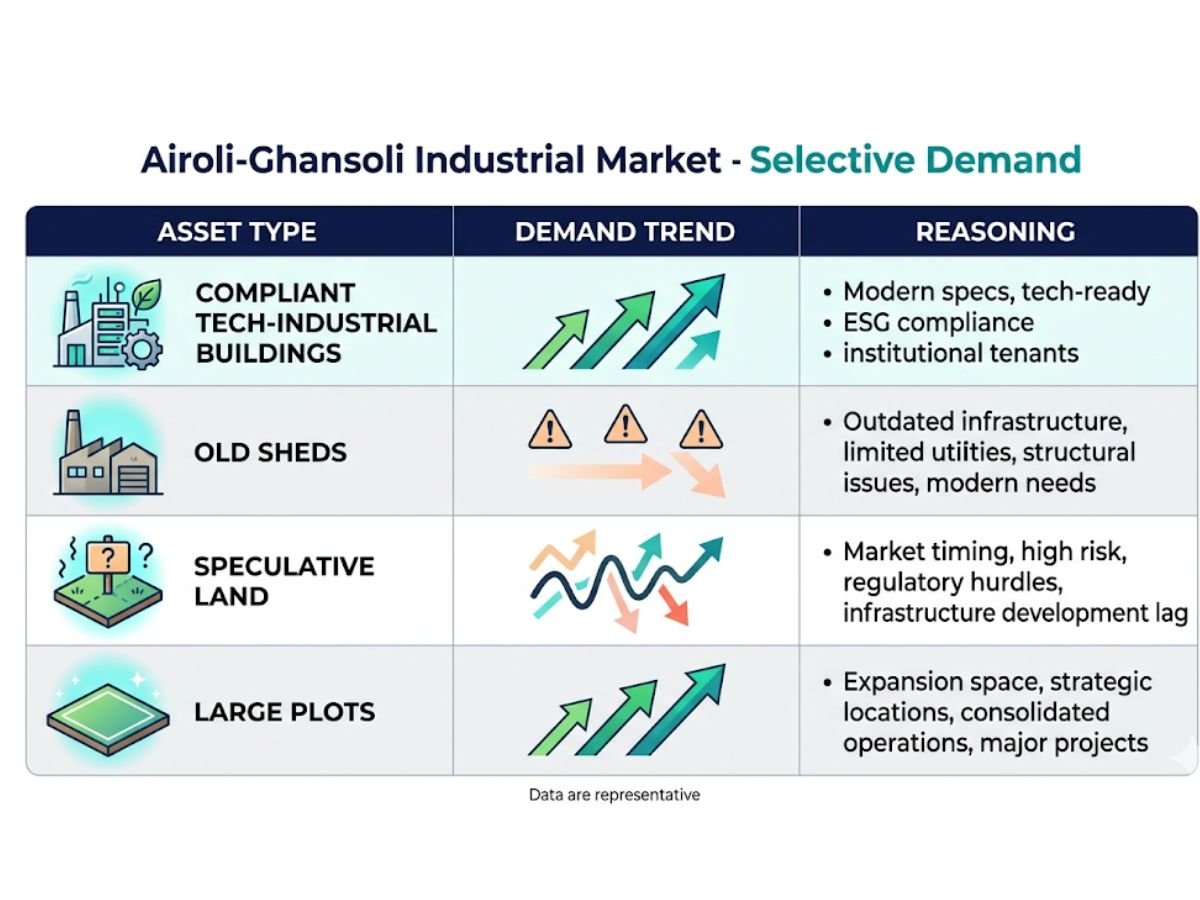

Airoli-Ghansoli is rising, but not as one uniform industrial market

| Asset Type | What Is Happening in the Market | Why |

|---|---|---|

| Compliant tech-industrial buildings, better plots, infra-ready land | Stronger interest and better long-term relevance | These assets fit power-heavy, fiber-heavy, backend, or enterprise uses. |

| Old galas, narrow-road sheds, obsolete workshops | Far more selective demand | Many cannot support scalable FSI, truck movement, floor loading, or modern occupier requirements. |

| Small speculative landholding without a development plan | Risky | MIDC timelines, holding friction, and local taxes can punish passive holding. |

| Large-format plots with good access and upgrade potential | Still strategically relevant | They can suit redevelopment, built-to-suit infra, or serious owner-user deployment. |

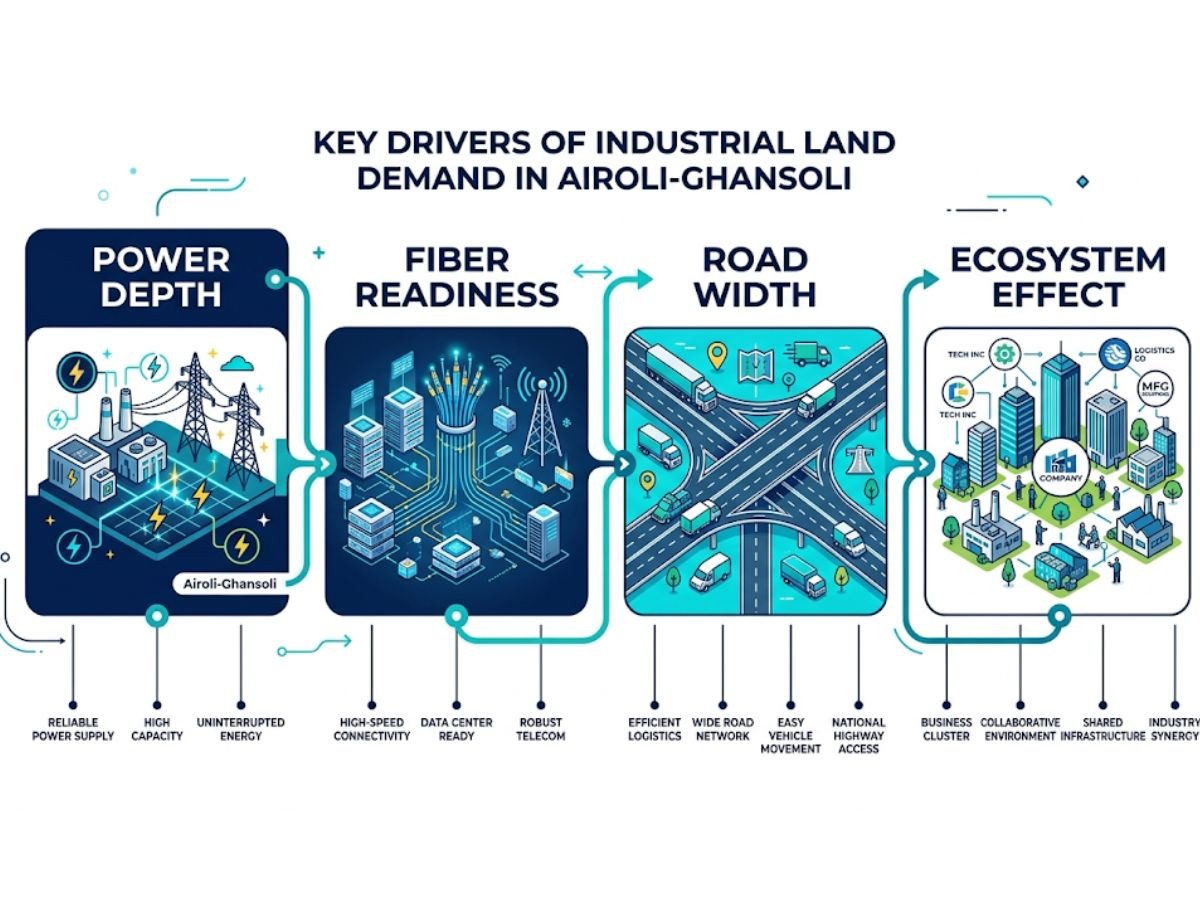

What is actually driving the Airoli-Ghansoli industrial land and tech-infra trend?

The main drivers here are not the usual generic lines like “good connectivity” or “future growth.” In this corridor, demand becomes real only when the location can support enterprise-grade operations.

Power depth matters more than most buyers realise

For normal industrial users, power is important. For data-heavy or backend tech-infra users, power is everything. The corridor’s relevance is linked to the broader power architecture already visible in the TTC belt and Navi Mumbai’s data infrastructure story. Public reporting around the Blackstone-Panchshil hyperscale plan in Navi Mumbai, with 500 MW capacity and over 3 million sq ft across 14 buildings, shows the scale of digital infrastructure capital now targeting this side of the region. That kind of investment does not happen because of branding. It happens because power and large-format infra logic exist.

This does not mean every nearby property suddenly becomes data-center-grade. It means the market starts rewarding plots and buildings that can realistically plug into that level of infrastructure ecosystem.

Fiber readiness is now part of land value

A plot in this belt is no longer judged only by frontage, compound wall, or age of structure. For backend offices, cloud-linked operations, support centers, and certain tech occupiers, fiber continuity matters. That is one reason the broader Airoli-Ghansoli-Rabale side feels different from a normal industrial pocket.

A simple way to understand it is this: in older industrial thinking, land value came from manufacturing utility. In the current tech-infra phase, land value increasingly comes from whether the site can support digital operations with low downtime.

Road width is not just about trucks. It changes development potential

This is one of the most important points in the whole article. In MIDC planning logic, road width affects the development potential of the plot. Under the MIDC Draft CDCPR, higher permissible FSI is linked to road width and plot size, and the table for additional FSI shows stronger development potential from 18 metres onward. That is why two plots in the same micro-market can behave very differently. One sits on a road that can support higher intensity development. The other does not.

That is also why frontage alone can mislead buyers. A “good-looking” plot on a weak internal road is not the same thing as a legally scalable plot with proper access width.

Surrounding occupier ecosystem compounds value

Airoli has long had stronger enterprise visibility because of established IT parks and corporate environments. Ghansoli benefits from the Reliance Corporate Park side, nearby business activity, and its adjacency to the wider TTC industrial-power ecosystem. The value of some plots rises not because of what they are today, but because of what kinds of occupiers can realistically work around them tomorrow.

That ecosystem effect is real. But it is selective. It helps land and buildings that fit the corridor’s next-use logic.

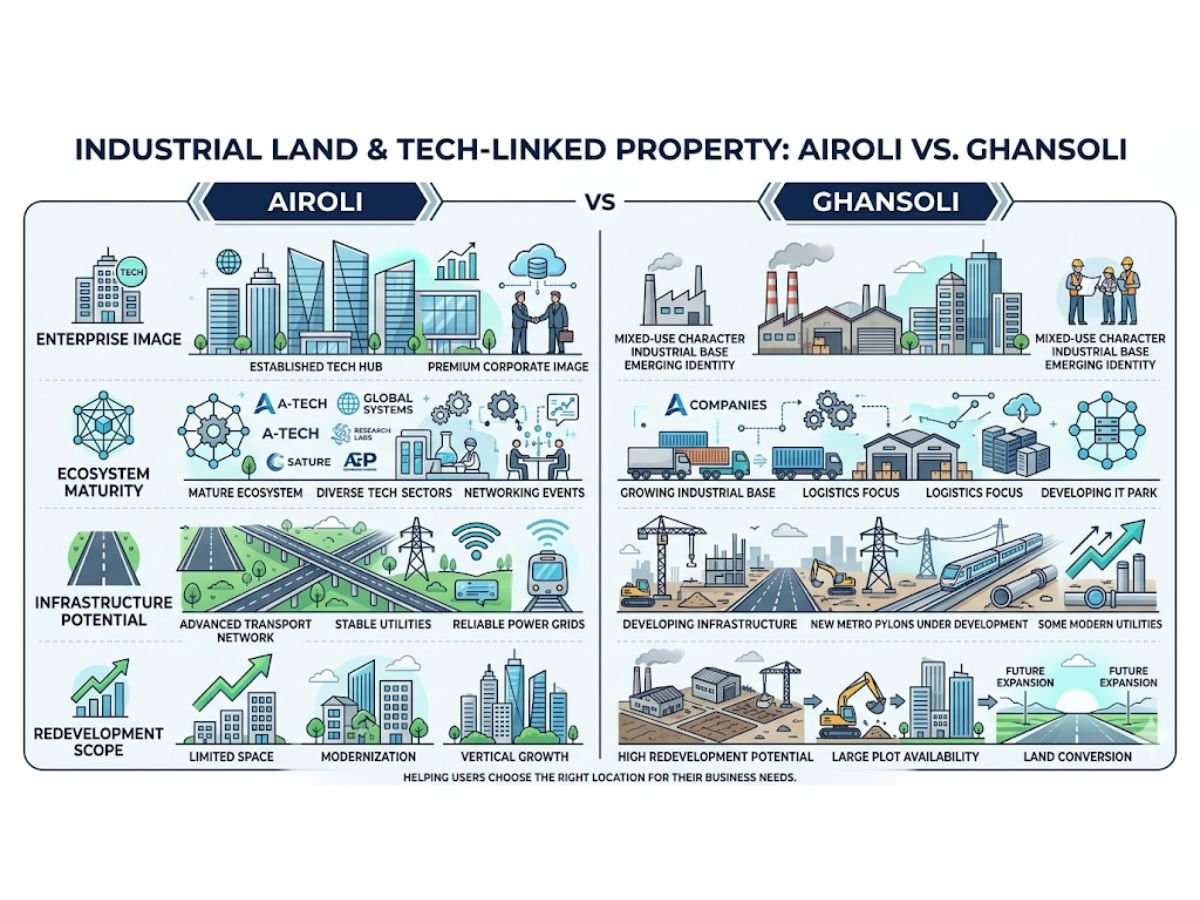

Does Airoli work better than Ghansoli for industrial land and tech-linked property?

There is no one-line answer, but there is a practical one.

Airoli usually feels stronger when the requirement is a more polished enterprise environment, predictable office-grade demand, and immediate credibility for backend corporate or hybrid operations. Ghansoli usually feels stronger when the requirement is larger-format infra logic, redevelopment potential, stronger backend utility, or long-horizon tech-industrial positioning.

| Factor | Airoli | Ghansoli |

|---|---|---|

| Enterprise-tech image | Stronger and more established | Improving fast, but more mixed |

| Mature office ecosystem | Stronger | Moderate to strong in select pockets |

| Large-format infra potential | Selective | Usually stronger |

| Data-linked market narrative | Present, but less dominant than pure office logic | Stronger |

| Buyer comfort for polished ready environments | Higher | Depends more on micro-location |

| Long-horizon redevelopment or backend infra story | Selective | Stronger in the right pockets |

Airoli is easier to understand. Ghansoli is more rewarding only when understood properly.

That is why many normal buyers feel safer in Airoli, while more aggressive long-horizon infra buyers keep watching Ghansoli and the nearby TTC side more closely.

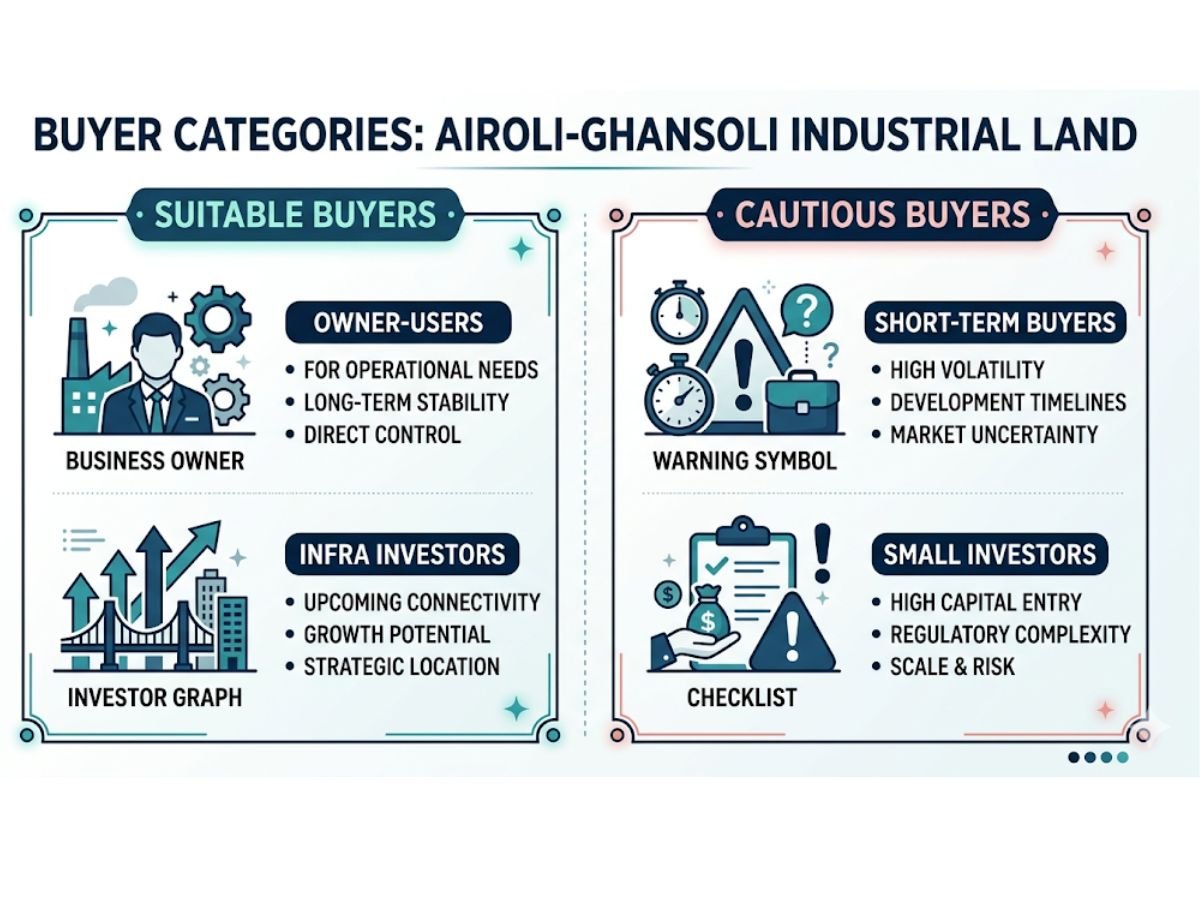

Which types of buyers should seriously look at this corridor, and who should stay selective?

Not every buyer should be here.

Owner-users

If a company genuinely wants to operate from the corridor, this market can make a lot of sense. That is because owner-users can extract real value from power, access, ecosystem, and deployment speed. They are not just waiting for appreciation. They are using the asset.

Long-horizon infra or tech-linked investors

These are the buyers who can benefit the most from the current phase, but only when they have compliance bandwidth, capital patience, and a clear development plan. The Maharashtra GCC Policy 2025 adds to this environment by offering incentives such as power tariff subsidy, electricity duty exemption, and related support for eligible units. That does not make every site attractive, but it does strengthen the broader case for serious tech-linked occupancy in Maharashtra, including the Mumbai Metropolitan Region.

Short-term appreciation seekers

This is where caution becomes necessary. The corridor sounds exciting, but it is not friendly to passive landholding. MIDC development timelines, extension issues, and the broader holding burden can damage returns if the buyer is just parking money and waiting.

Small industrial buyers with weak compliance capacity

This group should stay careful. If the buyer cannot verify transfer conditions, title chain, road width, power feasibility, dues, and development limitations properly, the risk goes up quickly.

What kind of property is actually benefiting here: raw land, industrial plots, built sheds, or tech-industrial buildings?

The better-performing category in this corridor is usually the one that is most ready for actual use.

Built and compliant tech-industrial buildings, shell spaces, or properly located industrial plots with clean paper trail and scalable access are much more relevant than vague raw-land stories. That is because the market today rewards speed, infra compatibility, and execution readiness.

Older sheds and galas can still have value, but not automatically. If they sit on narrow roads, have weak loading practicality, poor structural adaptability, or unresolved leasehold issues, they are not really part of the high-quality tech-infra story even if brokers market them that way.

So the asset question matters as much as the location question. Sometimes more.

Which local signals show real strength, and which signals are just market storytelling?

A reader should learn to separate proof from noise.

Real strength signals include:

- visible institutional capital coming into digital infrastructure

- better road and corridor integration work that changes movement practicality

- policy support for GCC and enterprise operations

- plots or buildings that clearly fit the road-width, access, and compliance requirements for larger-scale development

The corridor connectivity story is also getting support from ongoing infrastructure work. Indian Express reported that the Airoli-Ghansoli bridge project is a 3.47 km link, budgeted at about ₹540 crore, with completion targeted for September 2026, and that it is expected to improve access to MIDC and Mindspace-side movement. That matters, but it should be treated as a supporting mobility factor, not as a magic justification for every nearby asset.

Misleading signals include:

- “data center zone” language for tiny or unusable assets

- blind assumptions that every old industrial property near Ghansoli gets premium value

- treating a long-term corridor redevelopment or slum overhaul proposal as an immediate investment trigger

- using only future branding while ignoring power, road, and paper reality

The same caution applies to the wider MIDC redevelopment story in the Thane-Belapur belt. The recent 338-acre tender activity is important, but it is still a long-cycle and complex redevelopment process, not an instant value unlock for every plot around it.

What should a buyer check before purchasing land or industrial-tech property in Airoli-Ghansoli?

This is the part where real money gets protected.

Buyer checklist

- Verify the MIDC leasehold chain, not just seller possession

- Check whether any transfer permission, dues, or legacy conditions are pending

- Confirm actual road width on ground and match it with development potential

- Verify whether the asset is on a road that can realistically support the intended FSI and use

- Check NMMC dues, local tax burden, and usage classification

- Confirm whether any ULC-related transfer burden or special charge may apply

- Ask for proof of lease rent payment, not just verbal assurance

- Verify whether the structure has legal completion and usable compliance status

- Assess truck turning radius, entry-exit practicality, and loading movement

- Check whether the intended power requirement is realistic for that exact site

A buyer in this belt is not just buying a parcel. The buyer is entering a regulatory system.

Where can buyers get trapped in this corridor?

The most common trap is simple: paying future-tech pricing for present-day obsolete stock.

A narrow internal-road shed with weak access, no meaningful redevelopment headroom, and poor structural adaptability may still get pitched using words like “near data center,” “near RCP,” or “next big corridor.” That language can push buyers into overpaying for utility that does not exist.

Another trap is passive holding. A retail speculator may think, “I will buy now and develop later.” But this is not the kind of corridor where delay is free.

Example 1: the wrong buyer

A small investor buys an MIDC-linked industrial plot in the broader belt with no clear occupier plan. Three years later, he is still sorting title documents, transfer conditions, and development viability. Meanwhile, holding costs and project delay reduce the real attractiveness of the asset. On paper, the corridor has grown. In practice, his asset has not moved proportionately because it was never infra-ready.

Example 2: the right buyer

A serious owner-user or tech-linked investor acquires a better-located plot with proper access and a clear development roadmap. Because the buyer knows the intended use from day one, the corridor’s power, road, and ecosystem advantages become usable, not theoretical.

That is the difference between buying a story and buying an operational asset.

So what is the real trend in Airoli-Ghansoli right now?

The real trend is selective, infrastructure-led consolidation.

Airoli-Ghansoli is becoming more valuable for the right kinds of industrial-tech and backend-infra use. But it is also becoming harsher on weak stock, passive holding, and lazy assumptions. The corridor is not rewarding everything. It is rewarding readiness.

That is why the correct question is no longer, “Is this belt growing?” The correct question is, “Does this exact asset fit the next phase of this belt?”

Conclusion

Airoli-Ghansoli remains one of Navi Mumbai’s most important industrial-tech transition corridors, but the easy money phase is over. This is now a selective market where power depth, road width, fiber readiness, occupier ecosystem, and legal-operational clarity decide value. Airoli usually wins on maturity and enterprise comfort. Ghansoli usually wins on selected long-horizon tech-infra and backend potential. Buy here only when the asset itself is strong enough to deserve the corridor story.

FAQs

Frequently Asked Questions