MIDC Plot Transfer and Permissions in Maharashtra: What Navi Mumbai Buyers Should Check Before Buying

MIDC Plot Transfer and Permissions in Maharashtra is not a normal property purchase. You are not simply buying land or a shed. You are buying into an MIDC leasehold file that needs transfer approval, correct documents, updated dues, and a use case that MIDC and related authorities can actually support. For Navi Mumbai buyers looking at Taloja, TTC, or Panvel-side industrial stock, this matters before token, not after.

That is the real answer.

A clean-looking industrial deal can still become expensive or unworkable if the seller cannot show the right MIDC records, if the structure is not backed by a proper Building Completion Certificate, if the asset is mortgaged, or if your proposed activity does not fit the plot’s regulatory and environmental reality. MIDC itself treats transfer, subletting, change in name, and change in use as separate matters, not as one loose “handover” process.

The short answer: what Navi Mumbai buyers should understand before buying an MIDC property

| What to understand | What it means for the buyer |

|---|---|

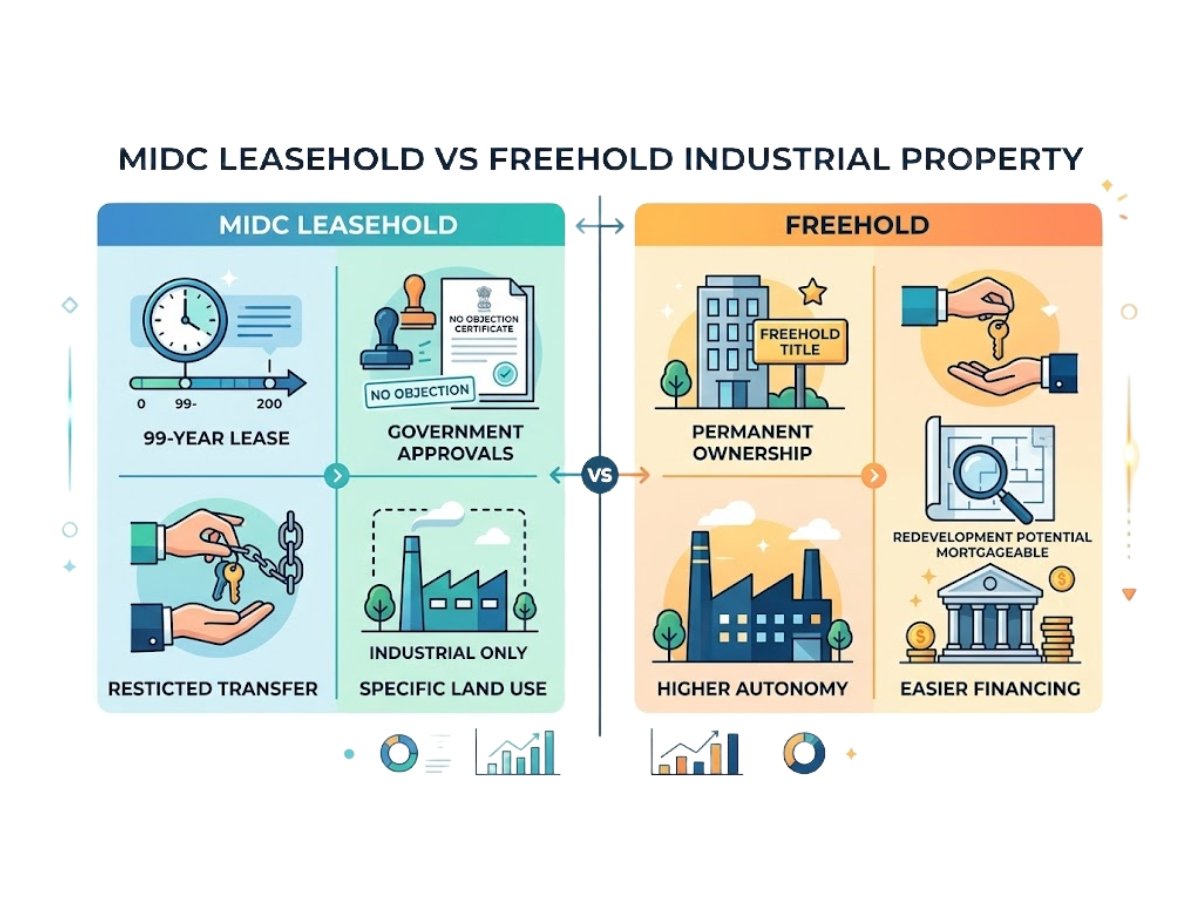

| MIDC property is usually leasehold, not ordinary freehold | The seller cannot treat the deal like a simple open-market sale. MIDC approval and compliance history matter. |

| Transfer needs a specific document stack | MIDC’s Citizen Charter and service pages show transfer-related requirements such as request applications, DPR/project profile, BCC in transfer cases, no-encroachment certificate, and other supporting records. |

| Mortgage changes the transaction | If the property is charged to a bank or financial institution, NOC and finance-side clearances become central. |

| Activity fit matters separately from title | Even if transfer is possible, your intended production or use may still need separate change-in-use or regulatory approvals. |

| Open plot and early-period restrictions matter | MIDC’s land-allotment guidelines state that no permission will be given for transfer or subletting of the plot for the next 5 years from allotment, and change of use is also restricted in that period. |

| Navi Mumbai buyers must check local ground reality too | In belts like Taloja and TTC, site usability, encroachment, municipal dues, and environmental fit can change the answer. |

The practical takeaway is simple. Do not release a heavy token just because the seller shows one lease deed copy or one old approval. In MIDC deals, the real risk sits in the missing papers, the wrong classification, and the gap between what is legally transferable and what is actually usable.

Why an MIDC transfer is not the same as buying an ordinary industrial property

An ordinary industrial property deal usually starts with title, possession, and price. An MIDC deal starts one layer deeper. You must ask whether the leasehold rights can be transferred in the way the seller is proposing, whether MIDC records support the present structure on ground, and whether the buyer’s intended use fits the plot’s regulatory framework.

This difference is not theoretical. The Bombay High Court recently described an MIDC plot as a long-term 95-year leasehold arrangement and noted that the rights under the lease were transferable in terms of the lease clause before it held that assignment of such leasehold rights was not a taxable supply of service in that case.

That matters because it shows the basic nature of what is being bought. You are not stepping into a simple freehold sale. You are stepping into a long-term leasehold position that remains tied to MIDC’s conditions, permissions, and file history. MIDC’s own customer portal separates transfer, sub-letting, change in name of company, and permission for change in land use into different application tracks.

In Navi Mumbai industrial markets, that difference becomes even sharper. Private industrial freehold options are limited and expensive in many practical belts, so buyers often move toward MIDC stock because the infrastructure base is stronger. But that infrastructure advantage comes with process discipline. Power, roads, industrial planning, and cluster logic may be better, but the file cannot be casual.

In which cases does MIDC transfer permission become the real deal-breaker?

Not every MIDC deal carries the same risk. Some cases are much more sensitive than others.

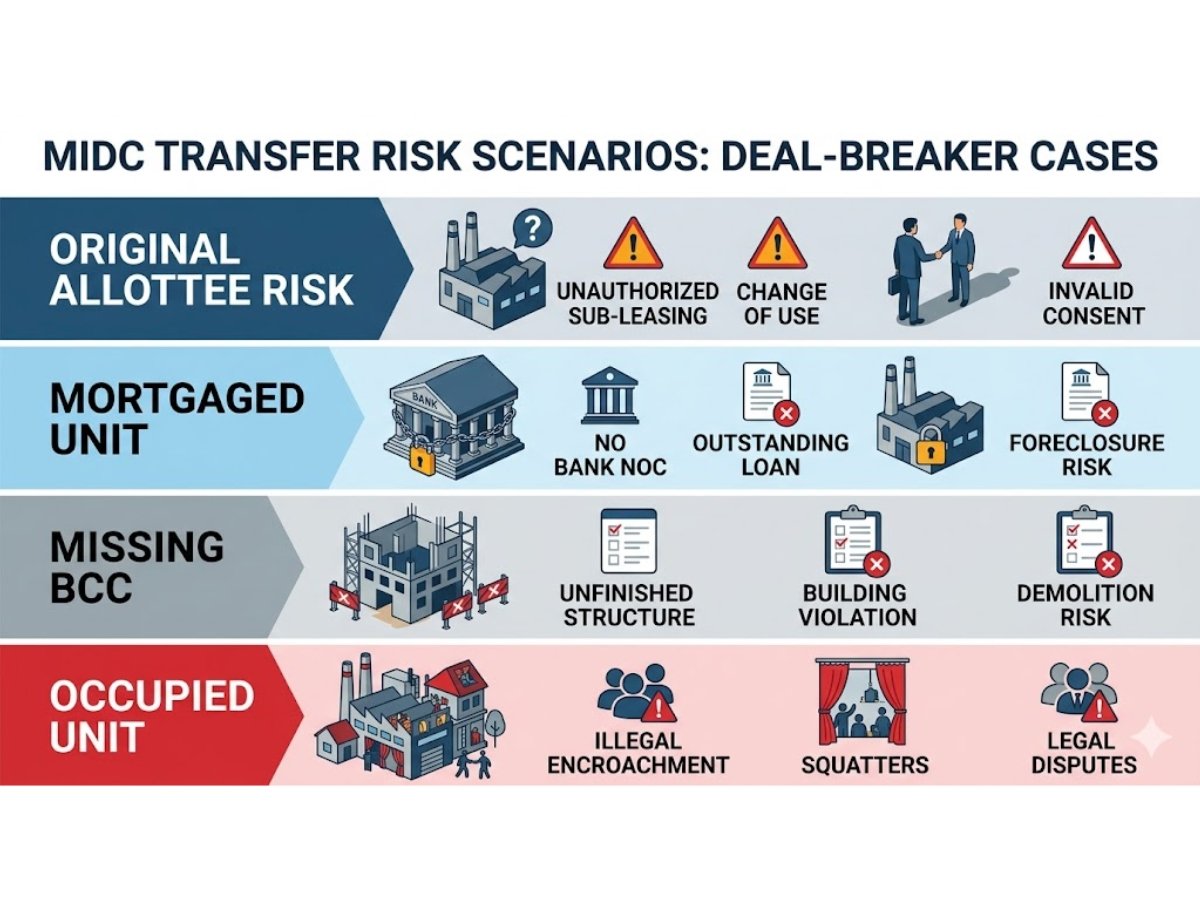

Buying from the original allottee

This is where many first-time buyers get overconfident. MIDC’s land allotment guidelines say no permission will be given for transfer of plot and for subletting of plot for the next 5 years from the date of allotment, and change of use is also not allowed in that period. The same document also says the plot holder has to obtain the Building Completion Certificate within 2 years from possession.

So if someone offers you an “early exit” open plot deal, your first reaction should be caution, not excitement.

Buying a built-up shed or gala

A built-up asset is not automatically safer. MIDC’s own documentation repeatedly treats the Building Completion Certificate as an important transfer-side document. The Citizen Charter lists BCC in transfer cases, and the related service page for industrial registration in transfer cases also lists the BCC together with lease deed or deed of assignment, project profile, and latest electricity bill.

That is why buyers should not confuse an approved plan with a completed and regularized structure. On ground, the seller may show a usable shed. On file, MIDC may still want stronger completion backing.

Buying a mortgaged or bank-financed unit

This is a common industrial-market trap. MIDC’s Citizen Charter separately lists the documents required for permission to mortgage a plot to a financial institution: request application, board resolution where applicable, loan approval letter, no-dues certificate, and NOC from the earlier financial institution if the plot is already mortgaged.

In practical buyer language, this means one thing: if a bank is already sitting on the asset, you cannot behave as if the seller alone can clear the deal.

Buying a running factory with an occupier already inside

If the unit is occupied, ask whether the present arrangement is lawful transfer, lawful subletting, or just an informal possession story. MIDC’s customer portal clearly treats transfer and sub-letting as different legal routes. MIDC’s sub-letting application page says sub-letting is permitted on payment of charges, that charges are payable in advance, and that sub-letting is allowed up to 10 years.

So if a broker casually says, “same thing hai, factory chal rahi hai,” do not accept that line. Running possession and legal status are not the same thing.

What documents should a buyer ask for before paying token on an MIDC plot, shed, or gala?

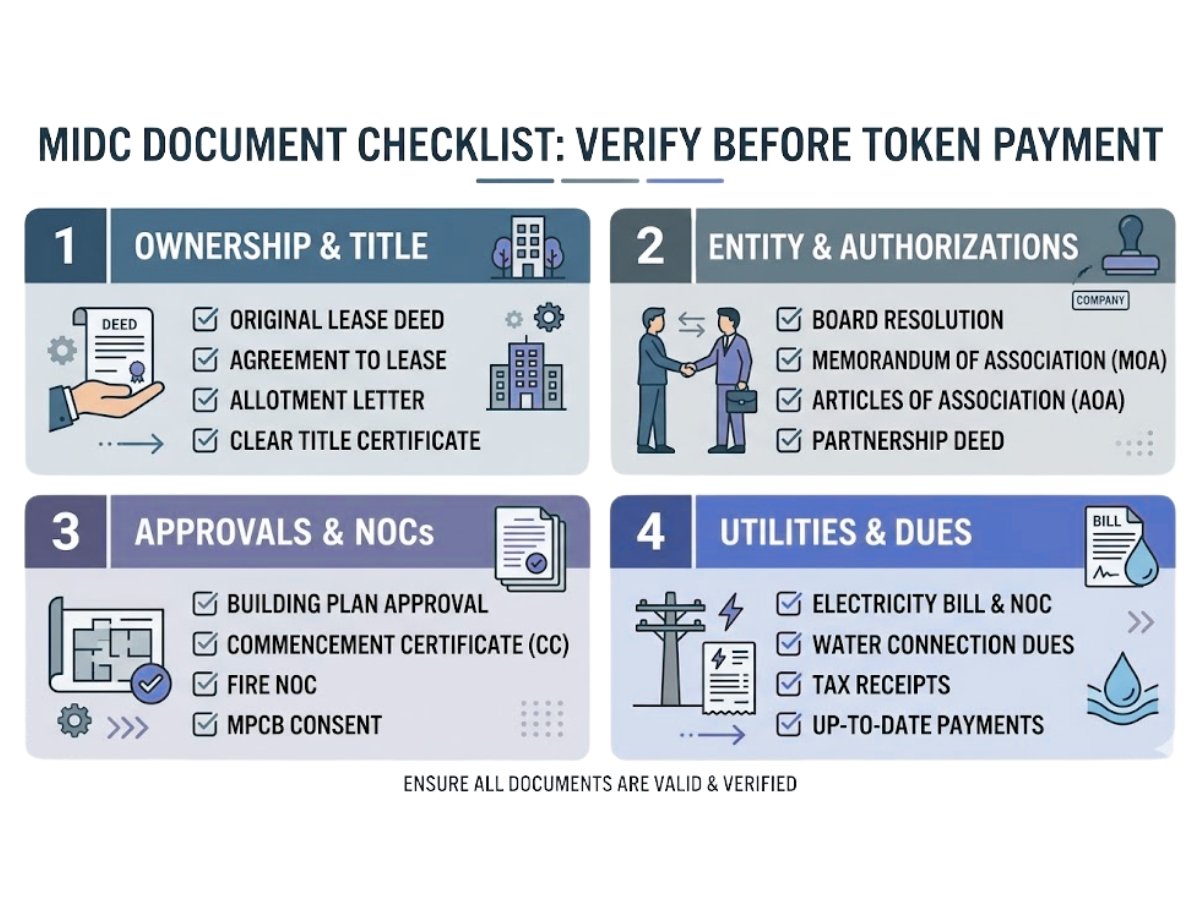

Before token, the buyer should ask for the core MIDC file, not just sale-side comfort papers.

Minimum practical document checklist before token:

- Copy of the original MIDC lease deed

- Copy of the latest deed of assignment if the property was transferred earlier

- Building Completion Certificate if the seller is selling a built-up asset

- Transfer order where relevant in the chain

- Buyer-side and seller-side request applications / resolutions where applicable

- Detailed Project Report / project profile, especially where MIDC wants product, manufacturing process, and raw-material clarity

- No-encroachment certificate and related NOC from the Executive Engineer / Deputy Engineer / SPA, MIDC

- Latest electricity bill

- Latest lease-rent / no-dues status

- Bank NOC if the property is mortgaged

- Basic proof of any name change / constitution change / partnership retirement history if the seller entity has been restructured over time

This is not guesswork. MIDC’s Citizen Charter says transfer of plot/shed/shop requires, among other things, the original plot holder’s request application, the request application of the transferee, the prescribed application form, DPR of the transferee, and NOC plus no-encroachment certificate from the Executive Engineer / Deputy Engineer / SPA, MIDC. The Citizen Charter also separately shows transfer-case documentation such as transfer order, project report, and BCC. The SWC service page for transfer-case registration further lists BCC, lease deed or deed of assignment with registration receipt, project profile clarifying products and manufacturing process, and latest electricity bill.

The practical lesson is even more important than the document list: ask for these papers before money moves. In industrial deals, the cost of discovering a missing file after token can be much higher than in ordinary residential transactions.

What permissions, NOCs, and clearances usually matter in an MIDC transfer?

A buyer should not lump all approvals into one bucket. Different permissions solve different risks.

MIDC transfer approval

This is the foundation. Without proper MIDC transfer handling, the rest of the transaction can remain stuck regardless of private agreement terms. MIDC publicly lists “Application for Transfer” as a separate land-department service.

Bank or financial-institution NOC

If the plot is mortgaged, finance-side consent matters. MIDC’s own charter requires lender-related documents for mortgage matters and NOC from the previous financial institution where relevant.

No-dues and lease-rent status

MIDC repeatedly asks for no-dues support in its processes. For mortgage permission, the Citizen Charter specifically lists the no-dues certificate from Executive Engineer / Deputy Engineer / SPA, MIDC. The broader transfer-related paperwork also expects file cleanliness rather than vague verbal assurance.

Building and site-status permissions

If the asset is built-up, BCC matters. If the site is physically compromised, the no-encroachment certificate becomes critical. A buyer should also independently match the actual built form on site with the file position.

Activity or product-fit approval risk

MIDC’s process material makes it clear that product, manufacturing process, and project profile are not side issues. They are part of the compliance logic. MIDC’s change-in-use track separately calls for request application, DPR, and no-dues certificate.

In simple language, title can transfer and operations can still fail.

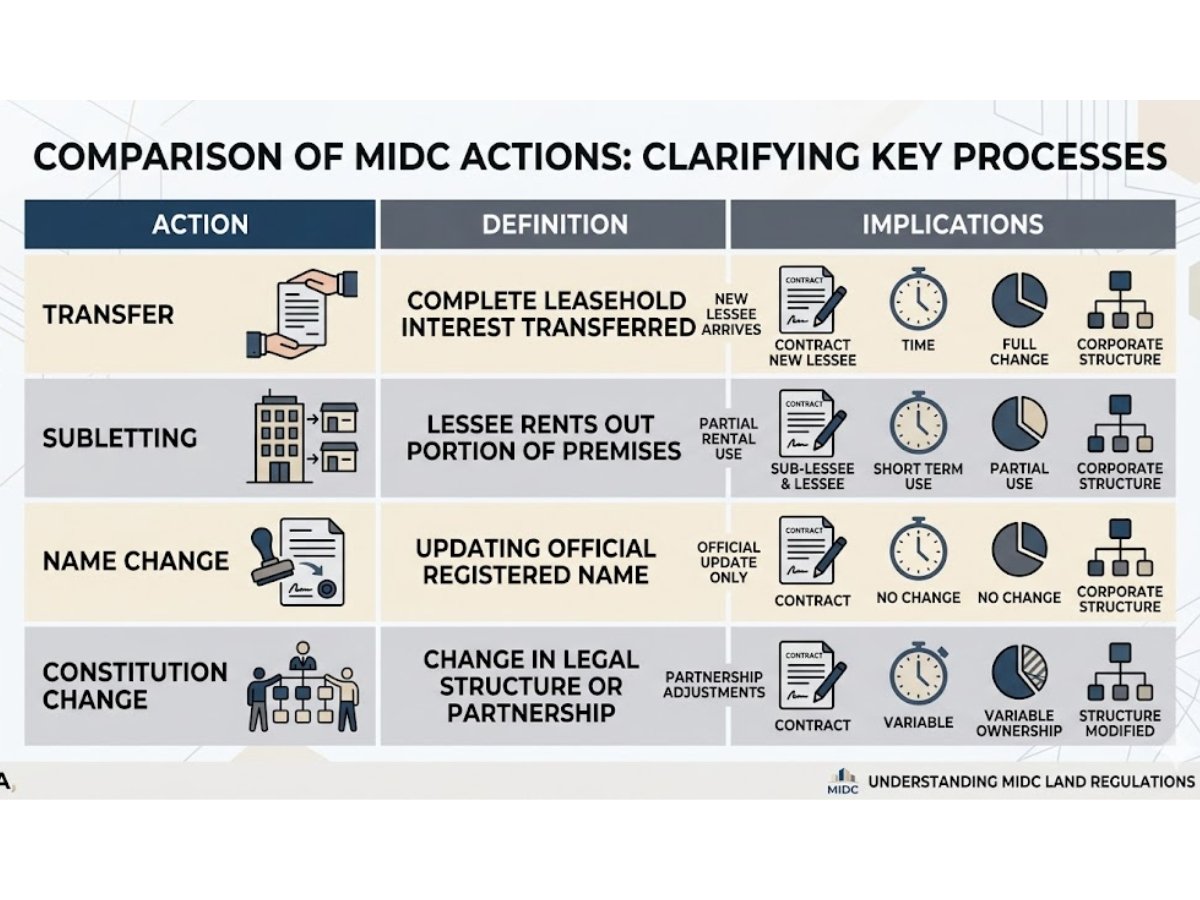

Transfer, subletting, name change, or constitution change: buyers should not confuse these

This is where many industrial buyers lose clarity.

| Action | What it really means | Why the buyer should care |

|---|---|---|

| Transfer | Permanent movement of leasehold rights from one party to another | This is the core sale-side route and needs MIDC transfer handling. |

| Sub-letting | Temporary use arrangement, not a full exit by the original allottee | MIDC treats it separately, allows it up to 10 years, and charges apply in advance. |

| Change in name | Same entity identity issue handled as a separate application path | Buyers should verify it is truly a name change, not a deeper restructuring. |

| Change in constitution / partner structure | Structural change in the business entity | This can change the legal and financial reading of the file, so buyers should not accept loose verbal explanations. MIDC’s registration-related documents explicitly separate “change in name / partner / constitution of company.” |

| Change in land use / activity | Operational shift from one use or product logic to another | This may need a separate approval path even after transfer. |

The big mistake is treating all of these as one “handover” story. They are not the same thing. MIDC itself does not treat them as the same thing.

What practical risks do Navi Mumbai industrial buyers usually miss even when the paper file looks clean?

A file can look fine and still be wrong for the buyer.

The first missed risk is activity mismatch. In Taloja, environmental and industrial-use realities are not abstract. MPCB has a dedicated SRO Taloja office covering MIDC Taloja and Uran Taluka, and public MPCB records also show the Taloja CETP facility at MIDC Taloja.

What does that mean in practice? It means the buyer should not assume any industrial activity can be inserted into any industrial plot just because the seller says “industrial zone hai.” Product profile, process, effluent burden, and consent pathway still matter.

The second missed risk is encroachment reality. MIDC’s Citizen Charter specifically refers to the NOC and no-encroachment certificate from the concerned engineering/planning side. If the plot edge, setback area, or boundary margin is physically compromised, the deal can stall long before the buyer starts production.

The third missed risk is operational suitability. A property can be legally transferable and still fail on access, truck turning radius, loading movement, utility layout, or older built-up design. This is especially relevant in parts of older industrial stock where today’s logistics needs are larger than yesterday’s layouts.

The fourth missed risk is civic-dues blindness. In TTC-side locations, buyers tend to focus only on MIDC and forget municipal exposure. NMMC has an active property-tax system and official payment interface, so civic dues are not a theoretical issue. A practical buyer in TTC should check municipal tax status as well, not just MIDC dues.

How should buyers in Taloja, TTC-linked belts, and Panvel-side industrial markets read MIDC transfer risk differently?

Local reality changes the practical answer.

Taloja

In Taloja, the transfer question is tightly linked to environmental fit. Because MPCB’s Taloja office covers MIDC Taloja and there is an operating CETP presence in the area, buyers should read the deal through a process lens, not just a document lens.

A clean engineering-style shed is not automatically suitable for a more pollution-sensitive manufacturing activity. In Taloja, the wrong use fit can destroy the value of an otherwise attractive deal.

TTC belt: Mahape, Pawane, Turbhe side

Here the biggest mistake is assuming that MIDC file clarity alone is enough. TTC buyers should also check municipal property-tax position with NMMC, because civic-side dues and operational friction matter in this belt.

TTC also has a lot of older running units, mixed occupier patterns, and built-up industrial stock. That means occupier status, subletting history, and actual on-ground usage should be checked much more carefully.

Panvel-side industrial markets

Panvel-side buyers often look for scale, affordability, or overflow-market value. Here the danger is different. Buyers sometimes assume bigger plots or cheaper rates automatically mean an easier transaction. But if infrastructure maturity, activity suitability, or document continuity is weak, the cheaper deal may become the slower deal.

So the local lens is this: Taloja is more activity-sensitive, TTC is more occupier-and-dues-sensitive, and Panvel-side stock often needs stronger maturity and usability scrutiny.

What should happen before token, before agreement, and before final payment?

A disciplined transaction sequence protects the buyer.

Before token

- Verify lease deed

- Ask for BCC if built-up

- Ask for chain of assignment

- Check whether the seller is the real file holder

- Ask for bank status

- Ask for no-encroachment status

- Ask what exactly the buyer’s future activity will be

This stage is about ruling out obvious landmines.

Before draft agreement

- Match the site with the file

- Verify whether the structure on ground matches what is being sold

- Confirm the need for any bank NOC

- Confirm whether the case is really transfer, or partly subletting / constitution / name-change cleanup

- Review project profile and product/process fit

Before major payment

- Ensure the MIDC transfer route being used is the correct one

- Ensure dues position is updated

- Ensure lender-side documents are ready

- Ensure the buyer has checked civic and environmental side issues where relevant

Before possession or operational handover

- Ensure the transfer order and execution path are actually moving

- Ensure no informal occupier issue is being passed on

- Ensure the use case is still feasible for the buyer’s business

A good industrial transaction is not just about “deal done.” It is about whether the buyer can legally and practically start work after the deal.

What are the clearest walk-away signals in an MIDC transfer deal?

Some problems are warning signs. Some are stop signs.

Walk away, or at least freeze the deal, if you see these:

- The seller cannot show a Building Completion Certificate for a built-up property

- The seller is vague about whether the property is mortgaged

- The file history is unclear and prior assignments are not traceable

- The broker says transfer, subletting, and name change are “basically same”

- The plot has visible boundary or access encroachment

- The buyer’s intended activity does not clearly fit the plot’s likely environmental and operational profile

- Municipal dues or MIDC dues are treated casually

- The seller pushes for token before sharing the MIDC file

The biggest red flag of all is resistance to paperwork. In industrial property, hidden reluctance usually means hidden cleanup cost.

Is an MIDC property always better than a non-MIDC industrial option for Navi Mumbai buyers?

No. It depends on what you need.

MIDC property is usually stronger when you need an established industrial ecosystem, clearer industrial planning logic, and infrastructure that is already recognized for industrial use. That is why serious manufacturing and process-led users often prefer it.

But MIDC property also comes with more authority-side process discipline. Transfer, subletting, mortgage handling, change in use, and file history are all more structured. MIDC’s own portals make that visible.

A non-MIDC industrial option may give more commercial flexibility in some situations, but it may create different headaches around land use, approvals, infrastructure, or local planning conditions.

So the better question is not “Which is better?” The better question is “Which risk profile matches my business better?”

Conclusion

For Navi Mumbai buyers, the smartest way to read an MIDC deal is this: do not ask only whether the property can be bought. Ask whether the MIDC rights can be cleanly transferred, whether the structure is properly backed, whether the dues and mortgage position are clean, and whether your business can actually operate there after purchase.

That is the real filter.

In Taloja, the activity and environmental fit can make or break the deal. In TTC, occupier reality, municipal dues, and older industrial stock need sharper scrutiny. In Panvel-side markets, lower entry pricing should not distract you from document quality and operational maturity. A good MIDC purchase is not just a cheaper acquisition. It is a transferable, usable, financeable, and workable industrial position.

If any one of those four layers is weak, the deal is not clean yet.

FAQs

Frequently Asked Questions