Exit Risk, Vacancy Risk and Liquidity in Industrial Property in Navi Mumbai

Industrial property is not liquid by default. In and around Navi Mumbai, the easiest assets to exit are usually practical, bankable, compliance-clean units that more than one kind of tenant or buyer can use. The risky ones are often oversized, over-specialized, awkwardly planned, weak on truck movement, or tied up in transfer and approval friction. That is the real point: a property can look strong on rent or price, yet still become hard to re-lease or sell when your first plan fails.

A lot of investors understand yield. Far fewer understand time-to-exit.

That is where mistakes happen.

A compact gala in a usable industrial belt may quietly outperform a larger “impressive” unit simply because more buyers can afford it, more occupiers can use it, and more banks are comfortable funding it. On the other hand, a bigger warehouse, a specialized shed, or a bare plot may look attractive on paper but become slow-moving if the next tenant pool is narrow, the transfer cost is heavy, or the property needs too many conditions to line up before someone can actually operate from it.

In Navi Mumbai, this gets even more practical because industrial real estate is not one uniform market. TTC-side units, Taloja stock, Panvel-Kalamboli logistics property, and Dronagiri-side industrial land do not behave the same way. MIDC, CIDCO leasehold, MPCB category, truck movement, staff commute, and lender comfort all change the answer.

This article explains how to judge exit risk, vacancy risk, and liquidity before you buy, not after the property gets stuck.

Quick Summary

The quickest answer is simple. Industrial property becomes easier to exit when it has broad usability. It gets stuck when it depends on a narrow use case, a narrow buyer pool, or messy paperwork.

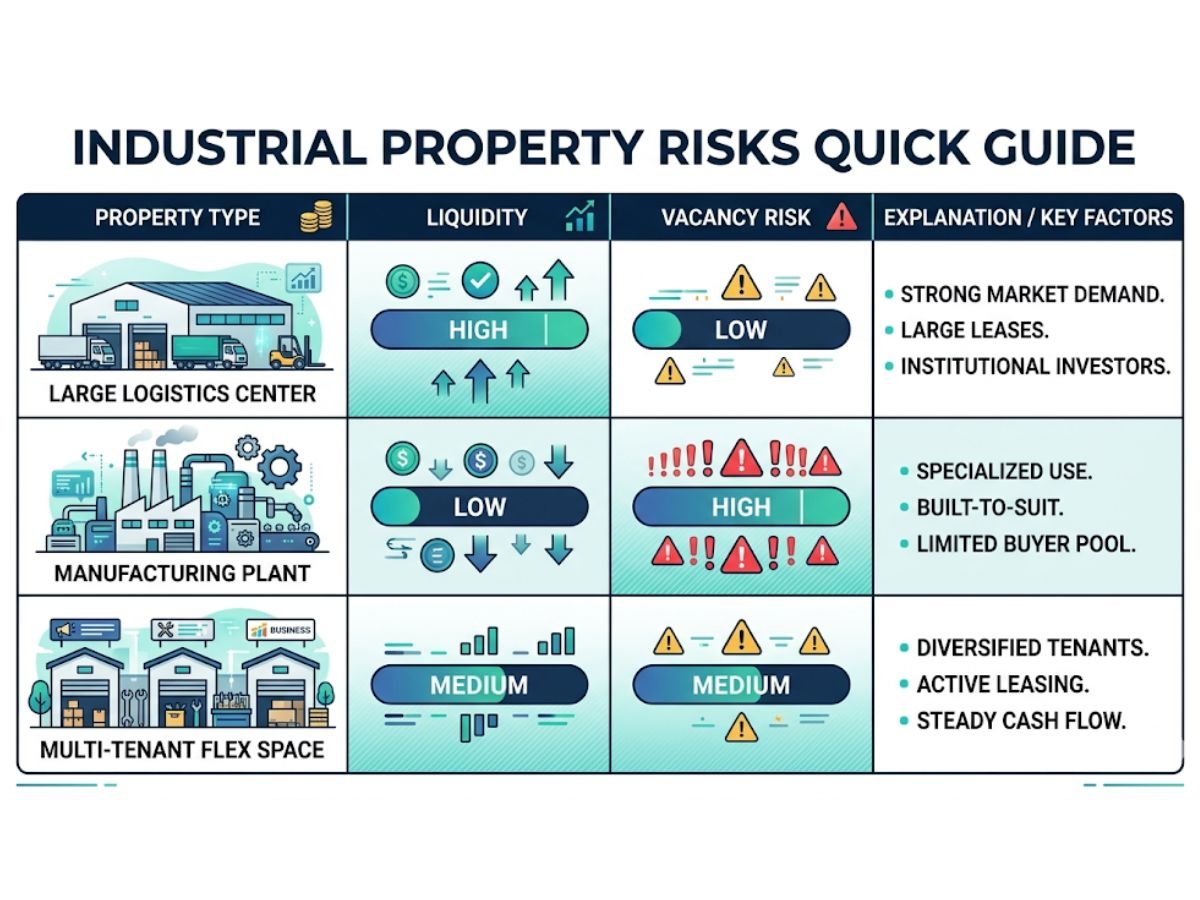

| Property type | Liquidity tendency | Vacancy tendency | Why it behaves this way |

|---|---|---|---|

| Compact gala or small industrial unit | Usually higher | Usually lower | Lower ticket size, broader SME demand, easier re-leasing |

| Ready-built shed with practical specs | Moderate to high | Moderate | Works well if loading, power, access, and layout are usable |

| Modern warehouse with strong clear height and truck movement | High in the right logistics belt | Low to moderate | Strong occupier demand where logistics depth is real |

| Specialized Red-category industrial shed | Lower | Higher | Narrow tenant pool, higher compliance friction |

| Bare industrial plot bought only for appreciation | Moderate to low | High income risk | No built income, holding risk, utilization conditions can create pressure |

| Awkward upper-floor or poorly planned industrial unit | Lower | Higher | Weak loading, poor truck handling, narrow operational fit |

The practical takeaway is this: industrial property liquidity is usually strongest in assets that the next tenant, the next buyer, and the next lender can all understand without too much friction.

That three-way test matters more than brochure language.

Exit risk, vacancy risk, and liquidity are not the same thing. What is the difference?

These three ideas are connected, but they are not identical.

Exit risk means how hard it is to sell

Exit risk is about resale. If you decide to sell in six months, one year, or two years, how many realistic buyers are available? Can they arrange funding? Can they understand the asset fast? Can they clear transfer conditions? If the answer is no, your exit risk is high.

A property can look valuable and still carry high exit risk. This is common in assets that are too specialized, too expensive for the local buyer pool, or tied to authority-side friction.

Vacancy risk means how hard it is to keep income going

Vacancy risk is about cash flow interruption. Suppose your current tenant leaves. How long will it take to find the next tenant, complete onboarding, and restart rent? If the property only suits one narrow business type, or if the next user faces fire, consent, power, or layout problems, vacancy risk rises sharply.

This is where many owners get trapped. The property was “leased once,” so they assume it will always lease again. That is not how the market works.

Liquidity means how fast and how cleanly the market responds

Liquidity is the combined market response. A liquid property gets attention from multiple buyer types, gets funded more easily, and moves with less administrative friction. An illiquid one may still have a theoretical price, but the market does not respond quickly or cleanly.

That is why a high-yield industrial asset can still have poor liquidity. Rent alone does not make an asset easy to sell.

Why two industrial units in the same area can have completely different liquidity

This is one of the biggest truths in industrial property. Same area does not mean same risk.

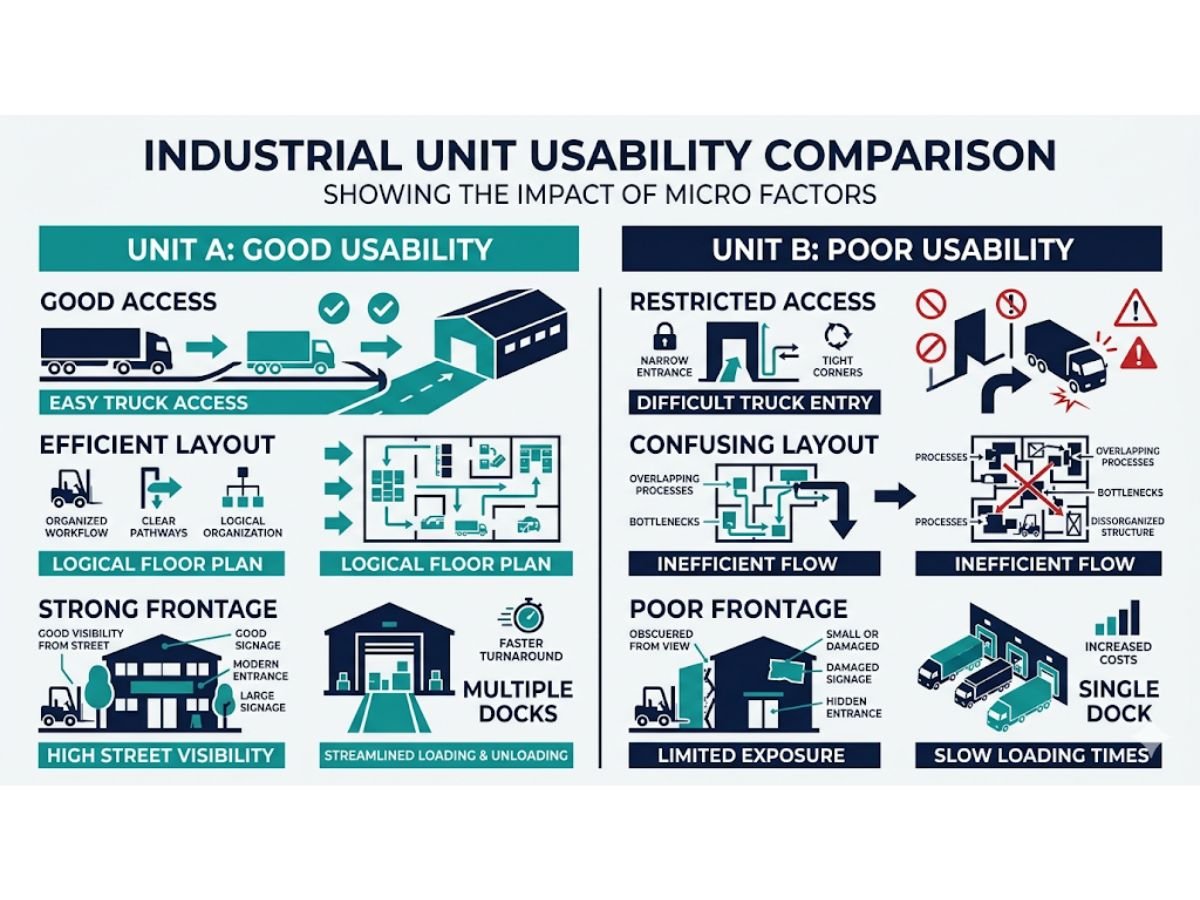

Two units in the same belt can behave very differently because industrial liquidity comes from micro-usability, not just pin code.

Size, frontage, loading, turning radius, and usable internal layout

A usable unit is easier to exit because more businesses can work from it. A badly shaped one starts narrowing its market from day one.

For example, one unit in Taloja may have smooth truck entry, sensible frontage, efficient internal planning, and decent turning space. The next unit may be inside a tighter cluster with weak access, bad loading position, and awkward internal columns. Both are in the same industrial belt, but one can attract more occupiers and the other can remain slow-moving.

Clear height, floor loading, power, and access matter more than brochure language

Industrial buyers should be careful with broad marketing language like “prime warehouse” or “excellent industrial property.” The real test is technical usability.

Modern distribution users usually prefer clear heights around 32 to 40+ feet. Manufacturing needs vary, but many serious occupiers still need practical volume, power, and movement. Standard dock height of around 48 to 52 inches, proper apron space, and dependable three-phase power can directly affect how fast a property leases or resells.

If a warehouse has only around 14 feet of clear height, weak turning radius, or no practical dock handling, it may not match modern logistics demand even if the area sounds good on paper.

Divisibility and multi-user flexibility reduce exit risk

One of the most underrated liquidity drivers is divisibility.

A 20,000 sq ft structure that can be split into four smaller occupancies often has lower exit risk than a single rigid block. Why? Because the next tenant pool becomes wider. The same logic applies in resale. A property that appeals to one giant user is more fragile than one that can attract multiple SME or mid-size users.

Example: same belt, different outcome

Imagine two industrial units in the same zone.

- Unit A is a 6,000 sq ft usable ground-level unit with decent loading, clean paperwork, broad Green-category use potential, and a realistic rent.

- Unit B is a 14,000 sq ft specialized shed with narrow access, custom fit-out for one process, and transfer or compliance queries.

Unit A may exit faster at a lower headline rent because the market for it is broad. Unit B may show a better yield on paper but remain vacant or take much longer to sell.

That is exactly why yield should never be read in isolation.

Which industrial formats usually stay more liquid, and which carry higher vacancy risk?

The format you buy often decides the future before the market does.

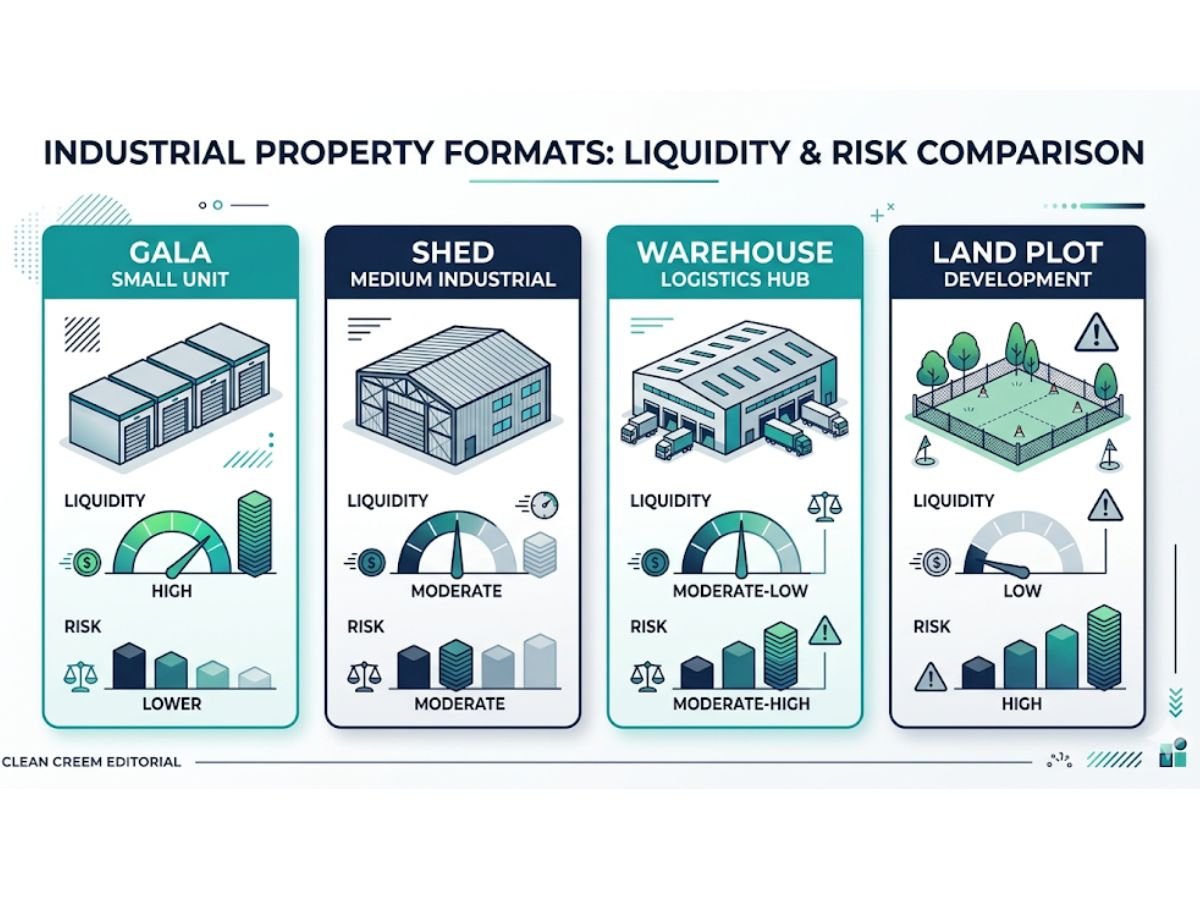

Compact gala or small industrial unit

This is usually the most liquid format for small and mid-size investors. The reason is not glamour. It is market depth.

More SMEs can afford it. More businesses can adapt to it. More local occupiers can take quick decisions on it. In clusters with active SME demand, a good compact industrial unit can be easier to re-lease and easier to resell than bigger stock.

This does not mean every gala is safe. Poor loading, upper-floor limitations, weak power, or documentation gaps can still hurt liquidity. But as a format, compact units usually offer a broader exit audience.

Ready-built shed

A ready-built shed can be attractive because it saves time. For an occupier or investor, immediate usability has real value.

But sheds are only liquid when their specs match real demand. A shed with usable height, workable truck entry, enough power, and a broad compliance profile can move reasonably well. A shed built around one specialized operation can become much harder to place.

So the right question is not “ready shed or not?” It is “ready for whom?”

Large standalone warehouse or specialized facility

This format can look strong in logistics-led belts, especially near freight-linked growth corridors, Panvel-side warehousing demand, or JNPA-influenced movement. But it is not automatically liquid.

Larger warehouses need a deeper tenant pool, stronger last-mile practicality, and a bigger buyer ticket. If the warehouse is well designed with around 32-foot clear height or more, proper dock handling, good apron space, and strong connectivity, liquidity can be good. If not, the asset may sit for months while still being marketed as “premium.”

Specialized facilities are even riskier. The more the asset depends on one narrow use case, the more vacancy and exit risk rise.

Bare industrial plot bought only for future appreciation

This is where many buyers become overconfident.

A plot gives flexibility, yes. But it also creates holding risk, execution risk, and future compliance risk. Under MIDC-style logic, non-utilization can become a real issue. The dossier notes that under-utilized plots may face non-utilization charges of around 10% per annum. That changes the economics very quickly.

A bare plot is not a passive asset. It needs a clear plan, capital discipline, and awareness of construction deadlines and authority conditions. Otherwise, resale becomes slower because the next buyer is not just buying land. They may be inheriting delay, cost, and compliance pressure.

What creates vacancy risk even before the tenant leaves?

Vacancy usually does not begin when the tenant vacates. It begins when the owner buys the wrong asset.

Rent level mismatch versus actual occupier demand

Some industrial owners buy on yield math that exists only in broker conversations. They underwrite the deal based on an optimistic rent, not achievable rent.

That gap becomes visible only later, when the tenant leaves and the market does not support the same number. Then the unit sits vacant because the rent expectation was wrong from the start.

Over-specialized fit-out that narrows the tenant pool

Highly customized industrial spaces can produce this problem. A unit designed around one chemical process, one pharma workflow, or one specialized layout may reduce the next-tenant pool sharply.

Sometimes the very fit-out that helped the first tenant becomes the reason the second tenant walks away.

Staff access, parking, truck movement, and operating convenience

This part is often ignored by investors who do not think like occupiers.

Industrial property needs to work every day, not just during inspection. If staff commute is painful, truck turning is poor, parking is tight, or operating hours become awkward because of approach issues, re-leasing slows down. In some belts, last-mile convenience matters almost as much as headline connectivity.

Compliance or documentation friction that slows onboarding

This is a major real-world issue.

If the next tenant faces delays in fire clearance, power enhancement, consent requirements, sanctioned-use confirmation, or building completion status, they may simply move to another property. Even small documentation gaps can damage leasing speed because industrial users usually want operational certainty.

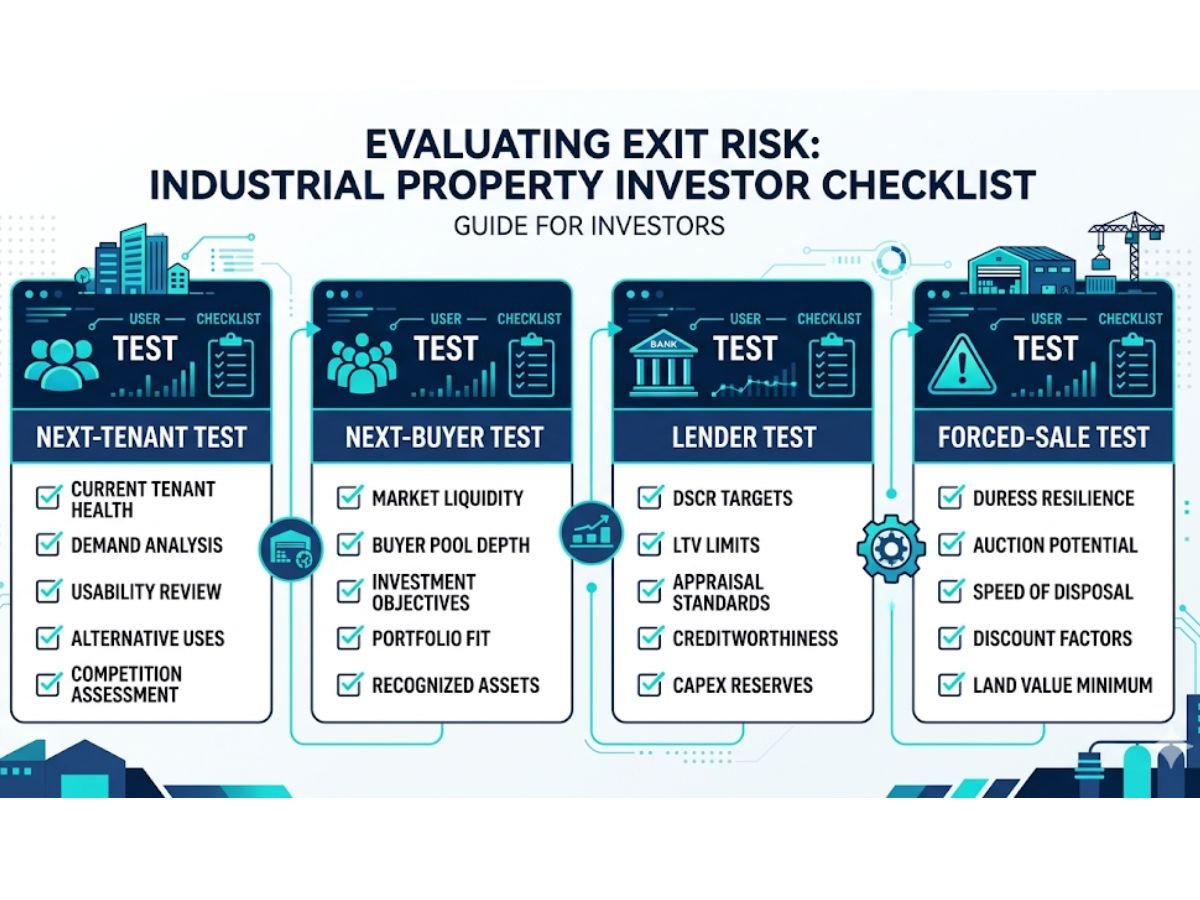

How should a buyer check exit risk before buying industrial property?

This is the most useful part of the whole discussion. Before token, before negotiation drama, before rental projection, run a practical four-part test.

The next-tenant test

Ask one simple question: if the current user leaves, which other business can start here with minimal changes?

If the honest answer is “only one very specific type,” vacancy risk is already high. A stronger asset can usually serve more than one occupier profile without major redesign.

Check:

- broad use compatibility

- loading and truck practicality

- power readiness

- fire and operational readiness

- realistic rent for the micro-market

The next-buyer test

Now think like the next purchaser, not like the current seller.

Can a normal buyer understand the asset quickly? Is the ticket size reasonable? Is the property easy to inspect, value, and finance? Is it divisible? Is the title and transfer path clear enough that the next buyer does not feel trapped?

If the buyer pool is only a handful of niche industrialists, exit risk is high.

The next-lender test

This is the bankability test. It is brutal, but useful.

If a Tier-1 lender is uncomfortable funding the next buyer, liquidity is weak. Period.

In the 2025 lending environment described in the dossier, lenders prefer stronger DSCR profiles and usually operate around 65% to 75% LTV bands depending on asset quality and borrower profile. If the property has documentation gaps, weak lease structure, thin cash flow support, or authority-side uncertainty, the loan becomes harder. That immediately shrinks the buyer pool.

The forced-sale test

This is the honesty test.

If you had to sell in six months, who would buy it? A broad local market? A few specialized users? Only one broker’s network? Or only a cash buyer looking for distress pricing?

The narrower the answer, the higher the exit risk.

How do Navi Mumbai industrial belts differ in liquidity and vacancy behaviour?

Area matters, but only when explained through occupier depth and use-case fit.

TTC-side belts and older industrial clusters with broader user depth

TTC-side industrial belts generally benefit from a wider industrial and business base. IT, engineering, service-linked industrial use, and mixed occupier depth can support better liquidity in the right stock.

But this is not a free pass. The dossier flags a local jurisdictional issue: taxation or control friction between NMMC and MIDC can create industrial climate stress in parts of the TTC-side environment. That kind of administrative friction can affect business comfort and therefore influence vacancy and exit behaviour.

So TTC-side stock can offer broad user depth, but buyers should not ignore local jurisdiction and cost conditions.

Taloja-side stock where use-case fit and compliance matter heavily

Taloja is one of the most discussed industrial belts because it serves manufacturing, logistics, and growth-linked users. The ASR-linked industrial rate bands in the dossier place Taloja and Additional Taloja roughly in the ₹12,100 to ₹15,460 per sq mtr range as official valuation anchors, though real market behaviour depends on exact pocket, access, and asset type.

Taloja can offer strong opportunity, but it is not one clean answer. MPCB category, process compatibility, internal access, power, and technical specs matter heavily here. A broadly usable Green or White category unit may behave very differently from a specialized Red-category setup.

In simple terms, Taloja rewards correct fit. It can punish lazy buying.

Kalamboli and Panvel-side logistics-oriented demand

Kalamboli and Panvel-side industrial and warehouse demand is more logistics-oriented in many pockets. This can support liquidity for the right large-format warehousing, especially where highway and freight logic are strong.

But logistics property is not just about “near airport” or “near port” marketing. The actual warehouse must match logistics standards. Height, docks, apron space, truck flow, and turnaround matter. If the asset misses those basics, the belt alone will not save it.

The dossier places Panvel and New Panvel around ₹12,500 to ₹15,000 per sq mtr as official valuation anchors in the relevant authority context. Again, that is not a promise of liquidity. It is just a reference base.

Dronagiri or port-influenced belts where the buyer pool can become narrower

Dronagiri and similar port-influenced areas can make sense for specific logistics and port-linked strategies. Their official value anchors may look cheaper, with the dossier noting roughly ₹7,000 to ₹9,000 per sq mtr in the CIDCO context.

But cheaper does not always mean easier to exit.

These belts can become narrower in buyer pool because the use case is more specialized and the demand story is not as universal as a broad SME industrial cluster. If the property depends too heavily on one logistics narrative or one future catalyst, buyers should be more careful.

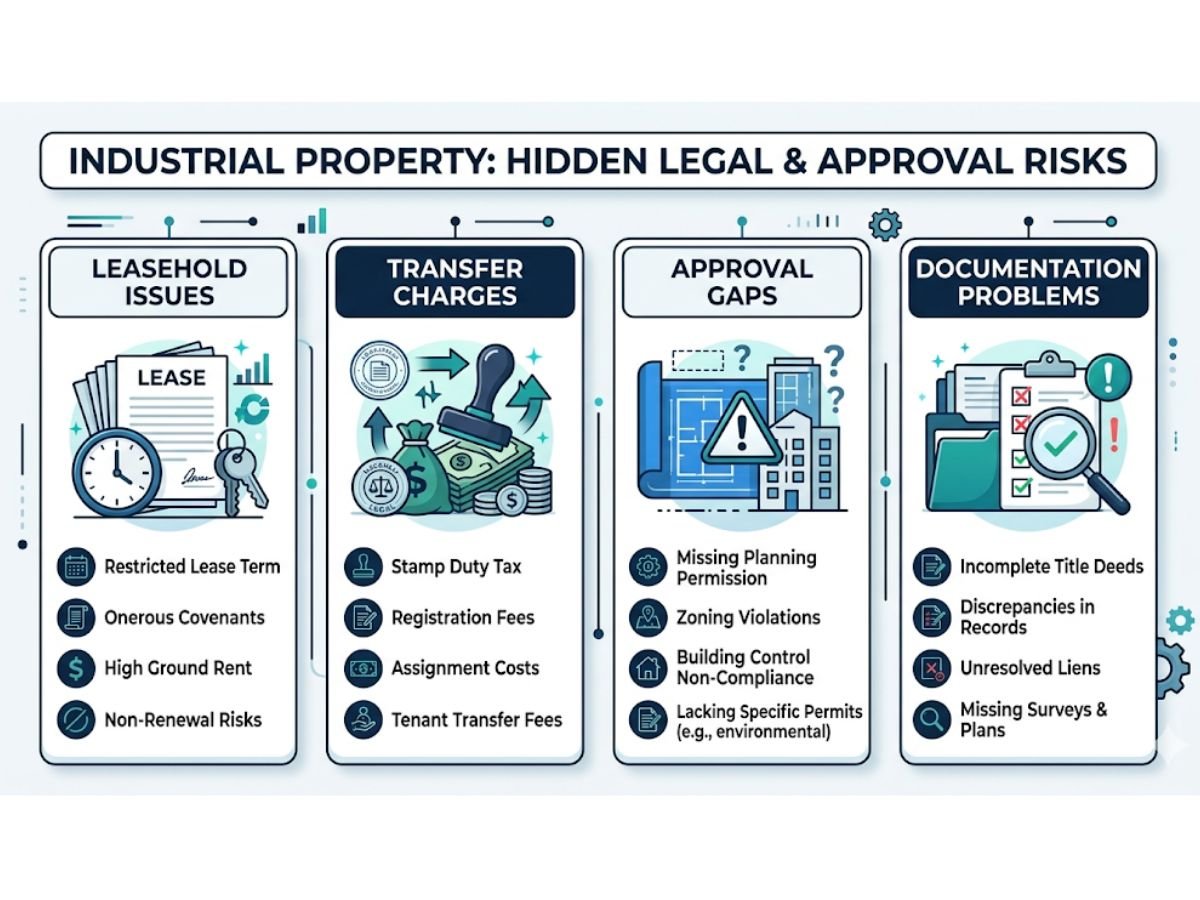

Which legal, leasehold, and approval issues can quietly damage liquidity?

Some industrial properties do not fail because of market demand. They fail because paperwork kills momentum.

MIDC or authority-side conditions that affect transfer, use, or bankability

MIDC-linked property can carry real transfer and utilization discipline. The dossier notes that non-utilization can trigger meaningful yearly charges, and that incomplete utilization or delayed production can become a resale friction point.

Lease balance also matters. If the remaining lease term becomes too short, lender comfort can fall. That can reduce bankability and directly hurt liquidity.

CIDCO leasehold and transfer-charge issues where relevant

CIDCO-linked industrial property must be treated carefully as leasehold-led stock unless a specific legal change clearly says otherwise. Buyers should not confuse residential freehold discussions with industrial reality.

The 2025-2026 CIDCO transfer charge structure is a serious cost layer. For industry or warehousing in developed nodes, the dossier notes:

- up to 200 sq mtr: about ₹3,22,100

- up to 500 sq mtr: about ₹6,40,200

- above 500 sq mtr: about ₹9,61,600

In other nodes, the charges are somewhat lower, but still meaningful. These are not small numbers. They affect affordability, negotiation, and exit friction.

Sanctioned use mismatch, loading mismatch, or documentation gaps

This is one of the biggest hidden risks in industrial resale.

If the marketed use and sanctioned use do not align, or the property is physically unsuitable for the claimed use, buyers and banks hesitate. The same happens when fire readiness, BCC, or building documentation is incomplete. The seller may call these “minor issues.” The market usually does not.

When MahaRERA matters and when it does not

MahaRERA does not apply to every industrial asset. But where the stock is part of a newer registered industrial park or industrial project, it can matter. In such cases, project status, timelines, possession reality, and promoter transparency can improve buyer comfort.

For older resale industrial units, the relevance may be limited. The key is to use MahaRERA where it genuinely applies, not as decorative credibility.

Is higher yield worth it if exit and vacancy risk are worse?

Usually, for small and mid-size investors, no.

A higher yield is only useful when it comes from true demand. If the yield exists because the property is harder to move, harder to finance, or harder to re-lease, then that extra return is often just risk compensation.

A specialized chemical or process-heavy unit may show 8% to 10% yield potential in some cases, while a more generic logistics or industrial gala may sit around a lower but steadier band. For many private buyers, the second option is healthier because downtime risk is lower and exit quality is better.

This is the real comparison:

- stable moderate yield with broad demand

- versus higher headline yield with narrow demand and slower exit

Most investors think they are choosing between returns. In reality, they are choosing between stress levels.

Who should buy lower-risk industrial stock, and who can tolerate higher-risk stock?

Different buyers can tolerate different kinds of risk. The mistake is buying a higher-risk asset with a lower-risk mindset.

| Buyer profile | Better fit | Why |

|---|---|---|

| Conservative investor | Compact gala, broadly usable built-up unit, cleaner title, active lender comfort | Lower downtime, wider resale pool, easier to understand |

| Active investor with leasing patience | Older shed or under-optimized property that can be improved | Can create value through better specs, better leasing, better compliance positioning |

| Self-use buyer with long holding horizon | Operationally strong asset with future resale flexibility | Can prioritize current use, but should still keep divisibility and bankability in mind |

| Speculative appreciation buyer | Bare plot or niche future-growth stock only with clear strategy | Highest risk if approvals, utilization, or market timing go wrong |

What should you ask the seller, broker, tenant, and banker before committing?

This is the due-diligence layer that saves real money.

Ask the seller

- What is the exact authority context: MIDC, CIDCO, private, or mixed?

- Is the property leasehold, and what is the balance lease period?

- Are all transfer charges, premiums, or NOCs fully understood and disclosed?

- Is the sanctioned use fully aligned with the marketed use?

- Is there any pending non-utilization issue, title issue, or documentation gap?

Ask the broker

- What rent has actually been achieved nearby, not just quoted?

- How many months did recent similar units take to lease or sell?

- Which occupier categories are realistically active in this exact pocket?

- Is the buyer pool broad or mainly niche?

- Are banks comfortable funding similar properties here?

Ask the current or past tenant

- What operational problems did they face?

- Was power sufficient?

- Was truck movement practical every day?

- Were there any delays from fire, consent, access, or local authority processes?

- If they are leaving, why are they leaving?

Ask the banker

- Is the asset financeable in its current legal and physical condition?

- Are there any authority, lease, tenure, or document issues that may affect sanction?

- What LTV is realistically possible here?

- Would a future buyer face difficulty because of ticket size or property type?

- Are there conditions that may reduce valuation or loan eligibility?

conclusion

Exit risk, vacancy risk, and liquidity in industrial property are really questions about failure planning. Not success planning.

If everything goes right, many industrial assets look fine. The smarter test is what happens when things go wrong. The tenant leaves. The bank becomes strict. The buyer pool shrinks. Transfer cost rises. The property has to be sold faster than expected.

In that situation, the better asset is usually not the one with the loudest yield story. It is the one with broader usability, cleaner paperwork, stronger bankability, better movement logic, and a wider next-buyer pool.

For most small and mid-size buyers in and around Navi Mumbai, the lower-risk choice is usually a practical, compliance-clean, correctly sized industrial unit in a belt with real occupier depth. The risky choice is often the asset that looks cheap, looks big, or looks high-yield, but depends on too many things going exactly right.

That is the core rule worth remembering: buy industrial property that can still work when your first plan fails.

FAQs

Frequently Asked Questions