Commercial Exit Risk and Vacancy Risk in Navi Mumbai

Commercial vacancy risk in Navi Mumbai is the risk that your rent stops. Exit risk is the risk that your capital gets stuck when you try to sell. The safer buy is usually not the cheapest unit or the one showing the highest brochure yield. It is the unit that has both tenant depth and buyer depth. In Navi Mumbai, mature business pockets usually reduce risk, while wrong size bands, upper-floor retail, weak access, inflated pricing, and CIDCO or MIDC transfer friction usually increase it.

That is the real point many buyers miss. They calculate yield, look at the area name, and stop there. But in Navi Mumbai, commercial property is not one market. Vashi behaves differently from a Panvel growth pocket. A ground-floor shop behaves differently from an upper-floor retail unit. A CIDCO-linked transfer behaves differently from an MIDC-linked transfer. If you ignore those differences, the deal can look profitable on paper and still become painful in real life.

The Short Answer

| Risk type | What it means | What usually causes it in Navi Mumbai | Who should care most |

|---|---|---|---|

| Vacancy risk | Long rent downtime or repeated reletting failure | weak tenant pool, wrong size band, poor frontage, upper-floor retail, high CAM/tax burden, weak access | cash-flow investors, loan-backed buyers |

| Exit risk | Slow resale, forced discount, or collapsed buyer financing | CIDCO/MIDC transfer friction, weak buyer pool, unrealistic pricing, poor building quality, thin lease comfort | investors who may need to sell in 2 to 7 years |

| Lower-risk pattern | Better rent continuity and better resale comfort | proven business nodes, practical layouts, sensible ticket sizes, clean transfer path | first-time investors, self-use buyers |

| Higher-risk pattern | Attractive on brochure, weak in actual market | speculative pricing, assured-return pitches, dead mall floors, niche units with one-tenant logic | aggressive investors only, and only after heavy due diligence |

The short verdict is simple: in Navi Mumbai, a commercial unit becomes safer when it is easy to use, easy to finance, easy to transfer, and easy to explain to the next buyer. If even one of those breaks badly, risk rises fast.

What Is the Difference Between Vacancy Risk and Exit Risk in Commercial Property?

Vacancy risk is an operating problem. Your unit sits empty, rent stops, and holding cost continues. Exit risk is a liquidity problem. You may still have a tenant, but when you want to sell, the next buyer either does not come, wants a steep discount, or cannot close because the transfer, title, or finance path is messy. That difference matters. A unit can perform well on rent for a while and still become difficult to exit.

In Navi Mumbai, vacancy risk hurts more than many buyers expect because vacant commercial property is not a harmless waiting game. NMMC-style tax math is based on rateable value, and non-residential property tax is commonly described as 68.33% of that rateable value after the usual 10% statutory deduction from expected annual rent. That means even a non-performing unit can keep draining money.

Exit risk, on the other hand, becomes brutal when authority-side charges or approvals enter the picture. CIDCO’s own services framework makes clear that transfer permission and transfer charges are part of the ownership change process, and the 2025 fee revision materially raised the cost burden in many Navi Mumbai transfers.

So think of it like this: vacancy risk decides whether income survives, exit risk decides whether capital survives.

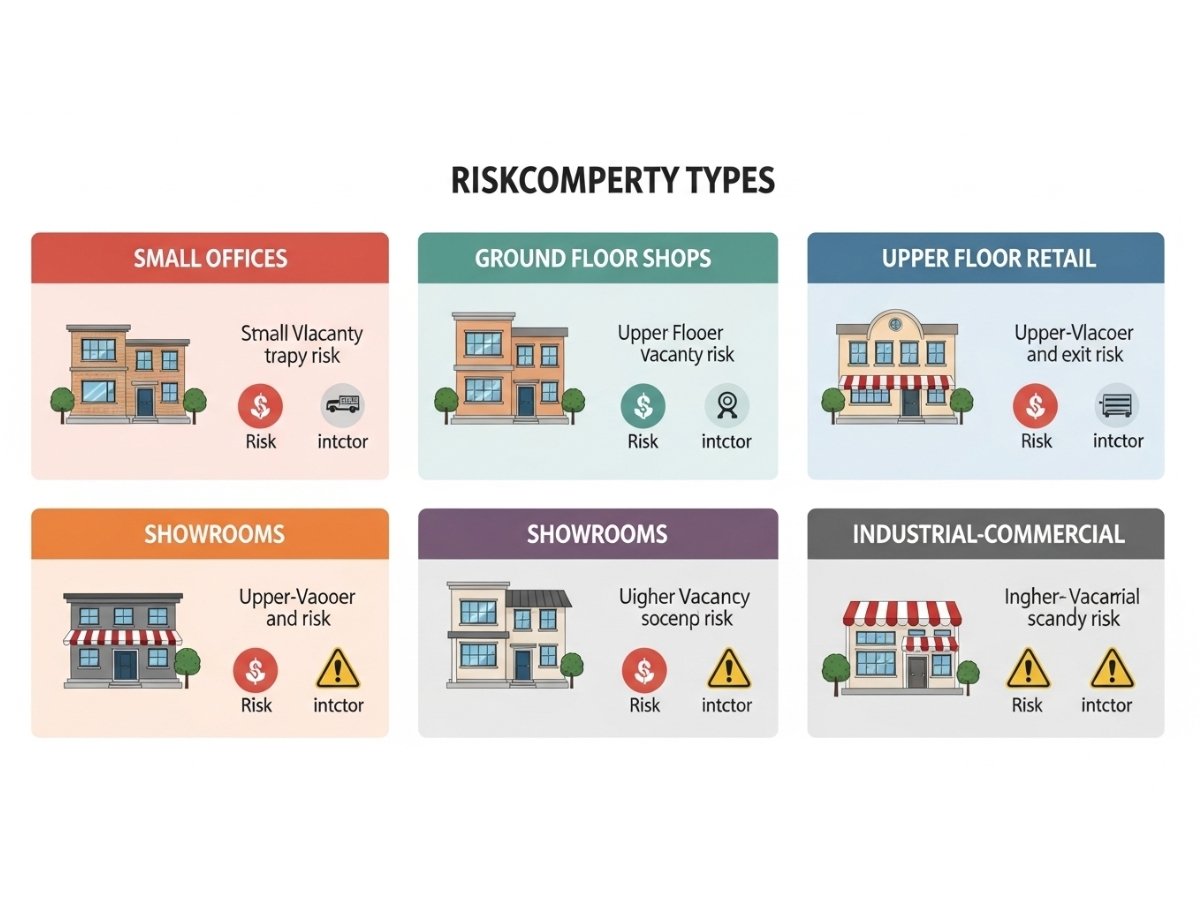

Which Commercial Formats in Navi Mumbai Usually Carry the Most Risk?

Small offices

Small offices are not automatically risky. In mature office pockets, they can work because MSMEs, consultants, back offices, brokers, logistics teams, clinics, coaching brands, and service businesses keep the tenant pool alive. But small offices become risky when the building is outdated, parking is poor, lifts are weak, signage is restricted, or the size is too odd for the actual local user base.

Ground-floor shops

Ground-floor shops usually have the deepest natural tenant pool. This is especially true when the frontage is usable, footfall is relevant, and the surrounding catchment is already active. That is why many first-time investors still prefer shops despite higher entry rates. The point is not that every shop is safe. The point is that a practical ground-floor shop is usually easier to explain to both tenants and resale buyers than a specialised upper-floor unit.

Upper-floor retail

This is where many buyers get trapped. Upper-floor retail often looks affordable compared with ground-floor stock, but the lower entry price is not a free gift. It is usually compensation for weaker walk-in logic, higher lift dependence, poor visibility, and narrow tenant depth. In weak projects, upper-floor retail can sit empty for long periods and then become hard to sell because the next buyer can see the same problem you ignored.

Showrooms

Showrooms can work well, but only in the right roads and catchments. They are not ordinary retail. They need visibility, frontage, parking or at least decent stopping logic, and category fit. A premium showroom unit on the wrong road is not a premium commercial asset. It is just an expensive mismatch.

Gala or industrial-commercial stock

Industrial-commercial stock, especially in MIDC-linked belts, can have strong occupier relevance. But the exit can get complicated. Transfer rules, development status, FSI consumption, and differential premium can materially change what looks like a simple sale. CAG’s audit material and transfer-guideline summaries both show why 10% and 30% differential premium outcomes matter in MIDC-linked transfers.

Pre-leased units

Pre-leased does not mean low-risk by default. A real lease with a durable tenant, proper deposit, realistic rent, and clear title can reduce vacancy risk. A fake “guaranteed return” story can do the opposite and hide future vacancy risk behind present marketing.

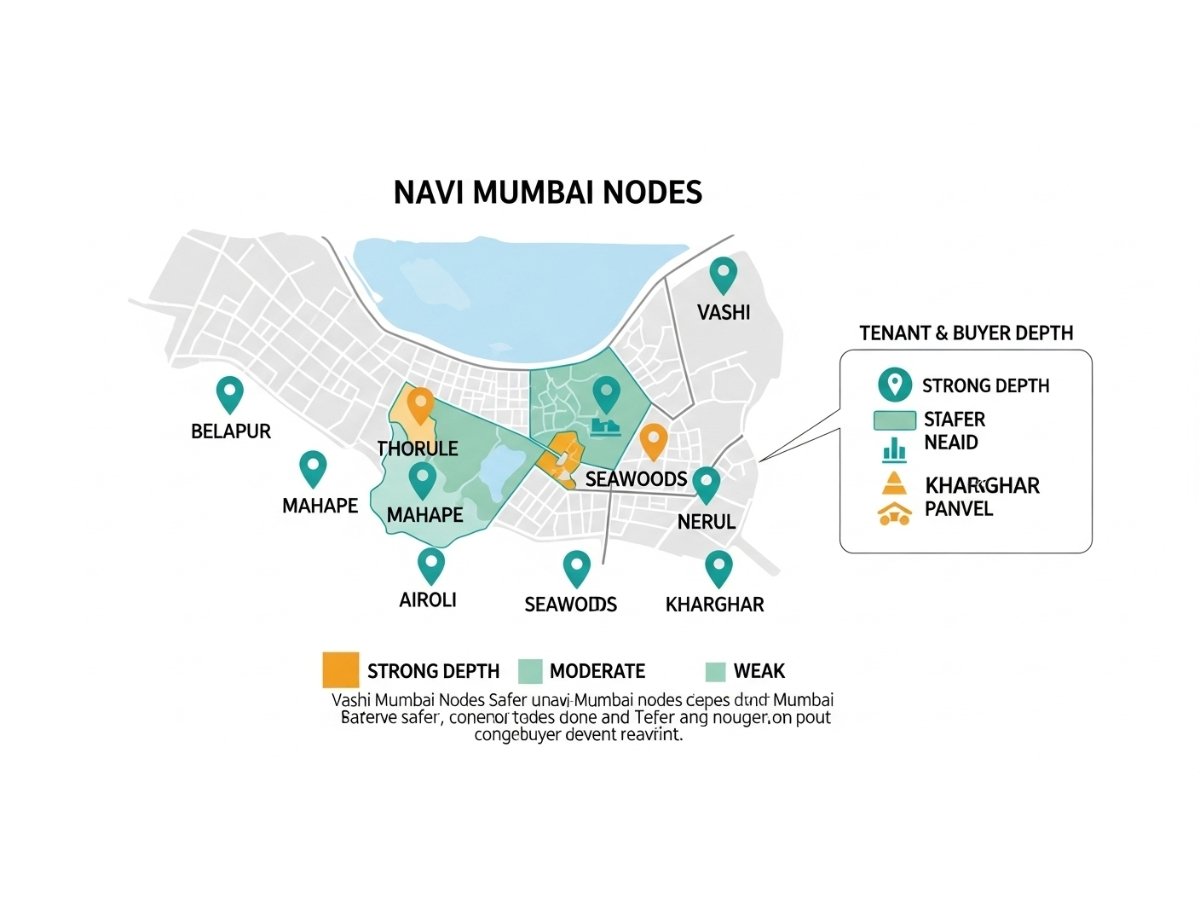

Which Navi Mumbai Nodes Usually Have Better Tenant Depth and Buyer Depth?

Node logic is not cosmetic. It changes both rentability and exitability.

Vashi and CBD Belapur for mature office and business movement

Vashi and CBD Belapur still benefit from market familiarity, established business movement, and easier explainability to local buyers. In Cushman & Wakefield’s Q4 2025 Grade A office data, Vashi showed 5.7% vacancy, which is materially tighter than many broader suburban office pockets. That does not make every Vashi unit good. But it does support the practical point that mature business districts usually offer better tenant depth and more predictable resale conversations.

Airoli, Mahape, Rabale and the wider Thane-Belapur belt for occupier-driven demand

This side of the market works differently. It is more occupier-driven, especially for office and industrial-commercial use. The same Cushman & Wakefield report shows Thane-Belapur Road at 11.5% vacancy in Q4 2025 and explicitly includes Airoli, Ghansoli, Mahape, Juinagar and Seawoods in that cluster. So the depth is real, but it is not the same as a Vashi high-street or Belapur standalone office conversation. The buyer pool can be more format-specific and more ticket-size-sensitive.

Nerul and Seawoods for selective premium commercial logic

Nerul and Seawoods can work, but this is not blind mass-market commercial demand. These pockets are selective. Good units can attract serious interest, especially where station access, road visibility, catchment quality, and overall building image support the use case. Weak internal units, awkward upper floors, or overpriced “premium” stock can still struggle.

Kharghar, Panvel and growth-led belts for selective current demand and future-led pricing

These locations attract buyers because the long-term city story is strong. But infrastructure-led pricing and actual present tenant depth are not the same thing. In growth-led corridors, vacancy risk is often higher in the short to medium term because the commercial ecosystem is still catching up. So if you buy here, you should do it knowing you may need more patience and stronger holding capacity.

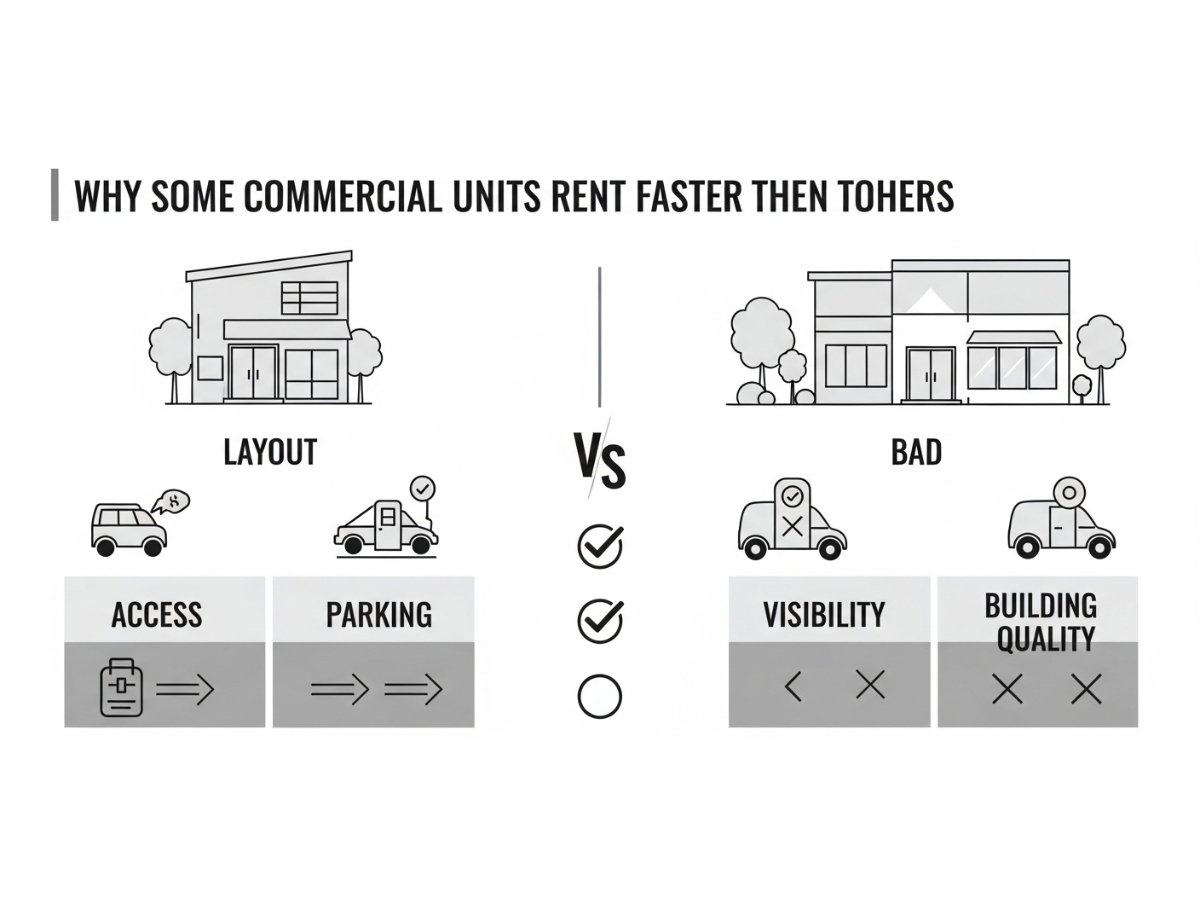

Why One Unit in the Same Node Gets Relet Quickly While Another Stays Vacant

Because the market does not rent “sector names.” It rents usability.

One office in the same belt gets relet in weeks because it has a sensible carpet area, decent lobby, stable lift access, workable parking, and a rent that matches the real user pool. Another stays empty because the layout is awkward, the floor plate is too small or too large for the local market, the building feels tired, CAM is heavy, or the customer journey is irritating.

Retail is even more unforgiving. A shop with clean frontage, direct line of sight, and natural stopping movement behaves very differently from a unit hidden behind a staircase, inside a low-conversion arcade, or on an upper floor with no anchor draw.

This is why “footfall” alone is a weak buying metric. What matters is usable footfall, conversion-friendly access, and the right tenant fit for that exact micro-location.

Why Some Commercial Units Become Hard to Sell Even If They Are Already Leased

A leased unit can still be a bad exit.

The first reason is the overpriced rent story. Some sellers want you to capitalise one unusually high rent and ignore whether that rent is sustainable after renewal. If the current rent is above market, or the tenant covenant is weak, the next buyer will discount the asset even if today’s brochure yield looks attractive.

The second reason is building quality and finance comfort. If the building is aging badly, services are weak, title documentation is thin, or the transfer path is messy, resale buyers become cautious. Banks become cautious too. At that point, the tenant alone cannot save your exit.

The third reason, and in Navi Mumbai this is a serious one, is authority friction. Indian Express reported that after the 2025 CIDCO revision, commercial properties above 200 sq m could attract transfer charges as high as ₹5,84,600 per sq m, with commercial land transfer rates starting from ₹1,93,400 per sq m, and CIDCO-related fee revisions also included a 50% hike for commercial shops and flats in registered societies. Even where the exact payable amount depends on size, location, and property type, the larger lesson is obvious: transfer cost can become so heavy that it changes the deal economics itself.

That is why exit risk in Navi Mumbai is not only “will someone buy this?” It is also “can the transaction still make sense after all transfer-side friction is priced in?”

Are Pre-Leased Commercial Properties in Navi Mumbai Really Safer?

Sometimes yes. Sometimes absolutely not.

A genuine pre-leased asset can reduce vacancy risk when the tenant is strong, the lease is registered, the deposit is meaningful, the escalation is reasonable, and the entry price is not inflated. In that case, you are buying an income stream that has at least some real market logic behind it.

But many buyers confuse “tenant on paper” with “safety in reality.” If the lease has a short balance term, weak lock-in, or a tenant whose business itself looks shaky, the future vacancy risk is only being postponed.

> Red flag: Be very careful with “assured return” or “guaranteed rent” pitches where the real tenant story is weak or absent. SEBI’s investor caution notes treat assured returns, overly consistent returns, and high-return-with-low-risk claims as classic warning signs in Ponzi-style behaviour, and the Banning of Unregulated Deposit Schemes law separately prohibits unregulated deposit schemes and related inducement. In plain language, if the return promise is doing all the work and the actual business use of the asset is unclear, do not treat that as safe income.

In commercial property, lease quality matters more than the “pre-leased” label.

How to Judge Vacancy Risk Before You Buy

Start with the building, not the brochure. How many units are actually occupied? How many are occupied by serious operating businesses and not just name boards? What is the reletting history of similar units in that exact building or immediate strip?

Then test tenant fit. Ask who can realistically take this unit in the next three years. Not theoretically. Realistically. If the answer depends on only one category, risk is already high.

Next, test total occupancy cost, not base rent alone. In NMMC-governed areas, non-residential property tax can materially increase carrying burden, and CAM, power load, parking cost, signage restrictions, and fit-out needs can together make a unit unattractive even when the headline rent looks fair.

For under-construction or recently delivered stock, check MahaRERA before you commit. MahaRERA’s public framework allows buyers to review registered-project disclosures such as sanctioned plans, project timelines, quarterly updates, approvals taken and pending, lapsed or revoked project status, and complaint access. That is not a box-ticking exercise. It is often the difference between a rental plan that starts on time and one that keeps getting pushed.

How to Judge Exit Risk Before You Buy

Exit planning should start before the token, not after possession.

First, ask who the next buyer will be. A local investor? A self-use business owner? A larger institutional buyer? If the likely buyer pool is too narrow, exit risk rises even if the property itself is decent.

Second, test finance comfort. Would a bank be comfortable lending to the next buyer on this exact asset? Clean documentation, clear transfer path, sensible valuation, and normal building condition all matter here.

Third, identify the governing authority and transfer mechanics. CIDCO-linked property transfers require permission and transfer charges as part of the process. MIDC-linked industrial-commercial transactions may involve differential premium, and the burden can vary sharply depending on development status and policy interpretation. Do not treat those as small clerical expenses. In some deals, they are value-changing numbers.

Finally, compare achieved market reality, not just asking prices. If a seller is quoting a premium because of one lease, one future corridor story, or one inflated promised rent, be careful. Exit comfort comes from broad buyer acceptance, not from one optimistic narrative.

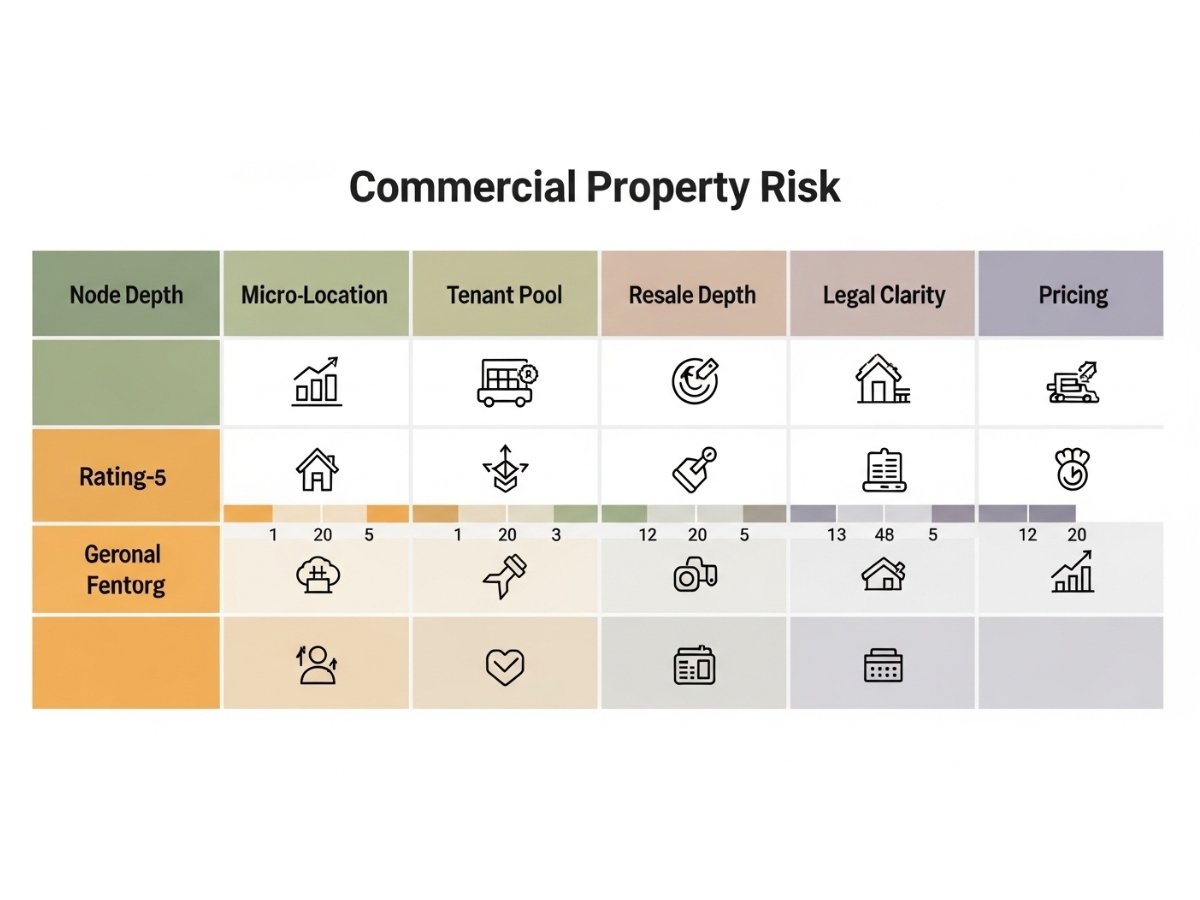

A Practical Risk Scorecard for Commercial Buyers in Navi Mumbai

Use this simple scoring model before you buy. Score each head from 1 to 5, where 1 = high risk and 5 = lower risk.

| Risk head | 1 | 3 | 5 |

|---|---|---|---|

| Node depth | speculative micro-market | mixed demand pocket | mature business pocket |

| Micro-location quality | hidden / awkward / poor access | workable but not ideal | strong frontage / clean access |

| Tenant depth | one narrow tenant type | moderate options | wide real tenant pool |

| Resale buyer depth | very limited | selective | broad local buyer base |

| Operating burden | high CAM / tax / fit-out pain | manageable | efficient holding cost |

| Legal / transfer clarity | unclear transfer path | partly clear | clean and explainable |

| Pricing discipline | story-driven pricing | near market | sensible entry relative to reality |

A unit scoring mostly 4s and 5s may still not be a bargain, but it is usually more survivable. A unit scoring multiple 1s and 2s can look cheap and still become a capital trap.

Who Should Accept Higher Risk and Who Should Avoid It Completely?

A first-time commercial investor usually should not chase complicated stories. Safer choices are normally practical units in proven pockets, even if the entry price feels less exciting.

A cash-flow-focused investor should care most about vacancy risk. For that person, tenant depth matters more than glamour.

A capital-gain-focused investor can accept more location-cycle risk, but only if holding power is strong and the legal-transfer path is clean. Buying in a growth-led corridor without the patience or liquidity to absorb downtime is not strategy. It is stress.

A self-use buyer gets some natural protection because the unit is being used. Even then, future resale still matters. If the asset is hard to explain to the next buyer, self-use alone does not remove exit risk.

When Should You Walk Away From the Deal?

Walk away when the unit is cheap for a reason that will not change.

Walk away when the seller cannot clearly explain transfer procedure, authority dues, leasehold position, or whether any permission is required. Walk away when the building has weak real occupancy and the broker keeps changing the tenant story. Walk away when an upper-floor retail unit is being sold like a high-street shop. Walk away when guaranteed rent is the main pitch. Walk away when the numbers only work if every optimistic assumption comes true.

And walk away when the legal path is foggy. In Navi Mumbai commercial property, unclear transfer mechanics are not a minor issue. They are often the real risk.

Conclusion

Commercial exit risk and vacancy risk in Navi Mumbai should never be judged only by node name, brochure yield, or future infrastructure story. The right question is much more practical: Can this unit attract a real tenant, and can it later attract a real buyer without the transaction collapsing under pricing, paperwork, or transfer charges?

If the answer is clear on both fronts, the property may be worth serious consideration. If the answer is weak on either front, the deal is already riskier than it looks. In Navi Mumbai commercial property, the best buy is rarely the loudest one. It is usually the unit that still makes sense after the marketing is removed.

FAQs

Frequently Asked Questions