Risks of Buying Property in Green Zone: Navi Mumbai Buyer Checklist

Buying property in Green Zone can be risky if you plan to build, resell, mortgage, convert, or develop the land later. Ownership does not automatically mean construction rights. Before paying token money, check zoning, 7/12, mutation entries, IGR records, title chain, NA/development permission, NAINA/CIDCO status, CRZ/CZMP exposure, and MahaRERA registration if it is sold as a plotted project.

Disclaimer: This is an educational guide. Verify the latest position with the relevant authority or a property lawyer before making a transaction.

What Does Green Zone Mean in Maharashtra Property?

“Green Zone” usually refers to land where development is restricted or controlled under a Development Plan, Regional Plan, local planning rules, or environmental regulations.

It is not the same as normal residential land.

In Navi Mumbai, Panvel, NAINA, Uran, Dronagiri, Ulwe, Taloja, Kharghar or Raigad-side areas, a Green Zone plot may be shown as cheap because the buyer may not get normal residential development rights.

The exact status depends on the land’s survey number, village, planning authority, zoning map, revenue records, CRZ status, road access, and development permissions.

Do not rely on broker statements like “Green Zone will become residential soon.” Get written verification.

Why Green Zone Property Looks Attractive

Green Zone land is usually marketed with these claims:

- “Airport ke baad rate double.”

- “NAINA approval will come soon.”

- “CIDCO development is coming.”

- “Farmhouse allowed hai.”

- “Buy now before zoning changes.”

- “Only token now, documents later.”

The problem is simple: future development is not guaranteed.

A cheap plot can become expensive if you later discover that construction is restricted, NA conversion is not available for your intended use, the layout is not sanctioned, or the land is affected by CRZ, mangroves, road reservation, inheritance disputes, or title defects.

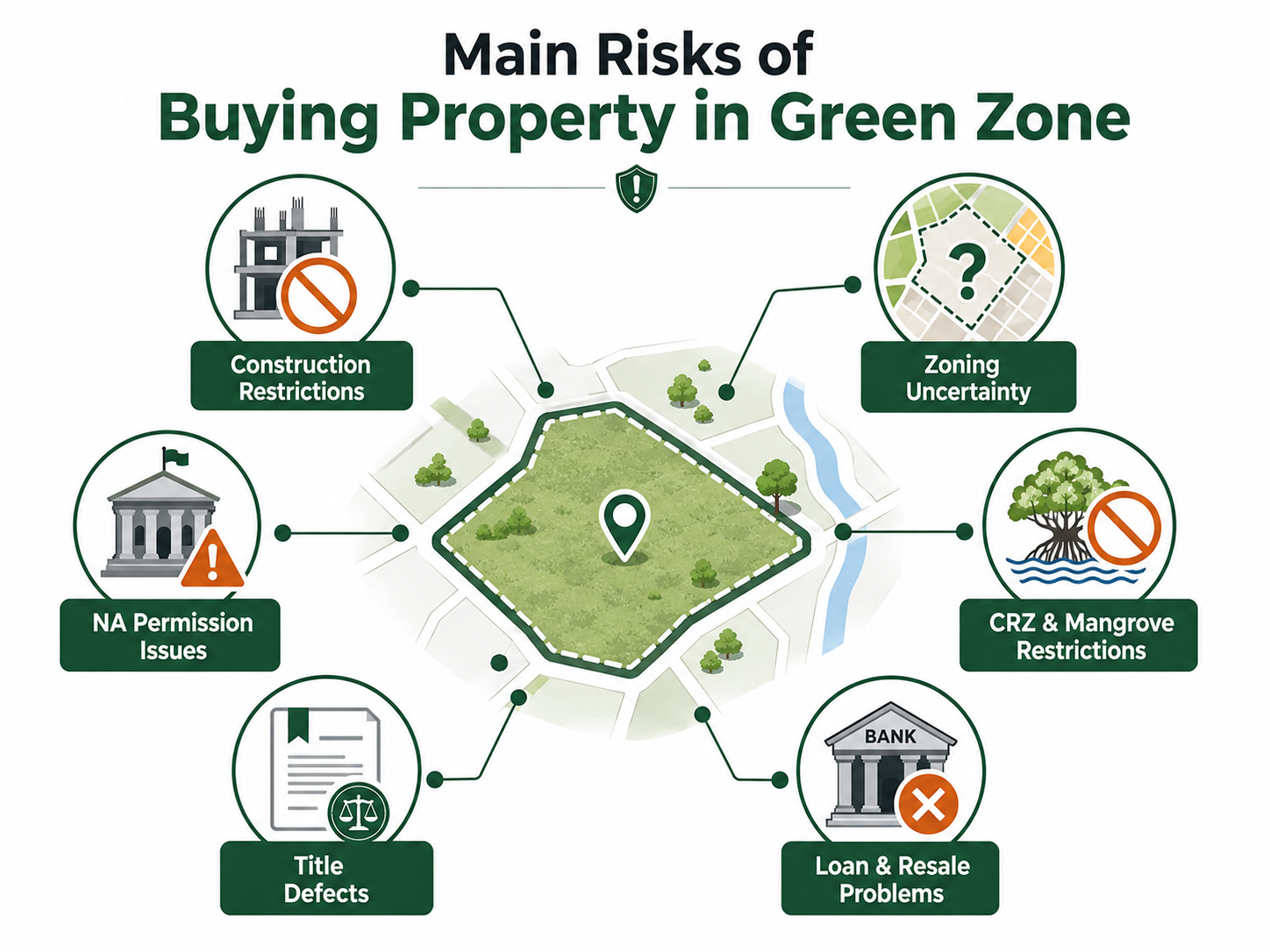

Main Risks of Buying Property in Green Zone

1. You May Own the Land but Still Not Be Able to Build

A sale deed may transfer ownership rights, but it does not automatically give construction rights.

To build legally, you need land-use permission, planning approval, building permission, and compliance with the applicable Development Plan or Regional Plan.

This is the biggest misunderstanding in Green Zone deals.

A buyer sees the 7/12 extract and assumes, “The owner name is there, so the land is safe.” That is not enough.

7/12 supports land-record verification. It does not confirm clean title, construction permission, NA status, zoning safety, or future development rights.

2. NA Permission May Not Be Available for Your Use

NA means non-agricultural use.

Many buyers think agricultural or Green Zone land can easily be converted to NA later. That is unsafe thinking.

Maharashtra’s updated land-revenue process has changed the role of separate Collector permission in certain cases where the proposed non-agricultural use is already permissible under the Development Plan, Regional Plan, planning rules, and the planning authority grants development or building permission.

But this does not mean every Green Zone plot has become buildable.

If the planning rules do not allow your intended use, the NA process change will not save the deal. Verify before transaction.

3. NAINA Zoning May Restrict the Land

Many plots around Panvel, villages near the airport influence area, and Raigad-side growth pockets are sold using the word “NAINA.”

That does not mean the plot is automatically approved.

For NAINA-area land, check:

- NAINA Development Plan

- Interim Development Plan, if applicable

- NAINA DCPR

- Town Planning Scheme status

- Zone Confirmation Statement, also called ZCS

- Commencement Certificate list

- Occupancy Certificate list, if any built structure exists

A plot may be inside the NAINA influence area but still not be usable for the buyer’s intended residential or commercial purpose.

4. CRZ, Mangroves, Creek or Wetland Risk

In coastal and creek-side areas, Green Zone risk can overlap with CRZ risk.

This matters in parts of Uran, Dronagiri, Ulwe, Kharghar creek-side pockets, Nerul, Raigad coastal belts, and Thane district coastal areas.

CRZ means Coastal Regulation Zone. CZMP means Coastal Zone Management Plan.

If the land is near mangroves, creek, coast, high-tide line, wetlands or water bodies, get a proper CRZ/CZMP check. A normal 7/12 extract will not tell you everything about coastal restrictions.

5. Title, Mutation and Family Ownership Problems

Green Zone plots are often old village lands or survey-number lands.

Common title risks include:

- Incomplete family partition

- Missing legal heirs

- Pending mutation entries

- Old Power of Attorney transactions

- Tenancy or occupancy restrictions

- Class-II or restricted tenure land

- Multiple agreements on the same land

- Unregistered sale arrangements

Ferfar means mutation entry. It records changes such as sale, inheritance, partition or other ownership-related updates in revenue records.

Mutation supports verification, but it does not replace a legal title search.

6. Bank Loan and Resale Problems

Banks may avoid funding land with unclear title, non-NA status, restricted zoning, unsanctioned layout, CRZ exposure, or missing approvals.

Even if you buy the land in cash, resale can become difficult later.

The next buyer may ask the same questions you ignored:

- Is it residential?

- Is NA done?

- Is the layout sanctioned?

- Is the title clean?

- Is the plot affected by CRZ or reservation?

- Will a bank give loan?

If the answer is unclear, your exit becomes weak.

Green Zone vs R-Zone vs NA Land vs CRZ

| Term | What it usually means | Buyer risk |

|---|---|---|

| Green Zone | Development is restricted or controlled | You may not get normal construction rights |

| R-Zone | Usually residential zoning | Still check approvals, title, road and building permissions |

| Agricultural land | Land recorded for agricultural use | Buyer eligibility, conversion and permitted use must be verified |

| NA land | Land permitted for non-agricultural use | Check exact NA use, layout approval and development permission |

| CRZ land | Land affected by coastal regulation | Construction may be restricted or require special clearance |

| No-Development Zone | Area where development may be restricted | Do not proceed without written planning authority confirmation |

Documents to Check Before Buying Green Zone Property

Use this table before paying token money.

| Document | Why it matters | Where to verify |

|---|---|---|

| 7/12 extract | Shows land survey details, holder name and land classification | Mahabhumi / Digital Satbara |

| 8A extract | Shows account-level landholding details | Mahabhumi |

| Mutation entries / Ferfar | Shows ownership changes in revenue record | Revenue office / online land records |

| Property card | Important for city survey / CTS properties | Mahabhumi / land records office |

| Sale deed chain | Shows transaction history | Seller + Sub-Registrar records |

| Index II | Gives registered transaction summary | IGR Maharashtra |

| IGR eSearch | Helps check registered property transactions | IGR Maharashtra |

| Zoning certificate / ZCS | Confirms land-use zone | Planning authority / CIDCO NAINA |

| NA / development permission | Shows permitted non-agricultural or development use | Planning authority / revenue records |

| Layout approval | Checks whether plotting is sanctioned | Planning authority |

| CC / OC | Needed if structure or project exists | CIDCO / NAINA / local authority |

| CZMP / CRZ check | Checks coastal restrictions | MCZMA / CRZ consultant |

| MahaRERA record | Needed for project-style plotted or builder sale | MahaRERA |

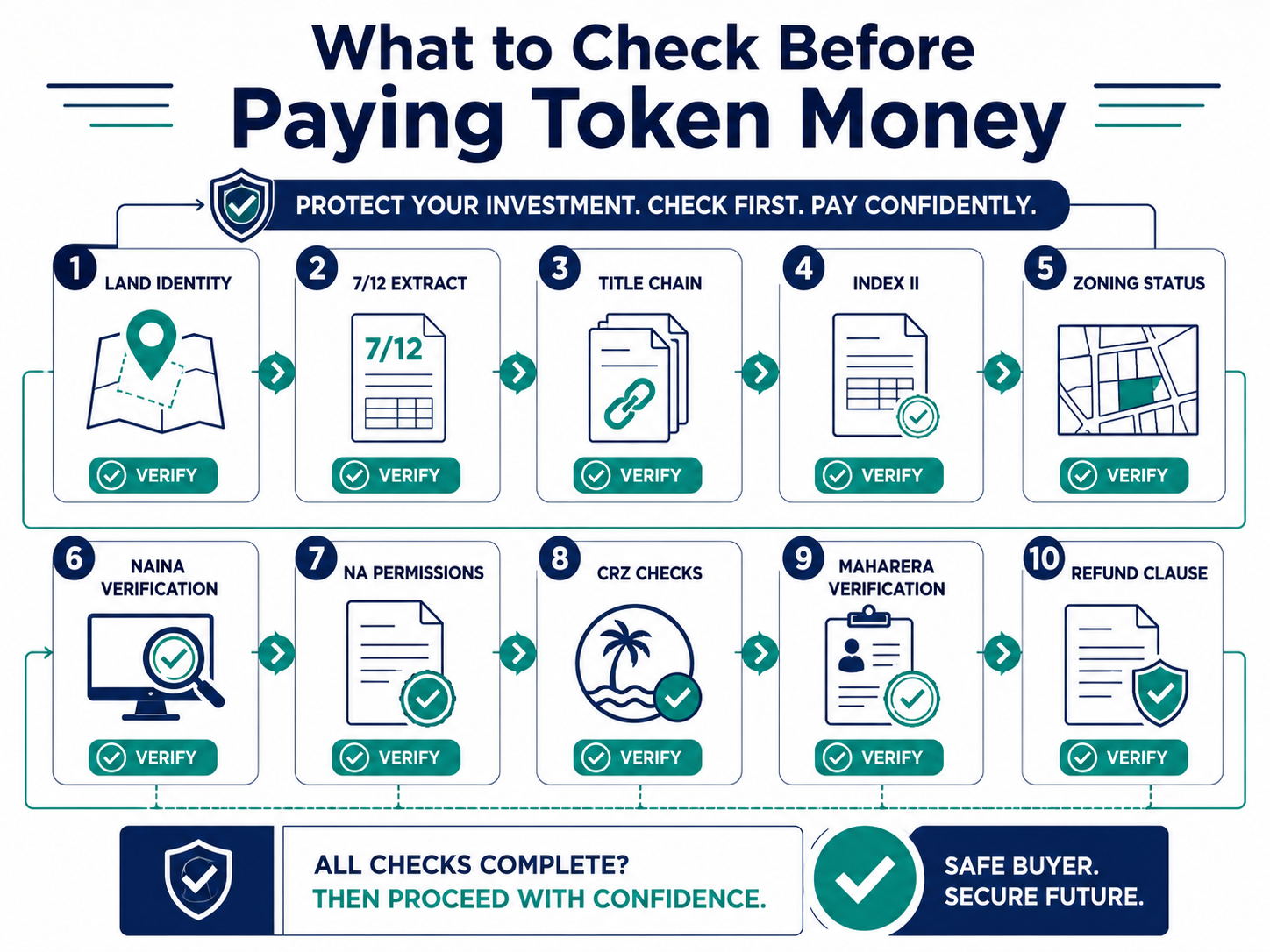

What to Check Before Paying Token Money

Before paying even a small token, ask for these details in writing:

1. Exact village name, taluka, district, survey number, gat number or CTS number. 2. Latest 7/12, 8A, mutation entries and property card, where applicable. 3. Complete title chain and Index II records. 4. Written zoning status from the relevant planning authority. 5. NAINA ZCS or CIDCO/NAINA status if the land falls in NAINA influence area. 6. NA order, development permission, layout approval, CC or OC if claimed. 7. CRZ/CZMP check if land is near creek, coast, mangroves or wetlands. 8. MahaRERA details if sold as a plotted development, farmhouse scheme, villa project or gated layout. 9. Refund clause if documents do not match seller claims.

Do not pay token money only because the seller says documents are “under process.”

How to Verify a Green Zone Property in Navi Mumbai

Step 1: Identify the Exact Land

Do not start with price.

Start with the land identity.

Ask for:

- Survey number

- Gat number

- CTS number, if applicable

- Village

- Taluka

- District

- Land area

- Road access details

- Boundary map or measurement plan

A Google Maps pin is not enough.

Step 2: Check Land Records

Check 7/12, 8A, mutation entries and property card from official land-record sources.

Plain English meaning:

- 7/12: village land record showing survey details, landholder name, area and land-use-related entries.

- 8A: account extract showing landholding details under a khata/account.

- Mutation/Ferfar: record of changes like sale, inheritance or partition.

- Property card: urban/city survey record for certain properties.

These documents help verification. They should not be treated as final proof of clean ownership.

Step 3: Check IGR Records

Use IGR eSearch and Index II to review registered transaction history.

This helps identify past sales, registered agreements, mortgages or other transactions.

Still, IGR search is only one part of due diligence. A lawyer should check title chain, court risk, inheritance, PoA, encumbrance and document validity.

Step 4: Check the Correct Planning Authority

Depending on the location, the authority may be:

- CIDCO

- NAINA

- NMMC

- Panvel Municipal Corporation

- MMRDA

- Gram Panchayat plus planning authority

- Revenue office

- MCZMA, if coastal regulation is involved

Do not accept “Gram Panchayat permission” as a substitute for planning-authority approval where higher approval is required.

Step 5: Get Written Zoning Confirmation

For Green Zone property, verbal assurance is useless.

Ask for written zoning confirmation, zoning certificate, Development Plan extract, Regional Plan extract, or NAINA ZCS where applicable.

If the seller refuses, treat it as a red flag.

Step 6: Get a Lawyer and Planner Opinion

A lawyer checks title.

A planner or architect checks buildability.

Both are needed.

Many buyers only do legal title verification and forget planning permission. That is dangerous in Green Zone, NAINA, CRZ, gaothan-side and agricultural land deals.

Navi Mumbai Example Scenario

A buyer is offered a cheap plot near Panvel in the NAINA influence area.

The broker says, “Airport development ke baad approval aa jayega. Sirf token de do.”

The buyer checks the 7/12 and sees agricultural classification. IGR search shows old family transfers. The seller gives no clear title report. The NAINA zoning check does not confirm current residential permission. The land also has unclear road access.

In this case, the buyer should not pay token money.

The correct next step is to demand written zoning confirmation, title report, NAINA/CIDCO status, road-access verification, and planner opinion.

Red Flags in Green Zone Property Deals

Stop and verify deeper if you see any of these:

- “Pay token now, documents later.”

- “Green Zone will become residential soon.”

- “NA is guaranteed.”

- “CIDCO approval coming soon.”

- “NAINA means approved.”

- “Only Gram Panchayat paper is enough.”

- “No need for lawyer.”

- “Cash payment preferred.”

- “Same layout is sold without sanctioned layout plan.”

- “RERA not needed” even though it looks like a plotted project.

- “CRZ does not matter here” for land near creek, coast or mangroves.

The biggest red flag is pressure before documents.

Common Mistakes Buyers Make

Mistake 1: Thinking 7/12 Means Safe Ownership

7/12 is important, but it is not the full title report.

It supports land-record verification. It does not confirm construction rights, clean title, bankability, CRZ safety or layout approval.

Mistake 2: Confusing Green Zone with Future Residential Land

A future-development story is not an approval.

Buy based on current written status, not future promises.

Mistake 3: Ignoring NAINA Zoning

NAINA is not one simple approval label. It has planning documents, DCPR, ZCS, town planning schemes, CC lists and OC lists.

Check the exact survey number.

Mistake 4: Ignoring CRZ/CZMP

If the land is near creek, coast, mangroves or wetlands, normal land records are not enough.

Get CRZ/CZMP verification.

Mistake 5: Paying Token Without Refund Terms

If the seller’s claims fail verification, your token should be refundable.

Put the condition in writing.

When to Consult a Professional

Consult a professional before token money if:

- The land is Green Zone, agricultural, gaothan-side, NAINA-side or CRZ-side.

- The seller depends on future conversion.

- The plot is part of an informal layout.

- Title chain has inheritance, PoA, Class-II or mutation issues.

- You are buying as an NRI.

- The deal is unusually cheap.

- The broker is pushing urgency.

The minimum team should include a property lawyer and a planner/architect. For coastal or creek-side land, add a CRZ consultant.

What If You Already Paid Token?

Do not pay more immediately.

Take these steps:

1. Ask for all documents in writing. 2. Save WhatsApp chats, receipts, payment proofs and advertisements. 3. Ask the seller to provide zoning, title, IGR, NA/development and CRZ proof. 4. Get a lawyer’s written opinion. 5. Check whether the token receipt has a refund clause. 6. If facts were misrepresented, consider legal notice or complaint options.

For the next step, read Token Amount Fraud Guide Navi Mumbai.

Final Wording

Before buying Green Zone, NAINA-side, gaothan-side or coastal land in Navi Mumbai, do not depend on verbal promises. Verify the documents first.

Next step: read never pay token money before document verification before giving any advance to the seller or broker.

FAQs

Frequently Asked Questions