Rent vs Buy in Vashi: The Straight Answer Based on 2026 Reality

If you’re deciding between renting or buying in right now, here’s the blunt answer: renting usually makes more financial sense in the short term. Property prices are high (₹1.5–2.5 Cr for a 2 BHK), while rents are relatively moderate (₹40K–₹60K). That creates a huge EMI vs rent gap. Buying only starts making sense if you plan to stay 7–10+ years, want long-term stability, or are betting on appreciation from infrastructure growth.

What Does It Actually Cost to Rent in Vashi Right Now?

Rent in Vashi depends heavily on two things: how close you are to the station and how old the building is.

Quick Rent Snapshot (2026)

| Configuration | Typical Rent Range | Practical Reality |

|---|---|---|

| 1 BHK | ₹25,000 – ₹35,000 | Older CIDCO flats cheaper |

| 2 BHK | ₹38,000 – ₹60,000 | Station-facing = premium |

| 3 BHK | ₹65,000 – ₹1.2L+ | Palm Beach & premium sectors |

| Luxury/Premium | ₹1.5L – ₹3L | Lifestyle-driven demand |

1 BHK, 2 BHK, 3 BHK rent ranges by sector proximity

- Sector 17 / 30 / 30A (walk to station)

+20–30% higher rent

Almost zero vacancy

- Sector 9 / 10 / 11 (interior but central)

Balanced rent, slightly older buildings

- Sector 26 side (newer but farther)

Lower rent, but daily commute cost added

Station-facing vs interior sectors difference

This is where most people underestimate things.

Living walking distance from Vashi station can:

- Save 30–40 minutes daily

- Remove auto dependency

- Justify paying ₹8K–₹15K extra rent

And this is exactly why renting works well hereyou can “buy convenience” without committing crores.

What Does It Cost to Buy a Flat in Vashi in 2026?

Buying in Vashi is expensiveand not just the flat price.

Property Price Snapshot

| Configuration | Price Range | Typical Buyer Reality |

|---|---|---|

| 1 BHK | ₹85L – ₹1.35 Cr | Entry-level ownership |

| 2 BHK | ₹1.3 Cr – ₹2.5 Cr | Most demand segment |

| 3 BHK | ₹2.5 Cr – ₹4.5 Cr+ | Family buyers |

| Premium (Palm Beach) | ₹6 Cr+ | Lifestyle + wealth storage |

Price per sq ft range

- ₹20,000 – ₹28,500 per sq ft average

- ₹30,000+ in prime sectors like 17, 12, 29

- ₹22,000 range in sectors like 26

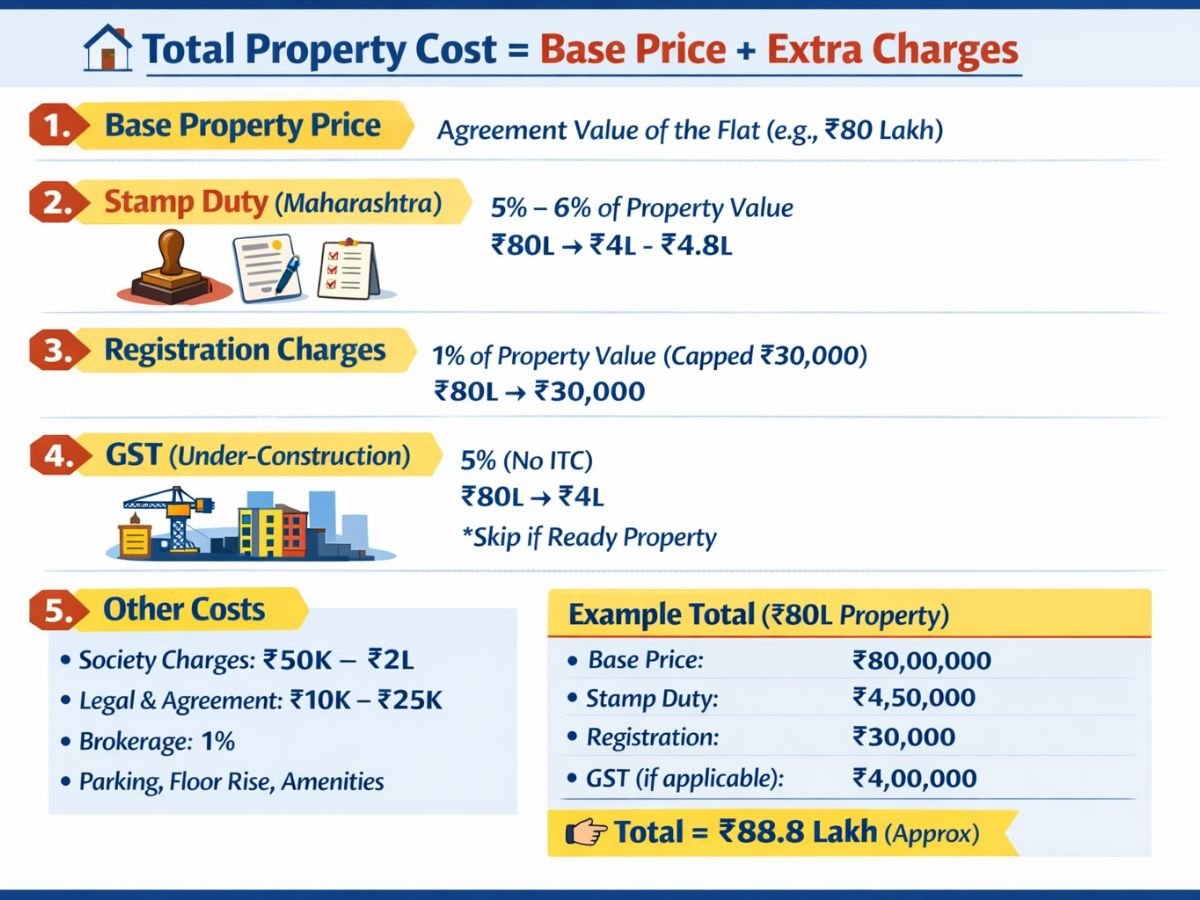

Total cost including stamp duty, registration

Here’s where most buyers get surprised.

On a ₹2 Cr flat, expect:

- Stamp duty: 6–7%

- Registration: 1% (capped ₹30K)

- CIDCO transfer: ₹75K – ₹3L

- Brokerage: 1–2%

- Society charges: up to ₹25K

Total extra cost = 10–15% above property price

So your ₹2 Cr flat actually costs closer to ₹2.2–2.3 Cr all-in.

Rent vs EMI in Vashi A Real Monthly Comparison

Let’s make this real.

Example Scenario

- Property: 2 BHK in Sector 17

- Price: ₹2.2 Cr

- Loan: 80% (₹1.76 Cr)

- Interest: ~8.5%

- Tenure: 20 years

EMI = ~₹1.5–1.55 lakh/month

Rent for same flat

₹55,000 – ₹65,000/month

Monthly Comparison

| Component | Buying | Renting |

|---|---|---|

| Monthly cost | ₹1.5L+ EMI | ₹60K rent |

| Extra costs | Maintenance, repairs | Minimal |

| Flexibility | Low | High |

| Upfront cash | ₹50–70L | Deposit only |

Gap = ~₹90,000/month

This gap is the single biggest reason renting wins in Vashi right now.

Why Rental Yield in Vashi Stays Low (And Why That Matters)

Rental yield in Vashi is roughly 2–3%.

That’s low. And it tells you something important.

- Property prices have already gone up a lot

- Rent has not increased at the same pace

- Demand is strong, but not enough to justify higher yields

What this means for you

- Buying here is not for rental income

- It’s a capital appreciation + stability play

- Investors looking for yield usually prefer other nodes

When Renting in Vashi Actually Makes More Sense

Renting is the smarter move if:

- You may move within 3–5 years

- Your EMI would be 40–50%+ of your salary

- You want to live near the station without paying crores

- You’re unsure about long-term plans in Navi Mumbai

- You don’t want renovation or maintenance headaches

Also, renting lets you upgrade or downgrade easilysomething buyers can’t do.

When Buying in Vashi Starts Making Sense

Buying starts making sense if:

- You plan to stay 7–10+ years

- You want a stable home for family or kids

- You’re okay locking ₹50–70L upfront

- You’re buying in a redevelopment-prone CIDCO sector

- You value ownership over flexibility

Buying in Vashi is less about monthly savingsand more about long-term positioning.

How Long Do You Need to Stay in Vashi to Justify Buying?

This is the real decision filter.

Break-even logic (simplified)

- Transaction costs alone = 10–15%

- EMI interest is front-loaded

- Property appreciation takes time

Break-even = ~8–10 years

If you sell before that, renting usually wins financially.

If you stay longer, buying starts catching up.

Does Vashi Still Have Appreciation Potential or Is It Saturated?

Vashi is not “cheap growth” anymore. But it’s not dead either.

Infrastructure factors

- Upcoming metro connectivity

These improve accessibility and attract higher-income buyers.

Comparison with nearby nodes

- → slightly newer, similar pricing in parts

- → cheaper but less premium perception

Reality check

- Vashi = mature market

- Limited supply keeps prices stable

- Appreciation is likely steady, not explosive

CIDCO Flats vs Builder Flats Does It Change Rent vs Buy Decision?

CIDCO Flats (older buildings)

- Lower entry price

- High redevelopment potential

- Leasehold complications (unless converted to freehold)

Builder Flats

- Modern amenities

- Higher cost

- Higher maintenance (₹5K–₹10K/month common)

What this means for rent vs buy

- Renting → builder flats give better lifestyle

- Buying → CIDCO flats can be smarter if you’re thinking long-term (especially redevelopment play)

Lifestyle Reality: What You Gain and Lose in Renting vs Buying in Vashi

| Factor | Renting | Buying |

|---|---|---|

| Flexibility | High | Low |

| Monthly burden | Lower | Much higher |

| Stability | Medium | High |

| Upgrade/downgrade | Easy | Hard |

| Emotional security | Lower | Higher |

| Hidden costs | Minimal | High |

There’s no perfect answer herejust trade-offs.

Common Mistakes People Make When Deciding Rent vs Buy in Vashi

A few mistakes that keep repeating:

- Ignoring CIDCO transfer charges

- Assuming rent will “cover EMI” (it won’t here)

- Underestimating renovation cost in old flats

- Overestimating appreciation blindly

- Not factoring commute cost/time properly

- Buying just because “rent feels like waste”

In Vashi, emotional decisions can cost ₹20–30 lakh over time.

Final Decision Guide What Should You Do Based on Your Situation

Let’s simplify this.

If you are:

Working professional (mid-20s to mid-30s)

→ Rent

Flexibility matters more than ownership right now

Family planning long-term stay

→ Buy

Stability + school + community matters

Investor looking for returns

→ Avoid or be selective

Low yield market

NRI or HNI buyer

→ Buy

Wealth preservation + premium lifestyle

Already renting in Vashi

→ Upgrade your rental first, then decide

Don’t rush into buying

Conclusion

In Vashi today, renting gives you better monthly cash flow, better flexibility, and access to premium locations without a massive financial commitment. Buying only makes sense if you are thinking long-term, staying at least a decade, or strategically entering a redevelopment opportunity.

A simple way to think about it:

Rent for the lifestyle you want today

Buy only if you’re ready to commit to Vashi for the long run

If you’re still unsure, don’t rush. In this market, waiting and observing is often the smarter financial move than forcing ownership.

FAQs

Frequently Asked Questions