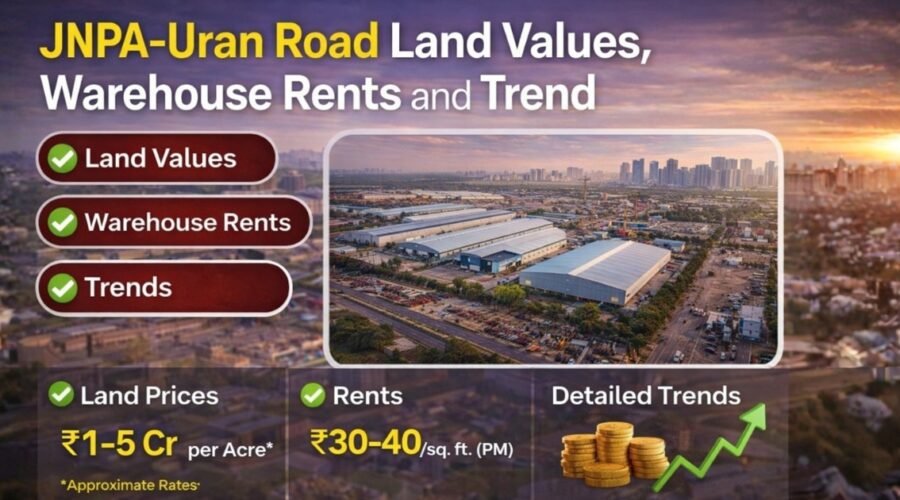

JNPA-Uran Road Land Prices: Warehouse Rents and Trend

JNPA-Uran Road land prices and warehouse rents are rising, but not as one uniform market. That is the first thing to understand. Port-facing logistics stock, Dronagiri-side pockets, Jasai-Pagote connector zones, and deeper Uran-side speculative land all behave differently. The right move in 2026 depends less on one “rate” and more on road access, zoning, title clarity, building quality, and whether the price is backed by real logistics demand or only a future story.

Most weak pages miss this completely. They treat the whole corridor as if port, airport and highway growth will lift every parcel equally. That is not how this belt works on the ground.

The JNPA-Uran Road corridor is important because three large forces are active at the same time. JNPA has just recorded its highest-ever annual container throughput at 8.17 million TEUs and 102.01 million tonnes of cargo in FY 2025-26. Navi Mumbai International Airport has already started commercial operations. And the six-lane Pagote-Chowk greenfield highway has official approval to improve movement between JNPA, NMIA and the national highway network. Those are real demand drivers. But they do not make every land parcel equally useful for warehousing.

JNPA-Uran Road land values and warehouse rents are rising, but not as one uniform market

The short answer is simple: yes, the corridor is gaining value, but the appreciation is fragmented and uneven.

A good warehouse market and a rising land market are not always the same thing. In some pockets, especially near functional freight routes, values are being supported by real occupier demand. In other pockets, land prices are running ahead because of airport headlines, Third Mumbai expectations, and future highway optimism. That difference matters a lot if you are buying for rent, not just for speculation.

Quick summary

| Market question | Practical answer in 2026 |

|---|---|

| Are values rising? | Yes, but not evenly |

| Are warehouse rents rising too? | Yes for better stock, not automatically for all sheds or plots |

| Is there one JNPA-Uran Road rate? | No |

| Best pocket for present logistics logic | JNPA-facing and Jasai-Pagote linked stock |

| Most caution needed | Internal Uran-side speculative land |

| Biggest mistake | Buying story instead of operational utility |

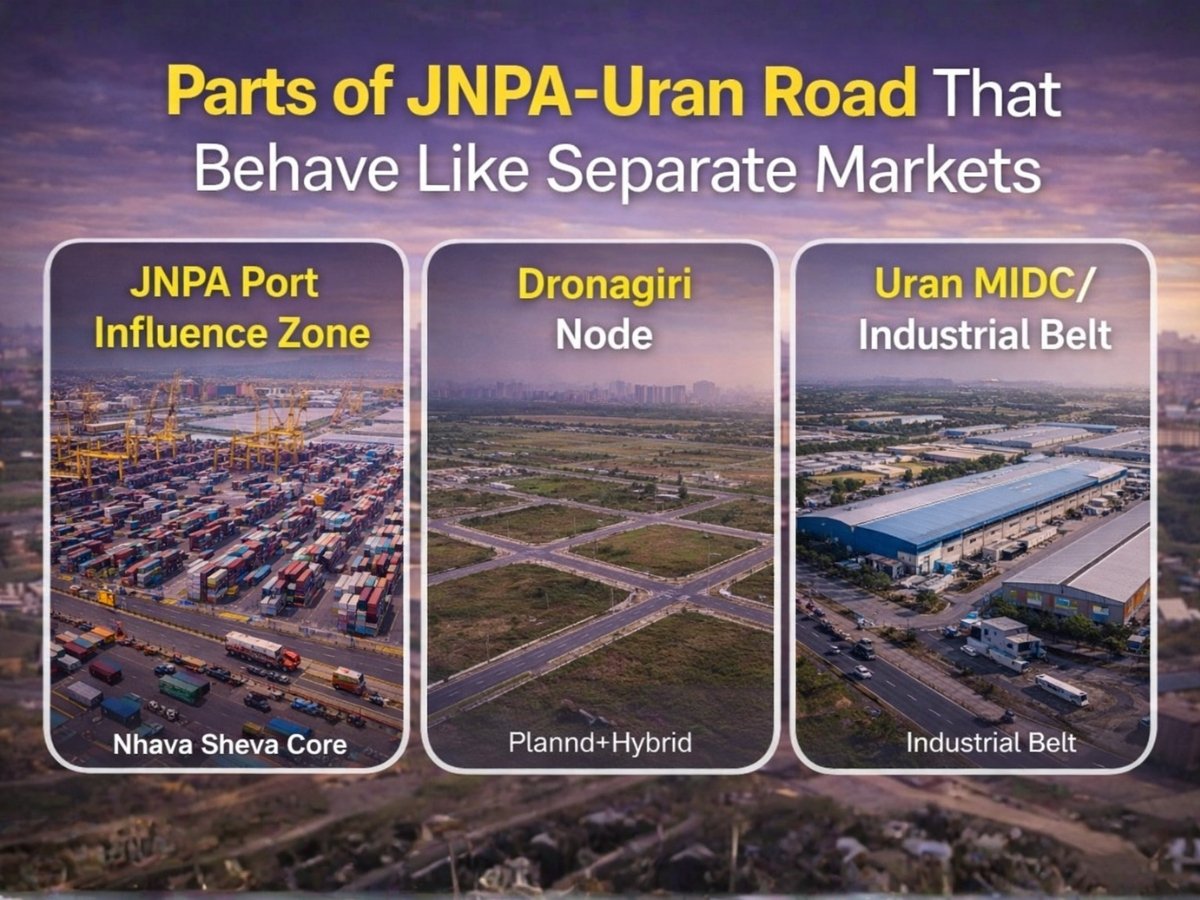

Which parts of the JNPA-Uran Road belt actually behave like separate markets?

This corridor should be read as at least four different sub-markets.

JNPA Road and port-facing logistics stock

This is the most operations-led part of the belt. Here, value is not mainly coming from hype. It is coming from time saved, truck trips reduced, customs-linked movement, and faster cargo turnaround. If an occupier needs direct port advantage, this zone remains the strongest.

This is also where premium warehouse stock can command the highest asking rents because the location solves an actual logistics problem. Current portal snapshots show large JNPT Township warehouse listings around ₹30 per sq ft per month, while some very large Uran-side/JNPA-linked listings are being marketed at ₹35 per sq ft per month. These are asking figures, not guaranteed achieved rents, but they show the premium that functional, larger-format stock can try to command near active logistics routes.

Dronagiri-side warehouse and land pockets

Dronagiri still has relevance because it sits within the broader port influence zone and has a planned-node framework. But it is no longer a clean warehousing-only story. Residential growth and mixed-use pressure have changed its character in parts. That matters because heavy vehicle movement, 24/7 operations, and large truck staging do not work equally well everywhere once local urban friction starts rising.

This is why Dronagiri often looks stronger on map logic than on actual warehouse economics. Land can appear expensive, but rental yields do not always keep up. For some occupiers it still works, especially smaller storage or lighter commercial activity, but it is not automatically the best answer for every logistics user.

Jasai, Pagote and connector-side opportunity zones

This is the part of the corridor where the story is strongest and the logic is improving in a practical way. Jasai and Pagote sit in the zone that can benefit from port access, airport relevance and better highway evacuation at the same time.

The Pagote-Chowk highway is a major reason this pocket is being watched closely. The project is 29.219 km long, six-lane, access-controlled, and was approved by the Cabinet to improve direct freight movement from JNPA toward Chowk and the broader regional road network. For logistics property, this matters because better evacuation can turn a merely “nearby” location into a genuinely efficient warehouse location.

Portal snapshots also show the market beginning to reflect this. A Jasai warehouse listing of 16,000 sq ft is being marketed around ₹20 per sq ft per month, which sits meaningfully below top JNPA-facing premium stock but still shows that better-quality connector-side warehousing is not being priced like generic village-side storage anymore. Again, this is asking rent, not market truth for every shed.

Internal Uran-side land where the future story can outrun present usability

This is where buyers need the most discipline.

The deeper Uran-side and KSC New Town influence areas are attracting attention because MMRDA’s K.S.C. New Town covers 323.44 sq km, and the state has approved the land acquisition and allocation policy for this new town area. That has naturally pushed speculative interest into internal villages and raw land belts.

But speculative attention and warehouse readiness are not the same thing. A plot may rise in price because people expect future urbanisation. That still does not mean it is ready for truck-heavy warehousing today. Internal access, road width, right of way, zoning, approvals, and logistics suitability can all remain weak even while asking prices jump.

What is pushing land values and warehouse rents up in this corridor right now?

Three real forces are supporting the corridor in 2026.

JNPA cargo growth and logistics volume

JNPA remains the foundation of this market. In FY 2025-26, it handled 8.17 million TEUs, up from 7.30 million TEUs in FY 2024-25, along with 102.01 million tonnes of overall cargo. That is not a small background detail. It is the core reason port-linked warehousing demand remains real. If cargo throughput keeps setting records, nearby facilities that help in fast movement, consolidation, cross-docking or storage stay relevant.

NMIA operations and air-cargo ecosystem spillover

NMIA started commercial operations on 25 December 2025. That alone changes regional geography, but the bigger point for this corridor is cargo. FedEx has already announced a 300,000 sq ft fully automated air cargo hub at NMIA with investment exceeding ₹2,500 crore. That tells you the airport story is not only about passenger traffic. It is about a future cargo and distribution ecosystem too.

This does not mean every plot near Uran becomes a premium air-cargo site. It means that the broader Panvel-Uran logistics belt now has a stronger multimodal case than before.

The Pagote-Chowk highway and why road connectivity changes pricing logic

Road logic changes warehouse logic. That is the simplest way to put it.

If trucks continue to lose time in choke points, even a good warehouse location can feel weaker in practice. If a new high-speed corridor reduces that friction, nearby land starts becoming more attractive for actual logistics deployment. The Pagote-Chowk highway is important because it improves the corridor between JNPA, NMIA and major onward routes. That is why Jasai-Pagote side pockets are getting more attention than random interior plots with no comparable movement advantage.

Are land values running ahead of real warehouse demand in some pockets?

Yes, in some pockets they clearly are.

This is the biggest caution in the entire corridor. Once a location gets attached to “airport influence”, “Third Mumbai”, or “future growth belt”, land prices can rise faster than rental logic. When that happens, warehouse yield gets squeezed. A buyer may pay a high raw-land price today, then realise that no occupier is willing to pay the rent needed to justify that land cost plus construction cost.

That risk is highest where:

- the plot is still dependent on future zoning clarity

- access roads are weak

- the location is not yet a proven truck movement belt

- nearby development is more narrative than functioning logistics

MMRDA’s KSC New Town framework is real and important. But from a warehousing point of view, buyers still need to separate urban development potential from immediate logistics usability. Those are two different investment theses.

> Caution > > If a land deal only sounds attractive because of airport, MTHL or Third Mumbai headlines, but you cannot clearly explain truck access, zoning, warehouse fit and likely tenant type, you are probably looking at a speculative land story, not a warehouse cash-flow story.

How should readers read warehouse rents here without getting misled by random listings?

The first rule is simple: never read warehouse rent as a single corridor-wide number.

A few online listings can make the market look hotter or cleaner than it really is. One large compliant warehouse near a better route can quote ₹30 to ₹35 per sq ft, while weaker stock deeper inside can struggle despite lower asking numbers. The headline rent never tells the full story by itself.

The second rule is that rent per sq ft matters only after building quality and movement quality are checked.

Warehouse rent reality checklist

Before trusting any rent quote, check these:

- Clear height: low clear height reduces true storage efficiency

- Floor strength: weak flooring limits racking and heavy movement

- Docking setup: dock levelers and truck handling matter

- Approach road width: a good shed on a bad road is still a weak asset

- Turning radius and truck court: critical for larger trailers

- Fire compliance and NOCs: serious tenants will screen this

- Power and utility reliability: very important for organised users

- Exact pocket: JNPA-facing, Jasai-linked, Dronagiri-side and internal Uran stock cannot be read as one rent bucket

If these are poor, the real achieved rent can fall well below the asking figure.

Which asset makes more sense here: raw land, ready warehouse, old godown, or built-to-suit potential?

Different asset types suit different buyers.

| Asset type | Best use case | Main upside | Main risk |

|---|---|---|---|

| Raw industrial land | Long-term developer or land banker | Highest future upside if zoning and execution align | No immediate cash flow, approvals and execution risk |

| Ready Grade A warehouse | Yield-seeking investor or occupier needing immediate use | Faster leaseability, better tenant quality | High entry cost |

| Old godown / older stock | Local operator with specific low-cost use | Lower acquisition cost | Obsolescence, weaker tenant pool, capex burden |

| Built-to-suit potential | Strong occupier-backed development | Custom fit, sticky tenant | Timeline and dependency on occupier |

For most normal investors, this is where mistakes happen. They assume raw land is always the smartest play because appreciation looks bigger. But in a technical logistics market, execution quality decides value. A mediocre plot bought on a hot story is often weaker than a truly usable ready warehouse bought at a fair yield.

When does buying in the JNPA-Uran Road corridor make sense, and when is leasing smarter?

Buying makes sense when the asset solves a long-term operational problem or when you are entering a logistics pocket before its connectivity improvement is fully priced in.

That means buying can be sensible for:

- port-linked end users

- logistics players who know their cargo pattern well

- developers who can build compliant stock in Jasai-Pagote side pockets

- investors buying proven Grade A warehousing, not random speculative land

Leasing is usually smarter when flexibility matters more than control. That is the case for many 3PLs, distributors, and growing businesses. In 2026, leasing often remains more practical than buying raw land and then spending time, money and approvals on creating a compliant facility from scratch.

Waiting is the smartest choice when:

- the land is agricultural or unclear in use

- zoning clarity is still weak

- right of way is doubtful

- the price assumes future infrastructure is already fully monetised

- the deal depends more on narration than on present warehouse mathematics

What title, approval and land-use risks should buyers check before trusting the growth story?

This corridor is not a place for casual due diligence.

CIDCO-linked land structures, leasehold history, transfer process, access-right issues and land-use mismatch can all seriously affect a deal. In Navi Mumbai-side planned areas, legal clarity is not a side issue. It is part of valuation.

What to verify before paying token

- Exact land use and whether warehousing is actually permitted

- Whether the plot is freehold, leasehold, CIDCO-linked or under another layered structure

- Chain of title, mutation, and supporting records

- Access road legality, not just physical existence

- Truck usability of the approach road

- Fire, environmental and operating compliance needs

- Whether the asset is suited for light storage, heavy storage, container-linked use, or only local distribution

This matters even more in 12.5% scheme or village-linked transactions where the paper trail may be more complex than buyers first assume.

> Caution > > A road-touch plot is not automatically a warehouse plot. A rising-location plot is not automatically a legally clean plot. And a cheap old shed is not automatically a bargain.

What kind of occupier or investor fits this corridor best?

The corridor is not for everyone.

Port-linked cargo users fit best in the JNPA-facing side where turnaround and drayage matter most. Highway distribution and modern 3PL-style warehousing fit better in improving connector-side zones such as Jasai-Pagote, especially as road logic strengthens. Smaller mixed-use or lighter storage users may still find some Dronagiri-side options workable, but that is a narrower use case than many advertisements suggest.

The weakest fit is the investor who has no logistics understanding and is buying only because the macro story sounds exciting. This market rewards clarity, not excitement.

How does JNPA-Uran Road compare with Kalamboli, Panvel-side belts and Dronagiri alternatives?

JNPA-Uran Road is strongest when port plus airport plus future highway logic all matter together. That is its special advantage.

Kalamboli is still powerful for road-led freight and established warehousing logic, especially for domestic movement and heavy trucking ecosystems. Panvel-side belts are useful where expressway-oriented domestic distribution matters more than direct port adjacency. Dronagiri remains relevant but is less clean as a pure large-format logistics answer than many people assume because of mixed urban pressure.

So the choice depends on what you are actually moving:

- EXIM and port urgency: JNPA-facing side

- Modern multimodal logistics and future-ready distribution: Jasai-Pagote side

- Road-led regional distribution: Kalamboli / Panvel-side belts

- Smaller, mixed-use, lighter operational requirement: selected Dronagiri stock

What market signals should you track over the next 12 to 24 months before paying a premium here?

If you are serious about buying, watch signals, not just stories.

First, track JNPA throughput. If container and cargo numbers stay strong, port-linked warehouse demand remains grounded. Second, track NMIA cargo ecosystem build-out, not just passenger headlines. Third, track the actual execution progress of the Pagote-Chowk highway, because physical progress matters more than announcement value once land starts repricing.

Also watch what happens to:

- leasing velocity of better Grade A stock

- vacancy in older godowns

- spread between premium asking rents and weaker negotiated rents

- zoning clarity in KSC New Town influence areas

If premium stock continues to lease while weak stock struggles, the market is telling you something very clearly: quality and location discipline matter more than corridor hype.

FAQs

Is the JNPA-Uran Road corridor good for warehouse investment?

Yes, but only in the right pocket and the right asset type. Better-quality, legally cleaner, access-friendly warehousing near functional freight routes is a different proposition from speculative internal land.

Are land prices near JNPA already too high?

In some pockets, yes. Especially where the price is being driven more by airport or future-city narrative than by present warehouse yield logic.

Which is better for warehousing: Dronagiri or JNPA Road?

For heavier, more port-dependent warehousing, JNPA-facing stock is usually stronger. Dronagiri can still work, but it is more mixed and not as uniformly logistics-efficient.

Does NMIA really affect warehouse demand here?

Yes, selectively. NMIA matters more for specialised cargo, distribution and multimodal logistics logic than for every ordinary land parcel in the wider Uran belt.

Should small investors buy raw land here?

Only with caution. If you do not have the holding power, legal diligence capability, and development understanding, raw speculative land can become a trap faster than it looks.

Final verdict

JNPA-Uran Road is one of the most important logistics-linked real estate corridors in the Navi Mumbai region today, but it is not a simple “buy anywhere” story. The strongest opportunities in 2026 are where present logistics utility and future connectivity are meeting together. That usually means better JNPA-facing operational stock and carefully chosen Jasai-Pagote side opportunities, not every interior Uran parcel carrying a growth tagline.

So who should buy now? Serious end users, informed developers, and investors buying proven logistics utility. Who should lease? Most occupiers who want flexibility and faster operational readiness. Who should wait? Anyone looking at unclear title, unclear zoning, weak access, or purely speculative land dressed up as a warehouse play.

That is the real corridor logic.

FAQs

Frequently Asked Questions