Risks of Buying Property in Flood Prone Area: Navi Mumbai Buyer Checklist

Buying property in a flood-prone area is risky if you do not verify flood history, drainage, zoning, CRZ/CZMP, title records, building approvals, OC, and MahaRERA/CIDCO/NAINA status before paying token money. In Navi Mumbai, Panvel, Ulwe, Taloja, Dronagiri and Uran, waterlogging can be linked to low-lying land, creeks, nullahs, holding ponds, mangroves, or weak stormwater drainage. Verify first; pay later.

Should You Buy Property in a Flood-Prone Area?

You can buy a property in a flood-prone or waterlogging-prone area only after strong verification.

Do not reject every property blindly. But do not treat flooding as a small monsoon problem either.

Flood risk can affect safety, resale value, maintenance cost, loan comfort, insurance, building approvals, and future redevelopment potential.

For wider buyer protection, read property buyer due diligence in Navi Mumbai before paying token money.

Simple rule: no token money until flood risk, title, zoning, CRZ, approvals and OC status are checked.

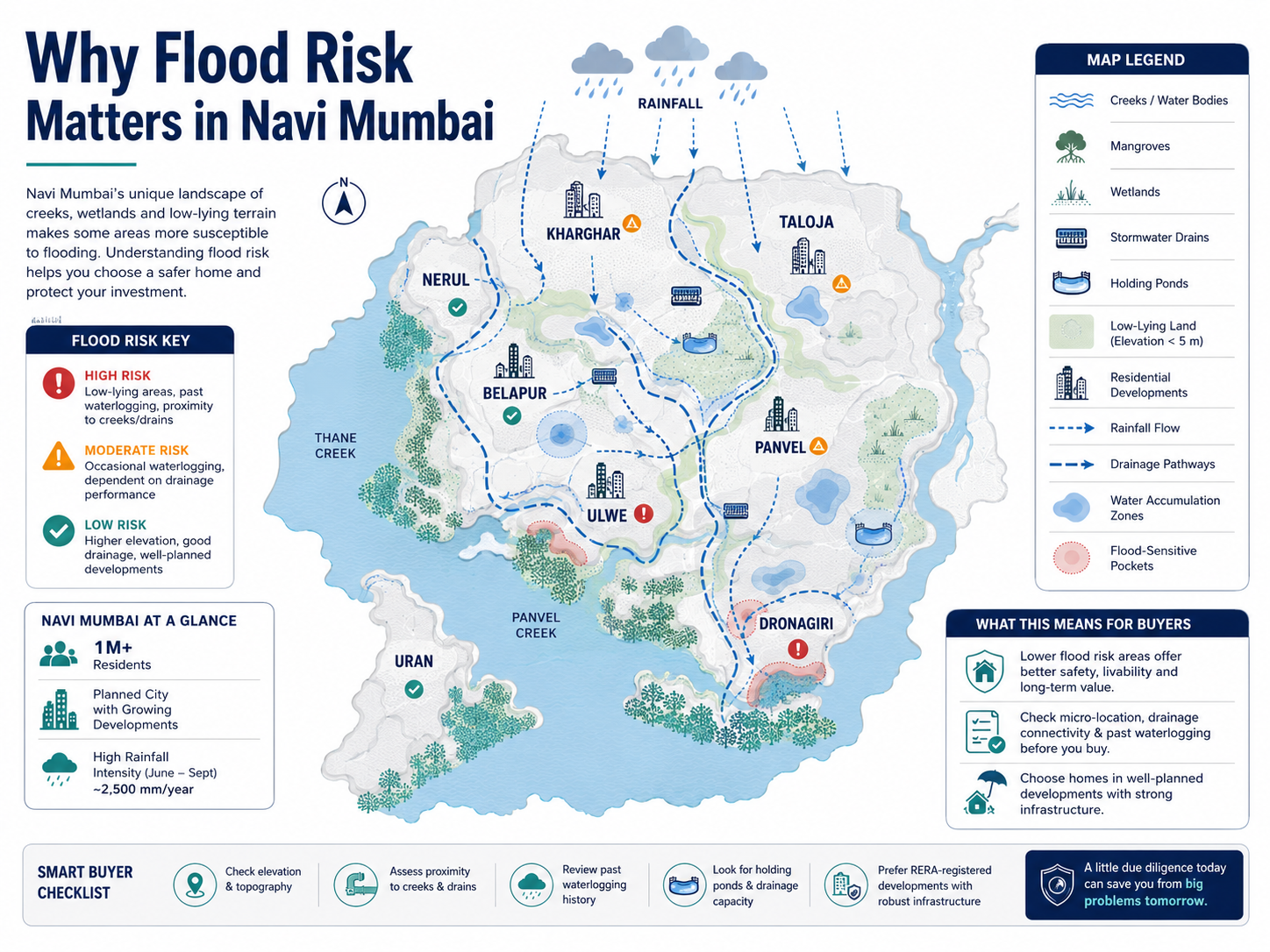

Why Flood Risk Matters in Navi Mumbai

Navi Mumbai is a planned city, but that does not mean every pocket is risk-free.

Some areas are close to creeks, mangroves, holding ponds, wetlands, low-lying roads, stormwater drains and reclaimed land. During heavy rain, high tide or poor drainage, waterlogging can become a real buyer problem.

This is especially important in parts of Navi Mumbai, Panvel, Ulwe, Taloja, Dronagiri, Uran, Kharghar, Raigad and NAINA influence areas.

A building may look good in summer. The real test is monsoon access, drainage, basement condition, stilt parking, lift pits, compound slope and nearby nullah flow.

Main Risks of Buying Property in a Flood-Prone Area

| Risk | What can go wrong | Buyer action |

|---|---|---|

| Physical damage | Damp walls, damaged flooring, lift issues, parking flooding, electrical risk | Inspect during monsoon or after heavy rain |

| Safety risk | Roads blocked, basement unsafe, emergency access affected | Check access roads and society records |

| Resale risk | Buyers may avoid known waterlogging pockets | Ask local residents and check past news |

| Loan/insurance risk | Lender or insurer may raise questions if title, approval or risk is unclear | Confirm before final payment |

| Approval risk | CRZ, floodline, green zone, no-development zone or unauthorized construction issues may arise | Verify with planning authority and lawyer |

| Maintenance cost | Pumps, drainage cleaning, waterproofing and repairs may increase society expense | Check society minutes and repair history |

Flood-Prone Does Not Always Mean Illegal

This point is important.

A property having waterlogging history does not automatically mean the property is illegal.

But flood risk may overlap with other serious issues.

For example:

- Creek-side land may need CRZ/CZMP verification.

- Low-lying land may need drainage and floodline checks.

- Plot land may need zoning and development permission checks.

- NAINA plots may need ZCS, DCPR, TPS and authority approval checks.

- Gaothan or village properties may need stronger title, boundary and revenue-record verification.

- Under-construction projects need MahaRERA, CC, approved plan and OC status checks.

Flood risk is not only a rain problem. It can become a legal, financial and resale problem.

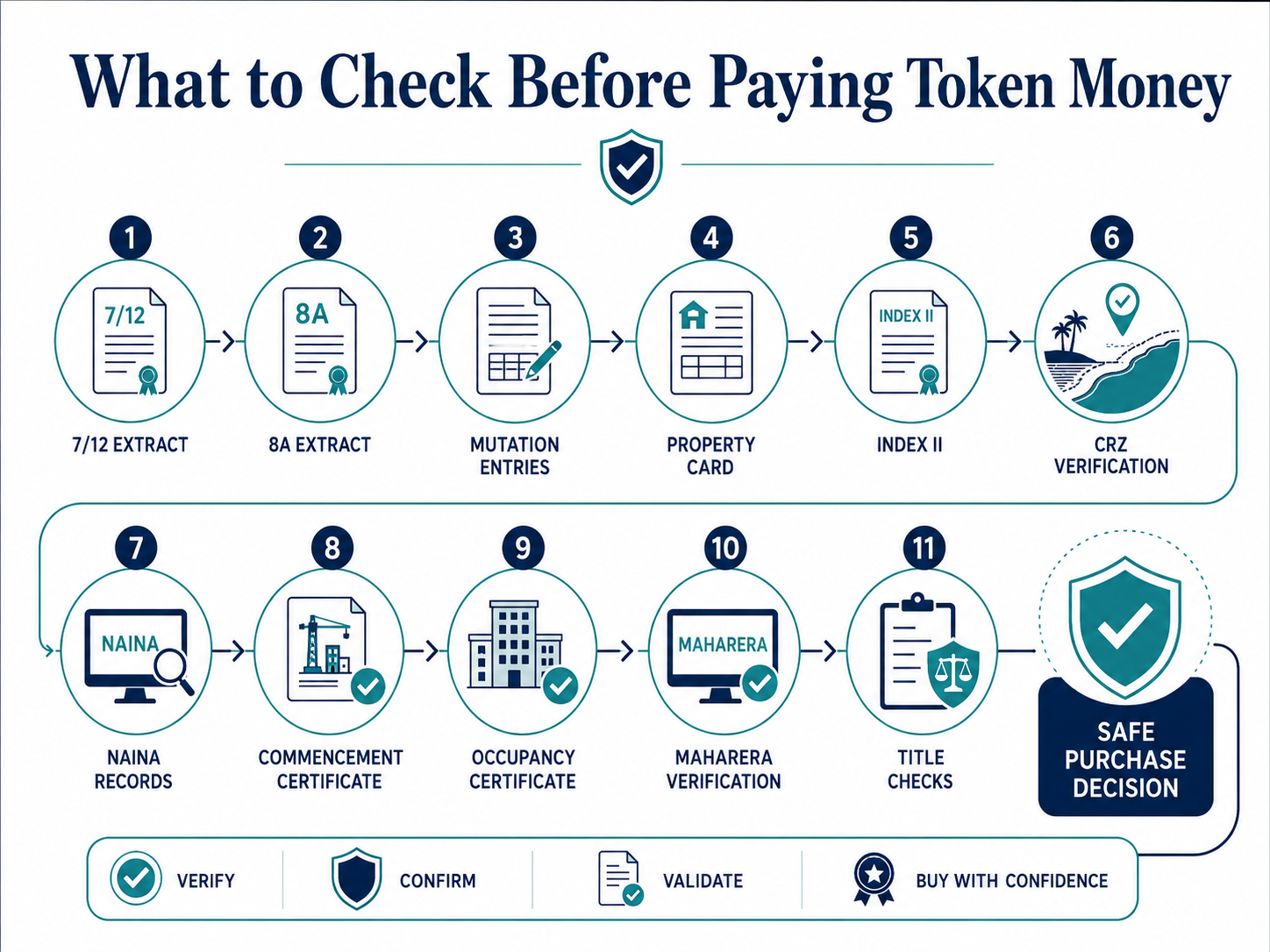

What to Check Before Paying Token Money

Do not pay non-refundable token based on a broker’s WhatsApp documents.

Ask for documents. Then verify them independently.

| Document / Source | What it helps check | Important note |

|---|---|---|

| 7/12 Utara | Land survey details, area, land type, names recorded in revenue records | It supports verification; it does not by itself prove clean title |

| 8A Extract | Account-wise landholding details | Match with 7/12 and seller claim |

| Ferfar / Mutation Entry | Changes after sale, inheritance, partition or transfer | Check whether mutation trail matches the title chain |

| Property Card | Urban property record where applicable | Useful for city property verification |

| Index II | Summary of registered document | Match with sale deed and IGR records |

| IGR e-search / registered documents | Registration history and document trail | Use for title-chain review |

| Development Plan / Regional Plan | Zone, reservation and permitted use | Needed for plot and land transactions |

| NAINA ZCS / DCPR / TPS records | Zone and planning restrictions in NAINA areas | Verify with CIDCO/NAINA source, not broker maps |

| CRZ / CZMP records | Coastal, creek, mangrove and CRZ restrictions | Needed near creeks, coast, mangroves and wetlands |

| Commencement Certificate | Permission to start construction | Verify from authority source |

| Occupancy Certificate | Building-use approval after completion | Essential for resale flat and completed project |

| MahaRERA project page | Project registration, promoter details, complaints, lapsed/revoked/abeyance status | Check before booking under-construction property |

Marathi terms in plain English:

- 7/12 Utara: A land record extract for agricultural or revenue land.

- Ferfar: Mutation entry showing a change recorded in revenue records.

- Index II: A registration summary of a registered document.

- Property Card: A city property record used in many urban areas.

- ZCS: Zone Confirmation Statement, useful in NAINA planning checks.

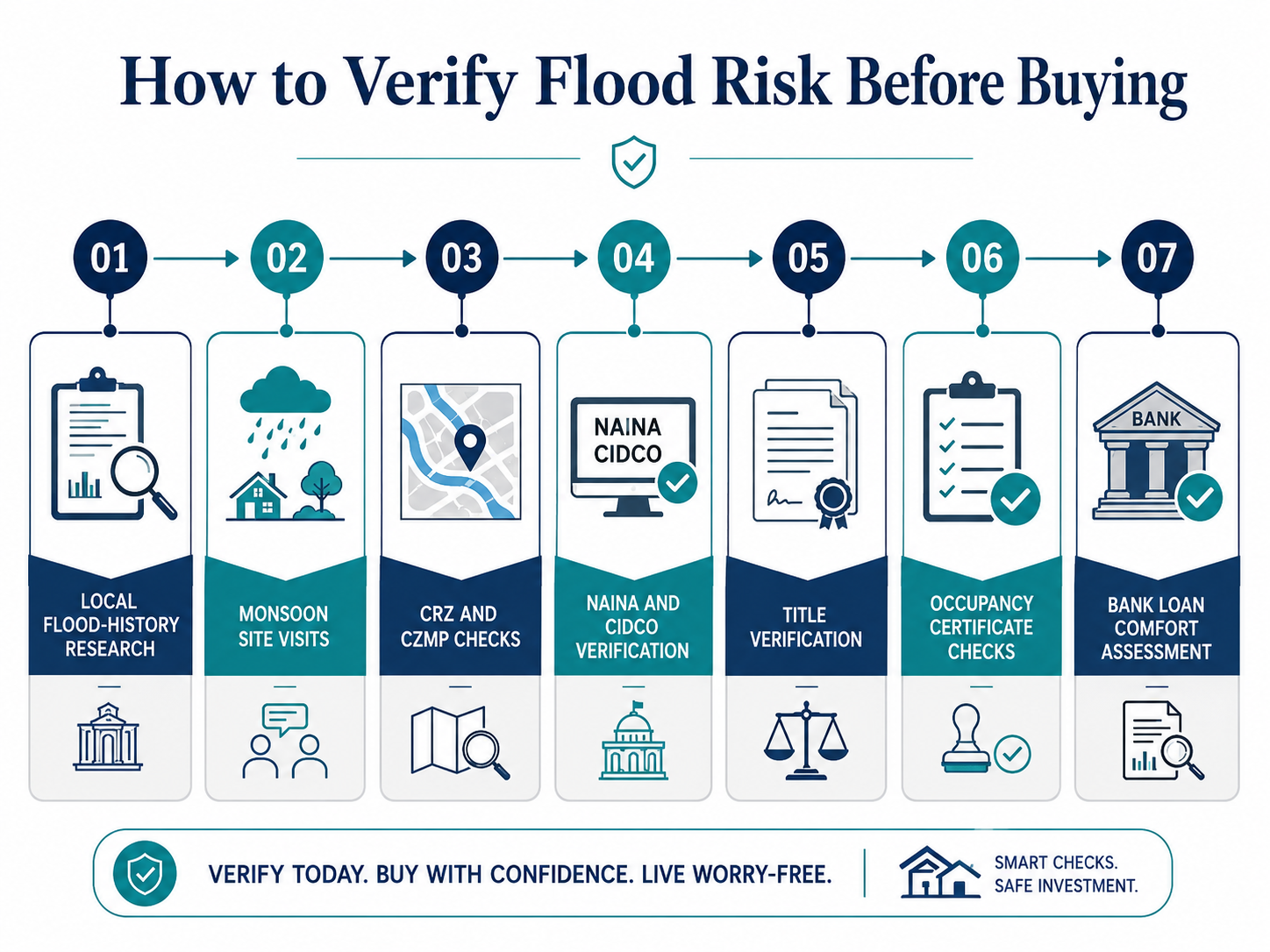

How to Verify Flood Risk Before Buying

1. Check Local Flood History

Ask nearby residents, shopkeepers, security guards and society members.

Ask direct questions:

- Did water enter the building compound?

- Did basement or stilt parking flood?

- Were lifts stopped during monsoon?

- Did access roads get blocked?

- How many times has this happened in the last 3–5 years?

- Was any major repair done after flooding?

Also search local news for waterlogging in the exact sector, village, road or node.

2. Visit During Monsoon

A dry-season site visit is not enough.

Visit during rain or within 24 hours after heavy rain. Check:

- Road level compared to building entrance

- Basement ramp slope

- Lift pit condition

- Parking dampness

- Compound water marks

- Nearby nullah or stormwater drain

- Smell, seepage and wall patches

- Pump room and drainage outlet

- Whether neighbouring buildings are raised higher

If the seller refuses a monsoon inspection, treat it as a warning sign.

3. Check CRZ and CZMP Near Creek or Mangrove Areas

For properties near creeks, mangroves, coast, wetlands or holding ponds, ask for CRZ/CZMP clarity.

This is relevant in parts of Ulwe, Dronagiri, Uran, Nerul, Belapur, Taloja creek-side areas and other coastal or creek-influenced locations.

Do not rely on “CRZ clear hai” from the broker.

Ask a professional to verify the latest CZMP map, CRZ category, mangrove buffer, and authority permission.

4. Check NAINA and CIDCO Approvals

For NAINA and CIDCO-influenced areas, check more than the sale deed.

Verify:

- Zone Confirmation Statement

- Development Plan / Interim Development Plan status

- NAINA DCPR applicability

- Town Planning Scheme impact

- Commencement Certificate

- Occupancy Certificate, if applicable

- Approved layout

- Access road status

- Drainage and infrastructure conditions

For NAINA plots, read NAINA plot verification before buying before committing money.

5. Check Land Records and Title

Flood risk and title risk are different, but both must be checked.

For land, plot, gaothan and village properties, review:

- 7/12 Utara

- 8A

- Ferfar / mutation entries

- Old sale deeds

- Index II

- Property card, where applicable

- Survey map

- Boundaries

- Existing possession

- Any court case or dispute

Read property title search before purchase if the title chain is not clear.

6. Check OC and Building Approval

For a flat, OC matters.

A completed building without OC can create problems with legality, loan, resale, water connection, redevelopment, and civic compliance.

For under-construction projects, check MahaRERA status and promoter updates. For completed or resale buildings, ask for OC, approved plan and society records.

Also read builder approval and OC verification before buying a flat in a risky location.

7. Check Loan and Insurance Comfort

Before final payment, ask your bank whether the property is acceptable for loan processing.

If the property has flood history, missing OC, unclear title, CRZ uncertainty or layout approval issues, the lender may ask questions.

Do not assume loan approval until the lender has checked documents.

Example: NAINA / Panvel Plot Near a Low-Lying Drain

A buyer finds a cheaper plot near Panvel or Taloja. The broker says, “Airport area hai, future residential banega.”

The plot is near a low-lying drain. The 7/12 still shows old agricultural history. The seller says NA permission is not an issue now. The broker asks for quick token.

A smart buyer should check:

- NAINA ZCS

- Development Plan or TPS impact

- 7/12 and mutation entries

- IGR registered documents

- access road

- flood history

- CRZ or creek influence, if nearby

- sanctioned layout

- legal title chain

- latest land-conversion position

If any answer is unclear, pause the deal.

Do not treat “future development” as permission. Verify before transaction.

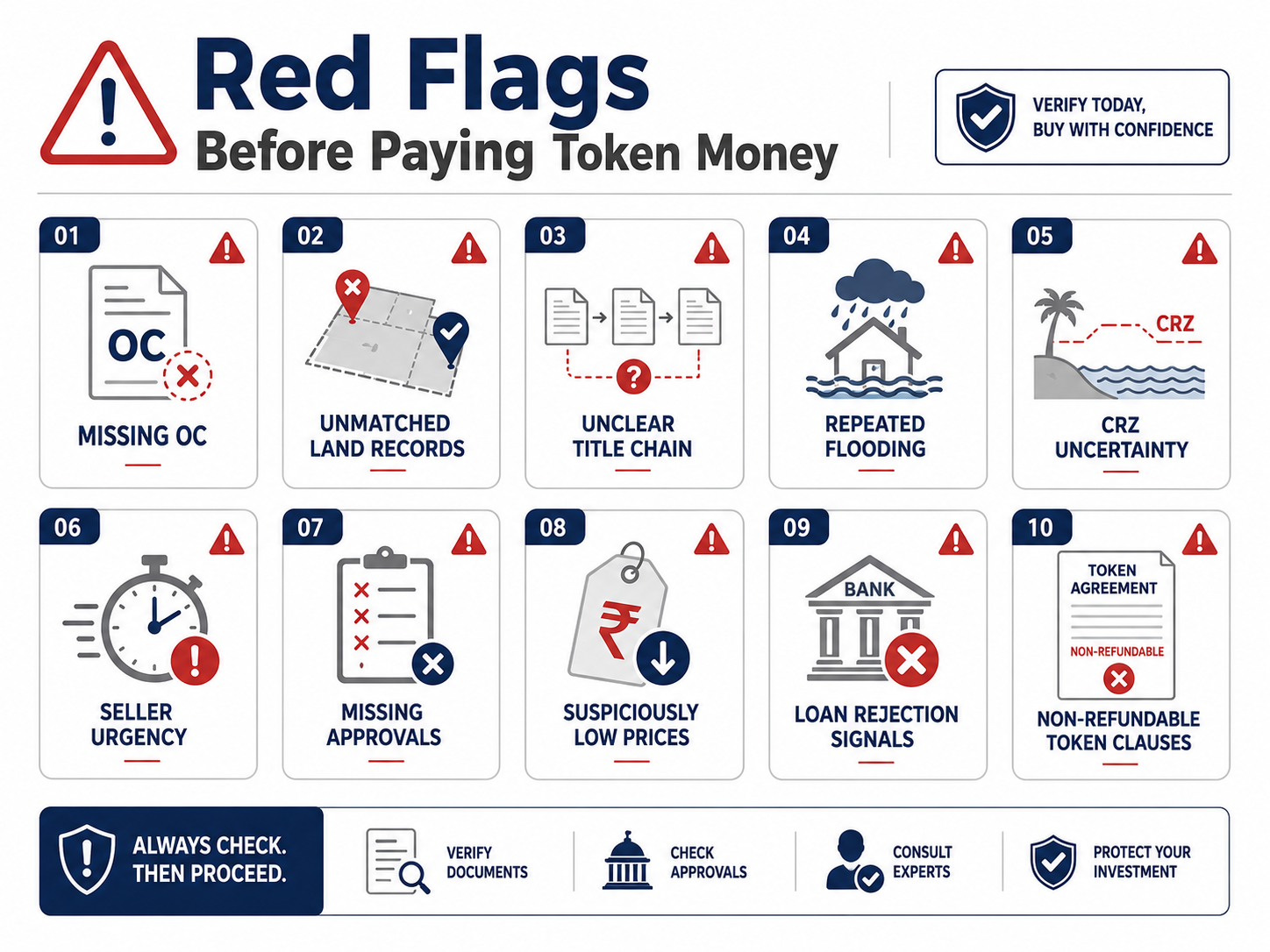

Red Flags Before Paying Token Money

Avoid or pause the deal if you see these signs:

- Seller says, “Token first, documents later.”

- Broker avoids monsoon and waterlogging questions.

- Price is much lower than similar nearby property.

- Building has no OC or only partial OC.

- Plot is close to creek, mangrove, nullah, wetland or holding pond.

- 7/12, sale deed and mutation entries do not match.

- Seller cannot show sanctioned layout or building approval.

- NAINA plot is sold only on “future growth” promise.

- Society members mention repeated flooding.

- Basement has dampness, stains or pump issues.

- Bank is reluctant to fund the property.

- Token receipt is non-refundable even if documents fail.

- Seller refuses lawyer verification.

The biggest red flag is urgency. Genuine property can wait for document verification.

Common Mistakes Buyers Make

1. Buying in summer without checking monsoon conditions. 2. Assuming Navi Mumbai planning means zero flood risk. 3. Trusting only broker-provided maps. 4. Checking title but ignoring CRZ, zoning and drainage. 5. Treating 7/12 as final ownership proof. 6. Ignoring OC in resale flats. 7. Believing “NA not required now” without legal verification. 8. Not checking MahaRERA status for under-construction projects. 9. Paying high non-refundable token. 10. Not asking nearby residents about flood history.

Quick Buyer Checklist

Before paying token money, confirm:

- Exact survey number / plot number / flat number

- Flood or waterlogging history

- Nearby creek, nullah, mangrove, wetland or holding pond

- 7/12, 8A, mutation and property card

- IGR registration trail

- Development Plan / Regional Plan / NAINA ZCS

- CRZ/CZMP status where relevant

- Approved layout

- Commencement Certificate

- Occupancy Certificate

- MahaRERA status, if under construction

- Society records and repair history

- Bank loan comfort

- Lawyer review

- Refundable token clause

Conclusion

Before paying token money for a flood-prone, creek-side, NAINA, CIDCO, gaothan or resale property in Navi Mumbai, get the documents checked first. Start with get property documents verified before token and avoid a deal where the risk is bigger than the discount.

FAQs

Frequently Asked Questions