Navi Mumbai Commercial Rental Yield by Node

Navi Mumbai Commercial Rental Yield by Node does not come from one city-wide number. It changes sharply by node, asset type, entry price, tenant depth, and local cost burden. In simple terms, Vashi and CBD Belapur usually offer safer and easier rent continuity, while Panvel, Kalamboli, and some growth-led pockets can show stronger headline yield on paper but carry more vacancy and execution risk. That is the real answer most investors need first.

Major commercial demand in Navi Mumbai is being helped by lower office rentals than the average of major Tier-1 cities, which is one reason the market is getting serious occupier attention. But that does not mean every node behaves the same. A station-linked office in Belapur, a shop in Vashi Sector 17, a Grade A office in Airoli, and a premium unit in Seawoods Grand Central are all part of different rental markets even if they sit in the same city.

Quick Summary: Which Node Fits What Kind of Commercial Yield Strategy?

| Node Cluster | Better For | Indicative Gross Yield Position* | Income Stability | Vacancy Risk | Best Suited Buyer |

|---|---|---|---|---|---|

| Vashi & Sanpada | Shops, compact offices, stable utility retail | Moderate to high | Very high | Low | Income-first buyers who want easier reletting |

| CBD Belapur | B2B offices, admin-led demand, service firms | Moderate | High | Low to medium | Safety-first investors wanting predictable office demand |

| Airoli & Mahape | IT/ITES offices, larger floor plates, corporate leasing | Moderate to high, but volatile by tenant type | Medium to high | Medium | Buyers comfortable with corporate lease cycles |

| Nerul & Seawoods | Premium showrooms, boutique offices, brand-led spaces | Moderate | High | Low to medium | Capital-safety and premium-positioning buyers |

| Kharghar | Mixed-use commercial, education-led demand, emerging business activity | Moderate to moderately high | Medium | Medium | Buyers blending current rent with future upside |

| Panvel & Kalamboli | Budget retail, logistics-linked spaces, lower entry ticket | High headline yield possible | Low to medium | High | Higher-risk growth buyers |

\*Indicative yield position is based on current market patterns, published asking data, and the local cost structure. Final negotiated rent, fit-out burden, frontage, floor, building age, and tax treatment can change the actual result materially. :

Which Navi Mumbai nodes usually give stronger commercial rental yield, and which feel safer?

The practical answer is this: safer yield and higher yield are not the same thing.

Vashi and CBD Belapur usually feel safer because tenant depth is real, reletting is easier, and businesses already understand those locations. Panvel, Kalamboli, and some other lower-entry pockets can show better headline percentages because the purchase denominator is lower, but that does not automatically mean the income quality is better. A property that looks like a 7.5% or 8% deal on paper can quickly become a weak performer if the unit stays vacant for months or needs repeated tenant resets.

This is where many pages go wrong. They treat commercial yield like a static formula. In reality, commercial rental yield in Navi Mumbai is a product of five moving parts: entry price, tenant depth, micro-location, building usability, and cost leakage. Once vacancy, CAM, property tax, brokerage, fit-out concessions, and authority friction are added, the order of “best” locations often changes.

Vashi and CBD Belapur: does mature demand improve safety even when percentage yield compresses?

Yes, that is usually the trade-off.

Vashi for shops, small offices, and reletting depth

Vashi remains one of the easiest commercial nodes in Navi Mumbai to understand. It has long-established business familiarity, station convenience, dense daily activity, and a mix of retail plus office demand. Current asking listings still show a wide office-rent spread, from smaller ticket spaces to larger furnished units, which is exactly what a mature market looks like: many unit sizes, many use cases, and multiple tenant types.

For investors, the real strength of Vashi is not only the rent figure. It is the depth of replacement demand. Small offices, shops, clinics, consultancies, agencies, and utility retail can all function here. That usually improves continuity of income, even when capital values are high enough to compress percentage yield.

CBD Belapur for office-led demand and selective retail

CBD Belapur works differently. It is more office-led, more administrative, and more B2B in nature. Current live listings still show everything from small station-adjacent office units to large fitted spaces in known commercial towers, which supports the view that Belapur is a strong office node rather than a pure high-street retail play.

So, does mature demand improve safety? Usually yes. The buyer pays for it through a higher acquisition cost and, therefore, a somewhat compressed yield percentage. But the trade can still be worthwhile because safer rent continuity often beats a flashy headline yield in a weaker node.

> Practical read: > Vashi usually suits income-first buyers who want faster reletting. > CBD Belapur usually suits office-income buyers who value stability over excitement.

Airoli and Mahape: are office clusters better for rental yield or only for occupier depth?

Airoli and Mahape can be strong, but they behave like office ecosystems, not like everyday retail nodes.

Current asking listings show Airoli office rents in triple-digit per sq ft territory in some cases, while Mahape listings show a broad range depending on building grade, furnishing, and floor plate size. That supports the key market truth here: these nodes can attract serious occupiers, but income stability depends much more on tenant profile than in Vashi or Belapur.

Navi Mumbai’s broader office market is also getting attention because rentals remain lower than average Tier-1 city levels, which helps corporate cost logic. CRE Matrix’s 2026 commentary also points to a strong development pipeline in Navi Mumbai, reinforcing the city’s role as a scalable office market.

But here is the real caution. Corporate offices come with heavier friction:

- bigger fit-out expectations

- longer negotiation cycles

- rent-free fit-out periods

- higher CAM in better office parks

- sharper pain if one large tenant exits

Office fit-out cost guidance from JLL and Cushman & Wakefield also shows Mumbai among India’s costliest fit-out markets, which matters because these costs often shape rent-free periods, tenant negotiations, and the first-year yield reality for office assets.

So Airoli and Mahape are not “bad” for yield. They are just less forgiving. They suit buyers who understand office leasing cycles and are not expecting retail-style continuity.

Nerul and Seawoods: why premium positioning does not always mean higher percentage yield

This is one of the easiest places for investors to get confused.

Seawoods and parts of Nerul can command strong absolute rents, especially in premium developments and premium-facing locations. For example, current listings around L&T Seawoods Grand Central and CBRE’s cited quoted rent point show clearly premium office economics. But premium rent does not automatically create premium percentage yield, because the purchase price denominator is usually much higher too.

That is why premium positioning often produces:

- better brand value

- stronger capital preservation

- higher headline rent

- lower percentage yield than expected

Station-linked utility demand in Nerul or Seawoods often behaves differently from Palm Beach-facing prestige stock. The first category may relet more easily because it serves functional daily use. The second may attract better brands or better image, but it can also face longer vacancy because the buyer is paying for visibility and status, not only rent efficiency.

> Caution: > A high monthly rent in Seawoods does not prove a strong commercial yield. The yield can still be compressed if the capital entry price is too rich.

Kharghar, Panvel, and Kalamboli: can lower entry price create better yield, or does tenant depth become the problem?

Lower entry price can absolutely improve headline yield. But it does not remove tenant-depth risk.

Kharghar is now influenced by a bigger future commercial story because CIDCO’s corporate park plan in Kharghar is live in public-facing materials, and newer reports in 2026 show bids being invited for a major International Corporate Park development there. That matters because future commercial expectations can start inflating today’s purchase prices before matching rent depth fully arrives.

Panvel and Kalamboli sit in a different logic. They benefit from highway and corridor strength, lower entry ticket, and future airport-area relevance. But current rental depth still varies sharply building to building and pocket to pocket. That means a lower acquisition cost can make a yield spreadsheet look attractive, while real leasing still remains uneven.

A small local reality check for these nodes

- Kharghar can work better where commercial activity is already functional, not where only future story is being sold.

- Panvel often offers better long-term upside logic than immediate rent certainty.

- Kalamboli can make sense for budget-led occupier demand and corridor-linked activity, but not every commercial unit there deserves a high-yield label.

This is why growth nodes should be treated as future-plus-current bets, not as pure income-safety bets.

Shop, office, or showroom: which asset type changes the yield answer in each node?

A lot changes.

| Asset Type | Usual Rent Stability | Vacancy Sensitivity | Fit-Out Dependency | Nodes That Often Suit It Better | Main Caution |

|---|---|---|---|---|---|

| Retail shop | Higher | Lower | Lower | Vashi, parts of Nerul, selected Kharghar pockets | Frontage, parking, and walk-in quality matter more than raw area |

| Corporate office | Medium | Higher | High | Airoli, Mahape, CBD Belapur | CAM, fit-out concessions, and vacancy between tenants can damage net yield |

| Showroom | High if the location is truly visible | Medium | Medium | Seawoods premium stock, Palm Beach-facing or select main-road stretches | Premium pricing can crush percentage return |

A Vashi retail shop and a Mahape office should not be judged by the same yield logic. Shops depend on frontage, daily catchment, and visibility. Offices depend on access, building systems, lift quality, parking, floor efficiency, and tenant category. Showrooms are even more sensitive because capital value often rises faster than rent.

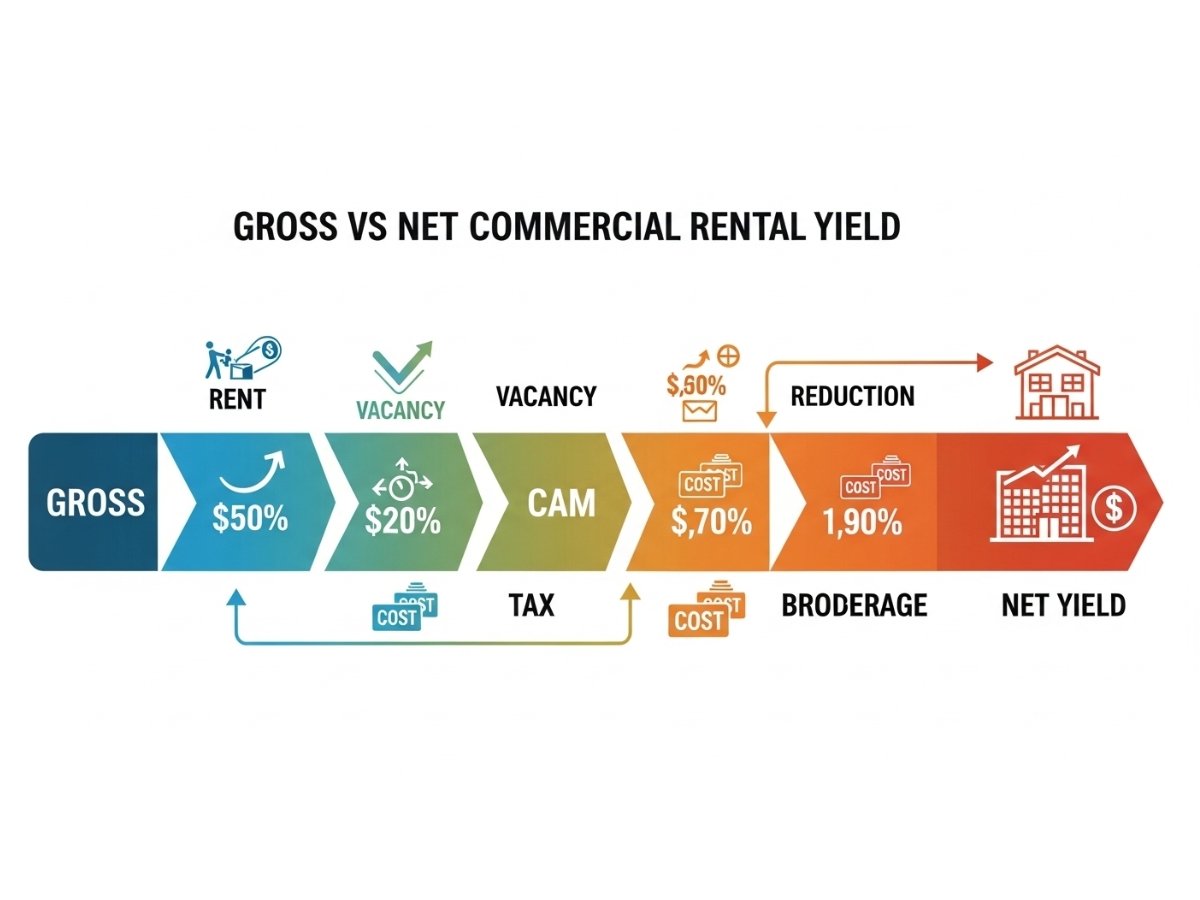

Gross yield is not real yield: which Navi Mumbai costs reduce the number on paper?

This is the section that most commercial buyers need, because brochure yield is rarely the real yield.

The IGR Maharashtra eASR system is meant to give indicative rate information and support valuation/stamp-duty processes. It is not the same thing as actual achieved rentability. MahaRERA, similarly, is useful for project and promoter checks, registration, and timeline visibility, but it does not certify that a finished commercial unit will lease quickly or at a certain rent. :

On the cost side, three local realities matter a lot:

1. Property tax treatment differs by authority. NMMC operates through a rateable-value-based system for property tax, while PMC’s own property-tax framework and documentation show a separate assessment structure and methodology. That means a Panvel-side commercial model should not be copied blindly from an NMMC-side model.

2. CAM can materially reduce office yield. Premium office stock often carries maintenance burdens that materially reduce net income, especially if the lease is not structured carefully. Live listings in Vashi and Belapur also regularly show separate maintenance charges, which is a reminder that gross rent and true rent-in-hand are different numbers.

3. CIDCO transfer friction is real. CIDCO’s Town Services page explicitly says transfer permission is required on payment of transfer charges. In April 2025, CIDCO revised transfer charges upward, and multiple reports highlighted sharp increases for commercial property categories, including a 50% hike for commercial shops and very high slabs for larger commercial properties.

A simple gross-vs-net example

Suppose a buyer acquires a commercial office and the gross yield works out to 8% on paper.

Now deduct:

- one month vacancy buffer

- CAM burden

- brokerage on reletting

- property tax

- basic interior reset or lease refresh cost

That 8% can quickly move closer to the mid-5% or low-6% zone in practical terms. The exact number will vary, but the message is simple: only net yield deserves decision power.

How should a buyer estimate commercial rental yield by node before buying?

A workable local method looks like this:

1) Compare real asking data, not only one broker quote

Pull at least three rent asks and three sale asks from the same building or same micro-pocket. The live market pages for Vashi, Belapur, Airoli, Mahape, and Seawoods show how wide asking ranges can be even within one node.

2) Standardise everything to carpet area

This matters a lot in commercial property. Different projects carry different loading, and yield gets distorted very quickly if one listing is carpet and another is super built-up.

3) Check usability, not only area

A 500 sq ft unit with poor frontage or bad parking can underperform a smaller but cleaner unit in the same sector. Offices need lift quality, parking, floor plate usability, washroom access, and power backup. Shops need frontage, signage, and walk-in logic.

4) Use Ready Reckoner only as a benchmark

The eASR is useful for stamp-duty reference and broad valuation context, not as final market truth.

5) Check authority and project status before trusting the yield

For under-construction or newer commercial projects, MahaRERA should be checked for registration and timeline visibility. Where CIDCO leasehold transfer permission applies, that cost and process should be understood early, not at exit..

When is a “high-yield” commercial deal in Navi Mumbai usually a trap?

Usually when the number is carrying the deal, instead of the property carrying the number.

A high-yield commercial deal should trigger caution when:

- the promised rent looks disconnected from nearby market asks

- the project is in a future-story node but present-day vacancy is visible

- the unit has poor frontage or odd layout

- the tenant type is weak, temporary, or easy to replace with empty space

- the seller is using “assured return” language instead of showing real rental demand

- the building has strong brochure quality but weak actual occupancy

- authority-side transfer charges, maintenance burden, or tax treatment are ignored

> Important warning: > CIDCO-linked transfer friction and local tax treatment can materially alter exit economics. A deal that looks strong on entry can underperform badly once transfer cost, downtime, and reletting cost are included.

Which kind of investor fits which node?

| Investor Type | What Usually Matters Most | Better-Fit Nodes |

|---|---|---|

| Income-first investor | Immediate monthly stability | Vashi, CBD Belapur |

| Safer reletting investor | Low downtime risk | Vashi, station-linked Nerul/Seawoods pockets |

| Office-income buyer | Corporate lease profile | Airoli, Mahape, CBD Belapur |

| Premium branding buyer | Visibility, image, capital safety | Seawoods, select Nerul, premium main-road showrooms |

| Higher-risk growth buyer | Lower entry cost plus future upside | Panvel, Kalamboli, selected Kharghar plays |

| Self-use plus backup-rent buyer | Operational flexibility | Kharghar, Belapur, Sanpada-type practical mixed-use stock |

The wrong commercial buy in the right node can still fail. But the right buyer profile makes the node decision much easier. A conservative buyer should not chase the same unit type that a speculative airport-corridor investor wants.

Final Verdict

The best commercial rental yield node in Navi Mumbai depends on what “best” means.

If the goal is safer monthly income and easier reletting, Vashi and CBD Belapur usually stay ahead. If the goal is office-led corporate leasing, Airoli and Mahape deserve attention, but only with a proper understanding of CAM, fit-out cycles, and tenant replacement risk. If the goal is premium positioning and capital safety, Nerul and Seawoods can make sense, though percentage yield often compresses there. If the goal is higher headline yield and future upside, Kharghar, Panvel, and Kalamboli can work, but only for buyers who accept present-day tenant-depth risk.

That is the real local conclusion: in Navi Mumbai commercial property, the smartest yield decision is not the highest number. It is the cleanest balance of rent continuity, cost leakage, reletting ease, and exit quality.

FAQs

Frequently Asked Questions