Data Center Growth and Industrial Land Competition in Navi Mumbai

Data center growth is changing industrial land competition in Navi Mumbai, but not in one broad, citywide way. The real pressure is concentrated in select TTC-side pockets like Rabale, Ghansoli, Mahape-side influence zones, and parts of Airoli where power, fiber, and campus-scale feasibility actually exist. That is the first thing to understand. Buyers should not pay a data center premium unless the plot has real infrastructure fit, clean title logic, and genuine large-format utility.

A lot of the confusion starts because news about Navi Mumbai’s data center boom is true, but it gets stretched too far. Mumbai holds a dominant share of India’s data center capacity, and Navi Mumbai is one of the biggest reasons for that position. Operators and developers like NTT, Sify, and Digital Edge already have large live or planned campuses here. But that does not mean every industrial plot from TTC to Panvel suddenly deserves a tech-infra premium.

Data center growth is changing industrial land demand in Navi Mumbai, but not everywhere equally

The simple answer is this: data centers are acting like a selective land filter, not a blanket industrial boom.

| Micro-market | What it suits better | Competition pressure |

|---|---|---|

| Airoli / Rabale | Corporate IT support, hyperscale-ready infra, enterprise-grade campuses | Very high |

| Mahape / Ghansoli | Hybrid tech-infra, larger-format campuses, power-heavy use | High |

| Taloja / Panvel-side belts | Warehousing, logistics, heavier industrial and outward migration demand | Moderate, but rising for different reasons |

| Random outer parcels marketed as future DC land | Mostly story-driven, not automatically suitable | Often overstated |

What changed is not just sector demand. What changed is who can pay for land. Hyperscale and institutional players can underwrite land differently from a normal warehouse user or light industrial occupier. That is why landowners in strong TTC-side pockets are now pricing plots around digital-infrastructure potential, not only around traditional factory or warehouse use.

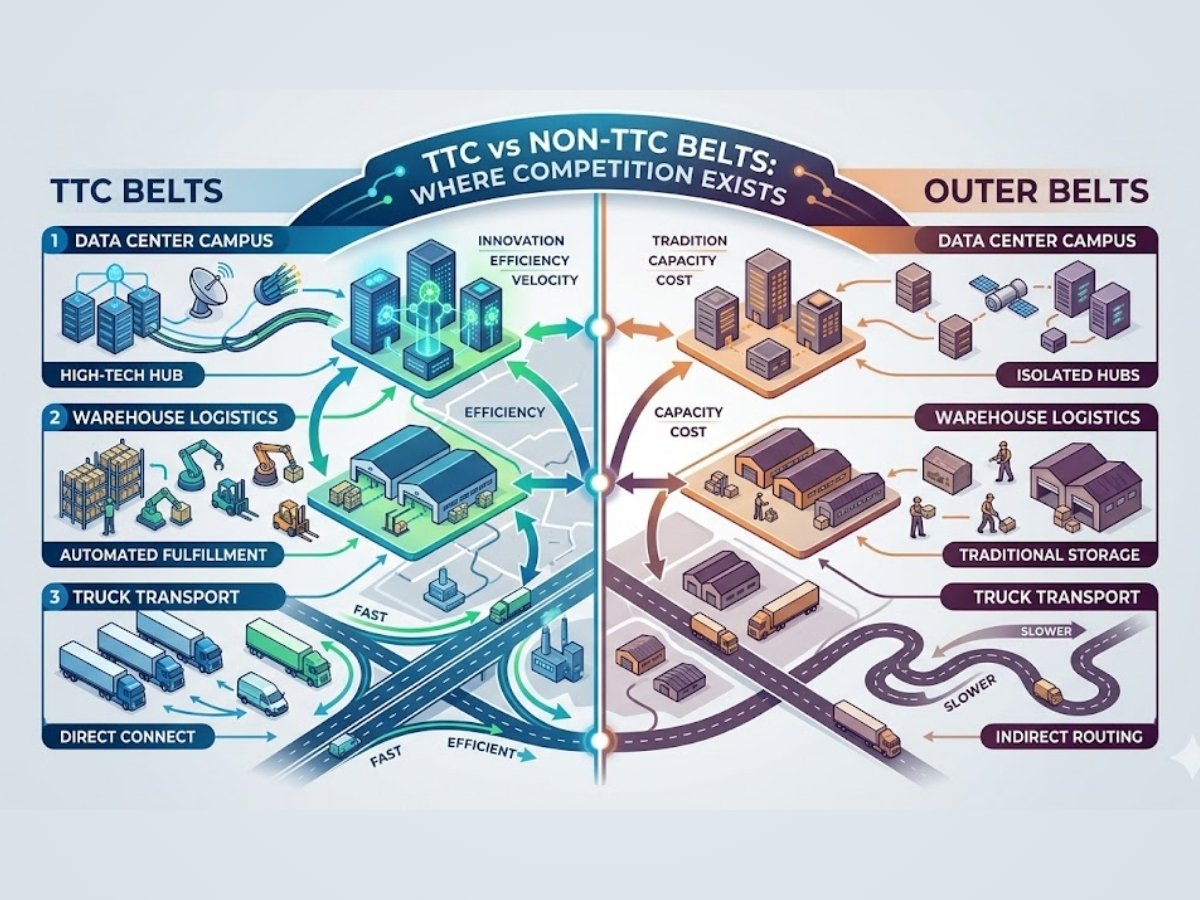

At the same time, Navi Mumbai is not one uniform industrial geography. The TTC belt has a very different logic from Taloja or Panvel-side land. TTC is power-and-network sensitive. Taloja and Panvel are more about logistics, truck movement, expansion room, and industrial economics. Mixing these two stories creates bad buying decisions.

Why does data centre demand compete so aggressively for only certain industrial plots?

Because hyperscale data-center land is rare. Industrial zoning alone is not enough.

Why power depth matters more than broad industrial status

A normal industrial user may manage with standard industrial power. A serious data center cannot. Real hyperscale campuses need a very different power environment, often tied to 110 kV or 220 kV ecosystem strength, not just standard three-phase supply. That immediately tells you the gap between a regular industrial plot and a real hyperscale-ready plot.

This is where many buyers get misled. They hear industrial plot and assume power can always be scaled later. In reality, grid connectivity and high-voltage access are not simple afterthoughts. If a site does not have a practical path to serious utility depth, its data center potential may remain only brochure language.

Why fiber ecosystem changes land value

Carrier-neutral, low-latency connectivity matters. So the premium is not only about land area. It is also about whether the site can function inside a real digital-infrastructure ecosystem with redundant network paths and practical connectivity depth.

Why larger contiguous parcels behave differently

This is one of the most ignored points in the market. Small industrial plots may still be useful industrially. But they are usually weak candidates for true hyperscale or multi-building data center campuses.

That is why competition gets aggressive only for plots that combine power, fiber, parcel size, and execution feasibility. Not for every 500 or 1,000 sq m parcel carrying an industrial tag.

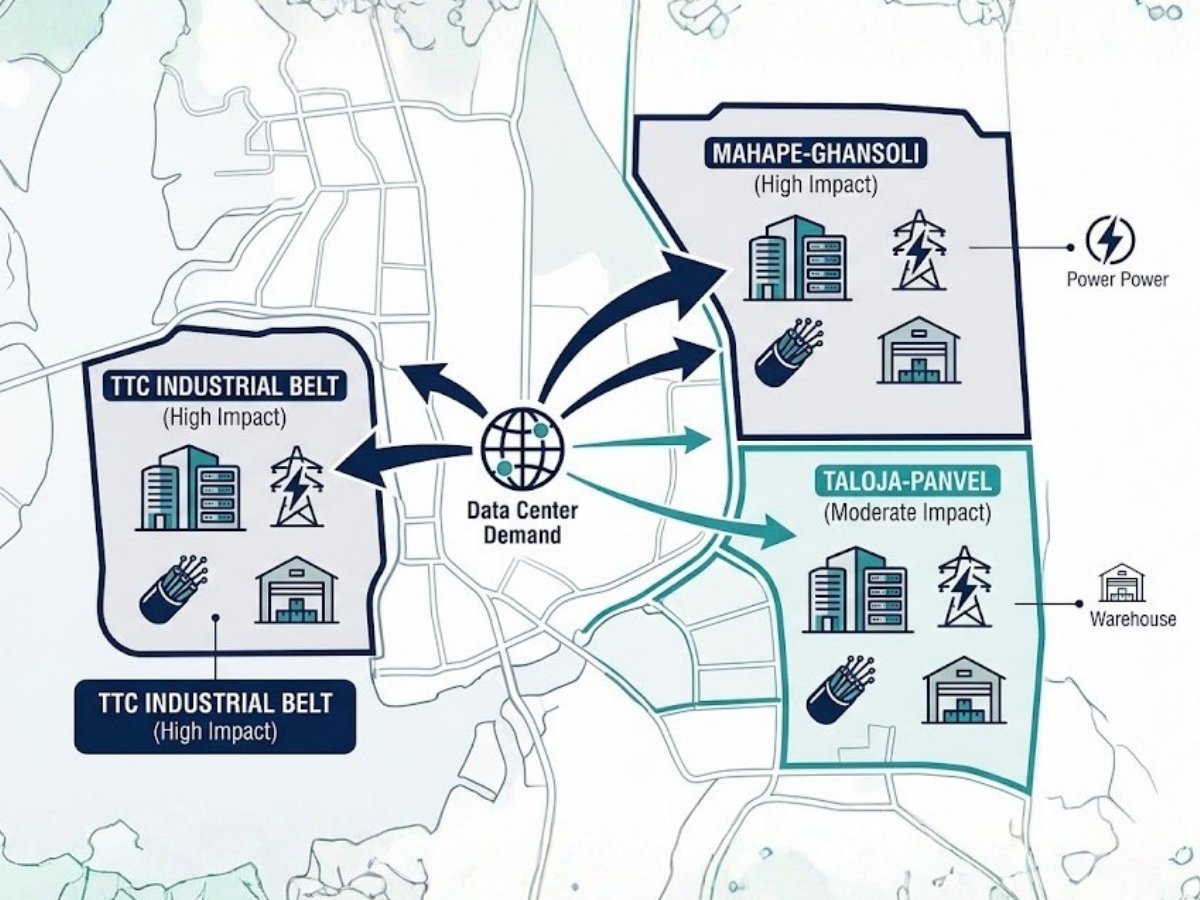

Which Navi Mumbai belts actually face real data-centre-led land competition?

The strongest real competition sits in the TTC-side ecosystem, not across all of Navi Mumbai.

Airoli and Rabale

Rabale is the clearest hyperscale-grade example because the infrastructure logic is already visible on ground. Airoli is slightly different. It fits more comfortably into corporate-tech, enterprise-support, and polished IT-linked environments, but it still benefits from the same broader TTC ecosystem. So Airoli can participate in the data center narrative, but Rabale is usually the heavier infrastructure benchmark.

Ghansoli and Mahape-side influence

Ghansoli and Mahape-side belts matter because this is where campus-scale stories are getting bigger. That supports the idea that large-format digital infrastructure is concentrating in this side of the market, not spreading evenly into every industrial node.

Why Taloja and Panvel should not be casually sold on a data-centre story

This is where many articles go wrong. Taloja and Panvel can absolutely rise, but usually because of logistics, warehousing, NMIA influence, highway movement, and industrial outward migration, not because they are natural substitutes for every TTC data-center-grade site. They are different markets with different economics.

That difference matters a lot. If a buyer pays a TTC-style tech premium in a Panvel-side or Taloja parcel without matching utility logic, they may simply be overpaying for ordinary industrial land.

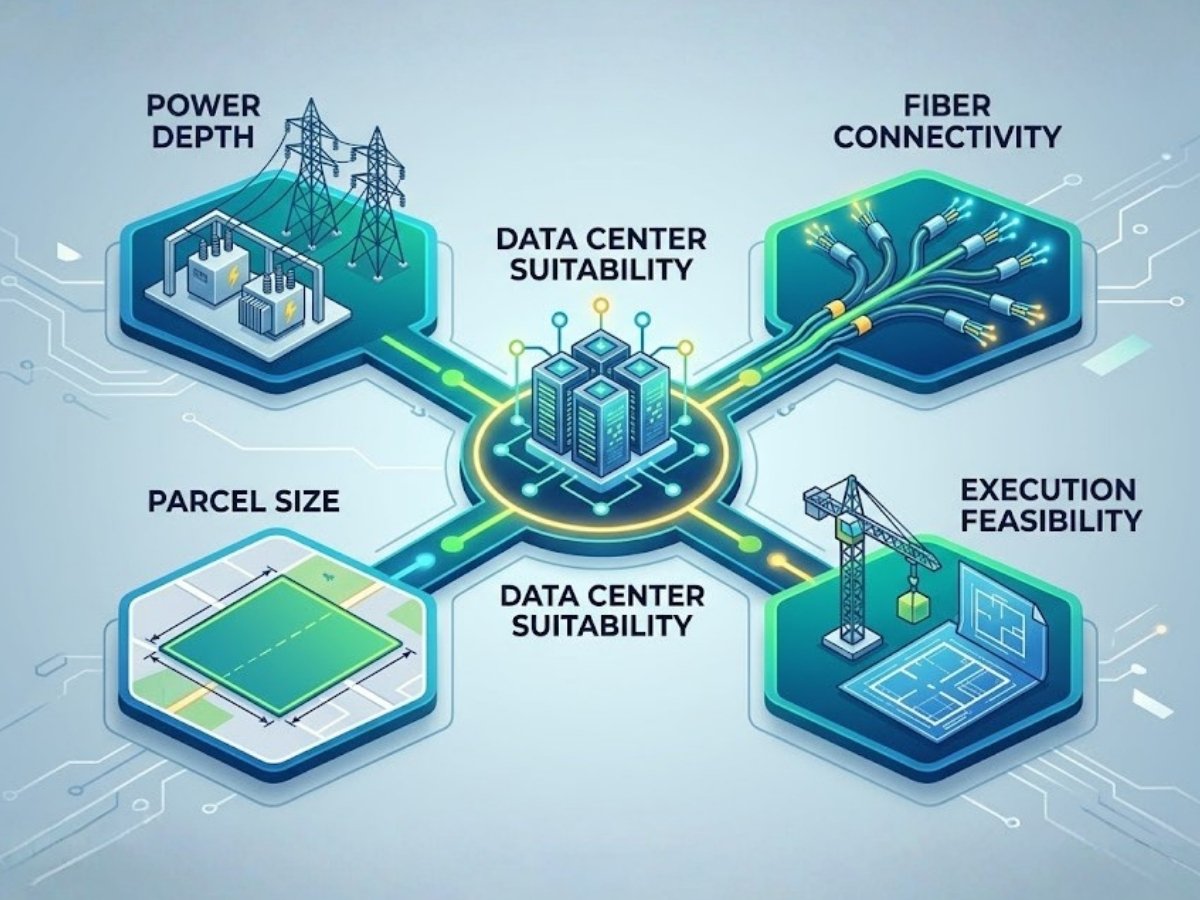

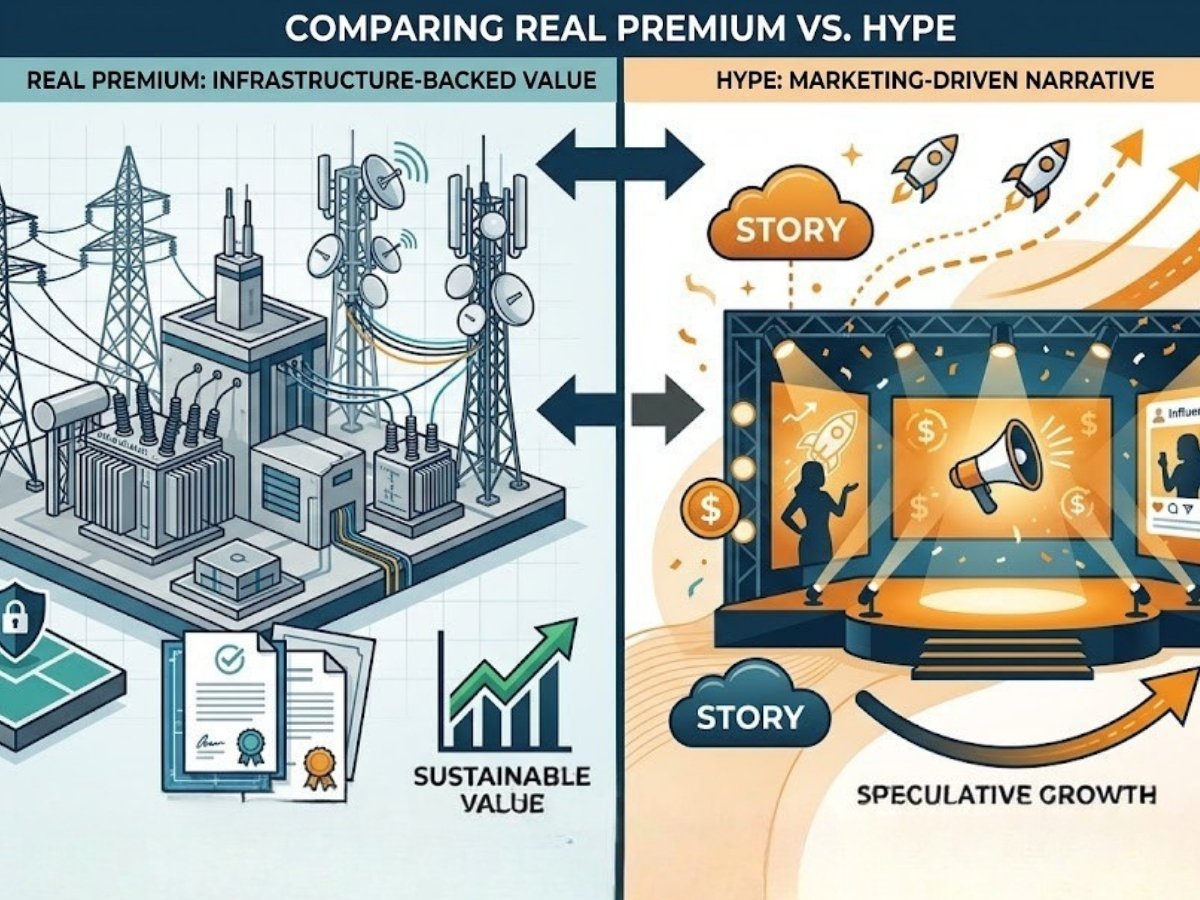

What actually creates a real data center premium on industrial land?

A real premium comes from measurable fit, not from excitement.

Real premium usually needs all or most of these

- Large contiguous parcel, often several acres rather than a small fragmented plot

- Clear industrial title or transfer pathway with manageable compliance burden

- Real access to high-voltage power ecosystem

- Dense, redundant fiber possibilities

- Good logistics access for construction, equipment movement, and operations

- Structural or development feasibility for heavy floor loading and campus services

- A location already inside, or immediately aligned with, a proven digital-infrastructure corridor

Story premium usually sounds like this

- Near a big data center

- Future data center hub

- IT policy allows it

- Industrial plot, so power can come later

- Once airport starts, tech will come here too

That second list is where many investors get trapped.

Policy support for data centers is real. But on ground, policy support does not replace infrastructure reality. A plot may qualify in policy language yet remain commercially weak for a real hyperscale build because power depth, fiber redundancy, size, or cost structure do not support it.

Which industrial land gets overmarketed on data-centre hype?

This answer is blunt: quite a lot of it.

Plots under one acre, awkward parcels, isolated sites with weak approach roads, and land that is merely close to TTC often get marketed as data-center candidates when they are really only conventional industrial plots. The adjacency story sounds strong, but the physical site may still fail on cooling infrastructure, transformer space, setbacks, campus circulation, heavy equipment access, or realistic utility routing.

A common local trap is what can be called the adjacency fallacy. A plot may sit near Rabale or across from a serious data center campus. But if it does not have access to the same power logic, the same fiber trenching practicality, and the same scale, it does not deserve the same premium. That difference is huge.

There is another financial trap too. Authority structure matters. Transfer charges, lease assignment cost, and management change cost can materially change the full acquisition picture. So a plot that looks attractive on headline rate alone may become far less sensible once authority-linked outgo is fully underwritten.

How does this competition affect normal industrial buyers, warehouses, and light industry users?

This is the real second-order story, and weak articles usually miss it.

When TTC-side land starts getting valued around data-center-grade expectations, ordinary industrial users lose negotiating power. A landlord holding a strong Rabale or Mahape-side parcel may prefer to wait for a higher-value infra or redevelopment play instead of locking into a standard warehouse or fabrication user at a normal industrial rent.

That pushes many traditional users outward. In practical Navi Mumbai terms, this is one reason Taloja, Panvel-side belts, and other outward logistics corridors remain important. Their economics still fit warehousing, 3PL, industrial storage, heavier activity, and land-hungry operations far better than premium TTC micro-markets.

So the effect is not only rising land values. It is also spatial reorganisation. High-tech, power-dense use stays concentrated in TTC-side pockets. More price-sensitive industrial and logistics demand keeps moving outward.

Should an investor pay more today because a plot has data center potential?

Usually, no, unless multiple hard conditions line up together.

Open-market expectations for premium TTC plots can be much higher where data-center-grade narratives are active. That is exactly why investors must separate official reference rates, asking rates, and true achieved value.

A simple investor filter

| When paying a premium may make sense | When it is safer to walk away |

|---|---|

| Large parcel, strong TTC-side location, clear title path, power-and-fiber feasibility, real institutional-grade fit | Small or broken parcel, ordinary industrial power, heavy authority-linked transfer burden not properly priced, no real campus logic |

| Buyer has long holding capacity and understands infra risk | Buyer is relying on quick resale to some data center company |

| Plot works even as industrial land if the data-center story weakens | Plot only works if the premium story comes true |

The biggest mistake is underwriting a weak plot as though a hyperscaler is guaranteed to buy it later. That is not investing. That is hoping.

What should a buyer verify before believing any data-centre-led land story?

Use this simple five-point filter before paying even one rupee of premium.

The 5-point data center feasibility test

1. Who controls the plot and transfer process? Check whether the land is under MIDC, CIDCO, or another authority structure. This changes transfer cost, title clarity, and acquisition complexity.

2. Is there real high-voltage power feasibility, not just normal industrial power? A serious data center story without strong power logic is weak from day one.

3. Can the site support redundant fiber entry and real network connectivity? Not just fiber available in the area, but realistic, diverse entry-path potential.

4. Is the parcel large and workable enough? Small plots usually fail campus logic, support infrastructure needs, and future expansion.

5. Does the plot still make sense as ordinary industrial land? This is the safety question. If the data-center story disappears, can the asset still hold value and find a user?

This is also where the MIDC vs CIDCO divide matters. State policy support for data centers is one side of the story. Transfer cost and authority burden are the other side. If a buyer ignores those two together, the underwriting is incomplete.

Who benefits most from this trend, and who should stay cautious?

The biggest winners are usually:

- landowners already holding large, usable parcels in strong TTC-side locations

- institutional or deep-pocketed buyers who can wait, aggregate, and solve infrastructure issues

- owners whose land already sits near real power-and-fiber ecosystems

The people who should stay most cautious are:

- small investors buying tiny plots only because they heard data center is coming

- warehouse operators trying to renew or buy in premium TTC pockets without tech-level margins

- buyers treating all Navi Mumbai industrial land as part of the same boom

In plain words, this is not a small-ticket gold rush. It is a capital-heavy, infrastructure-driven market.

Conclusion

Data center growth is making Navi Mumbai industrial land more competitive, but only in a narrow, infrastructure-backed way. The real winners are not all industrial plots. The real winners are select TTC-side parcels with serious power, fiber, scale, and title clarity. Everyone else needs to stay disciplined.

So the correct way to read this market is simple: selective premium, selective fit, selective risk. If a plot does not clearly pass that test, underwrite it as ordinary industrial land and nothing more.