Risks of Buying Property in CRZ Area: Navi Mumbai Buyer Checklist

Buying property in a CRZ area is not automatically illegal, but it is high-risk. Before paying token money, verify the CRZ classification, approved CZMP map, HTL/LTL distance, mangrove buffer, land records, title, NA/development permission, RERA status, and CIDCO/NAINA/local authority approvals. If the seller cannot give plot-specific documents, pause the deal and verify before transaction.

For the wider risk picture, also read Property Fraud Guide Navi Mumbai.

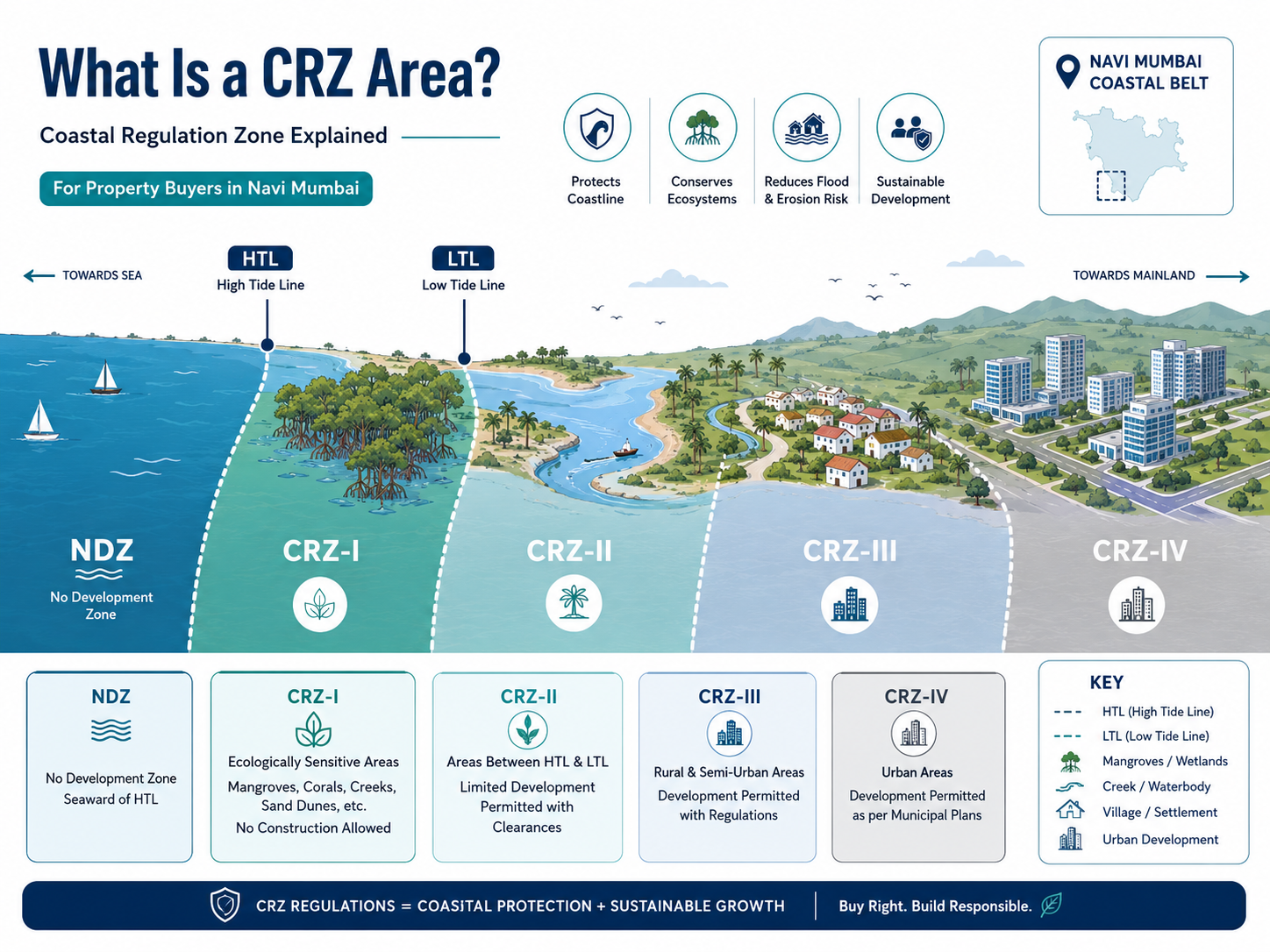

What Is a CRZ Area?

CRZ means Coastal Regulation Zone.

It is a regulated coastal area where construction, land use, redevelopment, reclamation, and certain activities are controlled to protect coastal ecology.

In simple words, if a property is near a sea, creek, mangrove, tidal waterbody, mudflat, salt pan, backwater, or coastal village, CRZ verification becomes important.

Important terms:

| Term | Simple meaning |

|---|---|

| HTL | High Tide Line |

| LTL | Low Tide Line |

| CZMP | Coastal Zone Management Plan map |

| NDZ | No Development Zone |

| CRZ-I | Ecologically sensitive coastal areas |

| CRZ-II | Developed urban coastal areas |

| CRZ-III | Less-developed or rural coastal areas |

| CRZ-IV | Water area and tidal waterbody zone |

A buyer should not decide only by looking at Google Maps, broker statements, or old layout plans. CRZ status must be checked using the latest applicable approved CZMP and plot-level records.

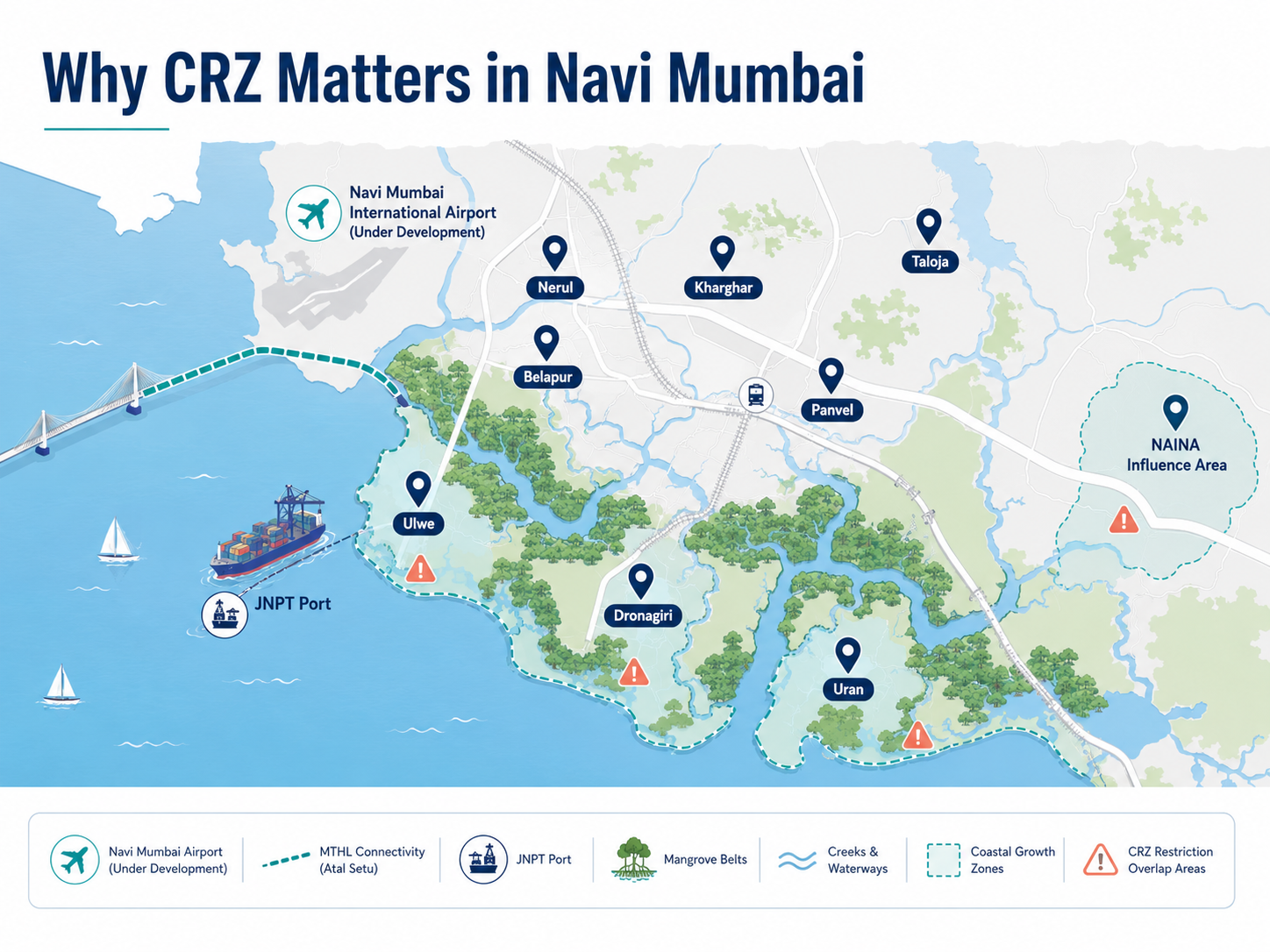

Why CRZ Matters in Navi Mumbai

Navi Mumbai and nearby growth belts have many creek-side, mangrove-side, village, CIDCO, NAINA, and coastal land pockets.

This matters in areas such as Ulwe, Dronagiri, Uran, Nerul, Kharghar, Belapur, Panvel, Taloja, Raigad, Thane creek belt, and NAINA influence areas.

Many deals are sold with growth stories:

- “Airport ke paas hai.”

- “NA soon ho jayega.”

- “CIDCO approval coming.”

- “CRZ issue manageable hai.”

- “Mangrove door hai.”

- “Future mein rate double.”

Growth potential does not remove CRZ risk.

A plot may look attractive because of airport, JNPT, MTHL, CIDCO, or NAINA development. But if the land is affected by CRZ, NDZ, mangrove buffer, green zone, reservation, title dispute, or missing approval, the buyer can face serious loss.

For NAINA-side plots, also read NAINA Plot Fraud Guide.

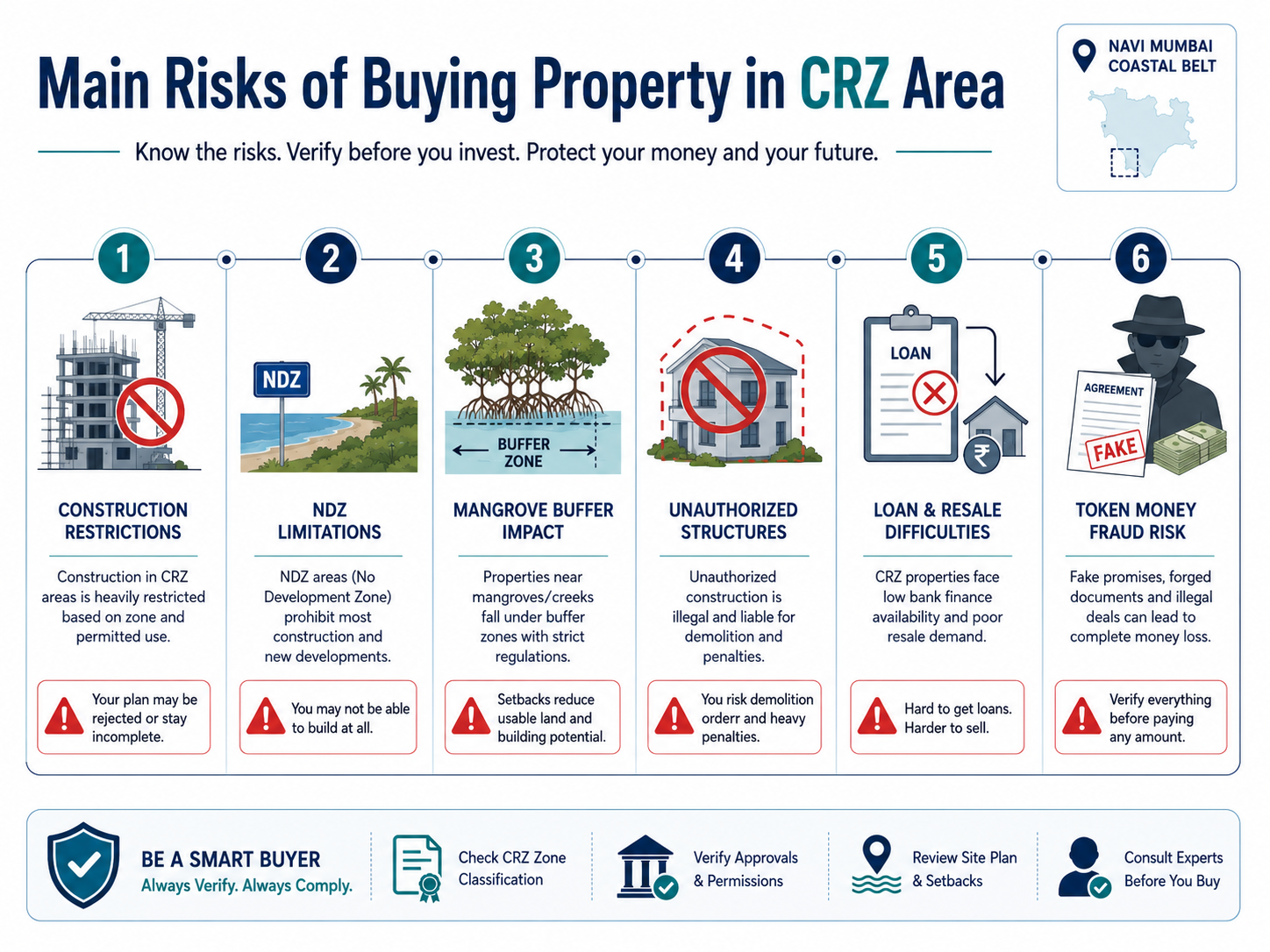

Main Risks of Buying Property in CRZ Area

1. Construction May Be Restricted

The biggest risk is simple: you may buy land but may not be able to build what you planned.

Ownership record and buildability are not the same.

A 7/12 extract, sale deed, or mutation entry may support ownership history, but it does not automatically mean the land is approved for residential construction.

You must separately verify:

- CRZ classification

- CZMP map

- HTL/LTL distance

- NDZ status

- Mangrove buffer

- Zone certificate

- NA or deemed NA applicability

- Layout approval

- Building permission

- Commencement Certificate

- Occupancy Certificate, where applicable

2. Land May Fall in NDZ

Some CRZ areas have No Development Zone restrictions.

If the land falls in NDZ, normal construction may not be allowed or may be heavily restricted. This is especially important for plots near creeks, mangroves, coastal villages, and undeveloped land pockets.

Do not rely on verbal statements like “construction allowed hai.” Ask for written, plot-specific verification.

3. Mangrove Buffer Can Block Development

In Navi Mumbai and surrounding coastal belts, mangroves are a major issue.

A plot may not directly touch mangroves, but it can still be affected by buffer restrictions, access issues, CRZ mapping, or environmental objections.

This is common near creek-side and low-lying land pockets.

If mangroves, mudflats, salt pans, wetlands, or tidal waterbodies are nearby, get a professional CRZ check before paying token money.

4. Existing Construction May Not Be Authorised

A house, bungalow, farmhouse, shed, boundary wall, resort structure, or old village construction may physically exist.

That does not automatically make it legal.

Before buying, check:

- Was the structure approved?

- Was it built before or after applicable restrictions?

- Is there a Commencement Certificate?

- Is there an Occupancy Certificate?

- Is it regularised?

- Does CRZ allow that use?

- Does the planning authority recognise it?

This is especially important for resale flats, gaothan structures, old layouts, and farmhouse-style coastal plots.

For related local risk, read Risks of Buying Gaothan Property.

5. Bank Loan and Resale Can Become Difficult

Banks usually check title, land use, approvals, building permissions, and project documents before giving loans.

If the property has unclear CRZ status, missing NA permission, weak title, no OC, no CC, or unapproved layout, loan approval can become difficult.

Even if you buy without a loan, resale can become a problem later.

Future buyers may ask the same questions you ignored today.

6. Token Money Fraud Risk Increases

CRZ property deals often become risky because buyers are pushed to pay token money before document verification.

Common pressure lines:

- “Sir, airport ke baad rate badh jayega.”

- “Aaj token do, kal documents de denge.”

- “CRZ ka kuch issue nahi hai.”

- “Local level pe sab clear hai.”

- “Ye old gaothan land hai.”

- “NA process mein hai.”

Do not pay token money without written refund conditions if CRZ, title, NA, RERA, or approval verification fails.

For this specific risk, read Token Amount Fraud Guide.

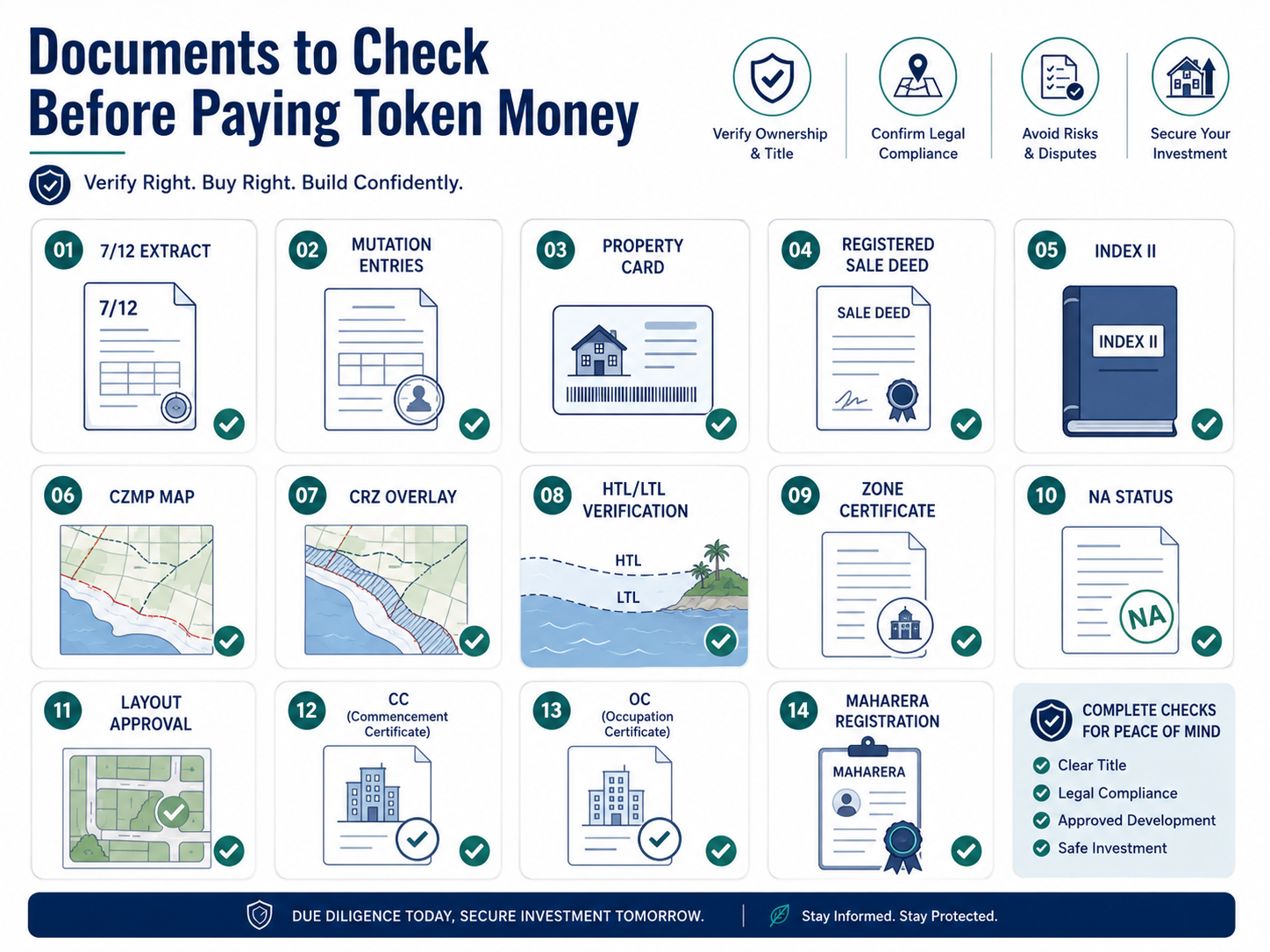

Documents to Check Before Paying Token Money

| Document | Why it matters | Red flag |

|---|---|---|

| Survey number / gut number / CTS number | Identifies the exact land parcel | Seller gives only location pin |

| Village, taluka, district details | Required for official records | Location details keep changing |

| Latest 7/12 extract | Shows land-record entry for rural land | Old extract or name mismatch |

| 8A extract | Helps check holding details | Missing or inconsistent record |

| Mutation / Ferfar entries | Shows past changes in land record | Recent disputed mutation |

| Property card | Important for CTS / city survey areas | Seller has only tax receipt |

| Registered sale deeds | Shows transaction chain | Missing link in ownership chain |

| Index II | Helps verify registered document details | Deed not traceable |

| Approved CZMP map | Shows coastal zone classification | Screenshot without source |

| CRZ plot overlay | Shows plot position against CRZ lines | No plot-level map |

| HTL/LTL demarcation | Checks tidal influence distance | Verbal distance claim |

| Zone certificate / ZCS | Shows planning zone and reservation | Green zone / reservation ignored |

| NA / deemed NA / land-use record | Shows permitted land use status | “NA soon” promise |

| Layout approval | Confirms approved subdivision | Unapproved plotting |

| CC / OC | Important for buildings | Ready flat without OC |

| MahaRERA registration | Needed for applicable projects | RERA number mismatch |

Use How to Check 7/12 and Mutation in Maharashtra as the next land-record article.

How to Verify CRZ Status Before Buying

Step 1: Get Exact Property Identity

Do not start with photos.

Start with records.

Ask for:

- Survey number

- Gut number

- CTS number, if applicable

- Village name

- Taluka

- District

- Plot boundaries

- Latest 7/12 or property card

- Mutation entries

- Registered title documents

Without exact land identity, CRZ verification is weak.

Step 2: Check the Approved CZMP

CZMP means Coastal Zone Management Plan.

This is the key map for checking how a coastal area is classified.

Do not rely on old maps, broker screenshots, or private layout brochures.

Ask a professional to check the latest applicable approved CZMP for the district and plot.

Step 3: Get a Plot-Level CRZ Overlay

A general CRZ map is not enough.

The plot boundary should be marked on the CRZ map. This helps check:

- Whether the plot falls in CRZ

- Which CRZ category applies

- HTL/LTL distance

- NDZ impact

- Mangrove buffer

- Creek or tidal-waterbody influence

- Whether the access road is also affected

This is where many buyers make mistakes.

Step 4: Verify Local Authority Permissions

Depending on location, check with the relevant authority:

- MCZMA

- CIDCO

- NAINA

- NMMC

- Panvel Municipal Corporation

- Revenue office

- City survey office

- Town planning office

- MahaRERA, if project-based

For CIDCO and NAINA areas, also check development plan, DCPR, zone confirmation statement, building permission, CC, and OC records.

For CIDCO-linked risks, read Fake CIDCO Plot Fraud Guide.

Step 5: Do Title Search

Title search means checking whether the seller has the legal right to sell and whether the property has disputes, claims, mortgages, or document gaps.

A proper title check may include:

- 30-year title search

- Registered sale deed chain

- Index II search

- Encumbrance check

- Litigation check

- Public notice

- Heirship check, where applicable

- POA verification, if seller is represented by attorney

For this, read Property Title Search in Navi Mumbai.

Step 6: Add Token Refund Conditions

If you still want to proceed, make token payment only with written conditions.

The receipt or token agreement should mention that token is refundable if:

- CRZ status is adverse

- Title is defective

- NA / land-use permission is not clear

- RERA details mismatch

- CC / OC / layout approval is missing

- Seller fails to provide documents

- Authority verification fails

Avoid cash. Avoid payment to the broker’s personal account.

Red Flags in CRZ Property Deals

Stop and verify if you hear any of these:

- “CRZ issue clear ho jayega.”

- “NA permission coming soon.”

- “Only token do, documents later.”

- “This is gaothan, so no CRZ issue.”

- “Old construction means legal.”

- “Mangrove is far, no need to check.”

- “CIDCO approval coming.”

- “RERA hai, so no need to check other documents.”

- “Owner abroad hai, POA se deal kar lo.”

- “Registry ho jayegi, baaki baad mein.”

- “Low price because urgent sale.”

- “Future airport growth guaranteed.”

- “Google Maps se check kar lo.”

One red flag does not automatically mean fraud, but it is enough reason to stop payment and verify before transaction.

For broker-side risk, read Broker Fraud Warning Signs.

Common Mistakes Buyers Make

Mistake 1: Assuming 7/12 Means Safe Property

7/12 is important, but it does not confirm that construction is allowed.

It supports land-record verification. It does not replace CRZ, zoning, NA, title, layout, or building approval checks.

Mistake 2: Assuming NA Permission Solves Everything

NA means non-agricultural use, but NA status does not automatically remove CRZ, NDZ, mangrove buffer, reservation, development-plan, or building-permission issues.

Maharashtra’s NA and land-conversion rules have seen changes, so buyers should verify the current position with a lawyer, revenue office, and planning authority before transaction.

Mistake 3: Assuming RERA Means Full Safety

MahaRERA registration is useful for checking project details.

But RERA does not mean the buyer should ignore title, land use, CRZ, CC, OC, layout approval, or litigation checks.

For builder-side risk, read Builder Approval Fraud Guide.

Mistake 4: Trusting Old Layouts

Old layouts, old village maps, and old sale documents may not reflect current CRZ, CZMP, DP, reservation, or authority status.

Always check the current records.

Mistake 5: Paying Token Before Verification

This is the costliest mistake.

Once token is paid without a strong refund clause, the buyer loses negotiation power.

Example: Creek-Side Plot Near Uran or Dronagiri

Suppose an NRI buyer is offered a plot near Uran, Dronagiri, Jui, Ranjanpada, or Ulwe.

The broker says:

“Airport ke paas hai. NAINA growth area hai. CRZ ka issue nahi hai. Token do, documents baad mein.”

The buyer should not proceed blindly.

Before token money, the buyer should ask for:

1. Survey/gut number and village details 2. Latest 7/12 and mutation entries 3. Registered sale deed chain 4. CZMP and CRZ classification 5. Plot-level CRZ overlay 6. HTL/LTL and mangrove-buffer check 7. Zone certificate or ZCS 8. NA / land-use / layout status 9. Seller identity and POA verification 10. Written refund clause

Decision rule:

If the seller cannot provide plot-specific CRZ, title, land-use, and authority records, do not pay token money.

What to Check Before Paying Token Money

Use this quick checklist:

- Exact survey/gut/CTS number received

- Latest 7/12 or property card checked

- Mutation entries reviewed

- CZMP checked

- CRZ category checked

- Plot boundary overlaid on CRZ map

- Mangrove and creek distance checked

- Zone certificate / ZCS checked

- NA / deemed NA applicability checked

- Layout approval checked

- CC / OC checked for buildings

- MahaRERA checked for applicable projects

- Title chain reviewed

- Seller identity verified

- POA verified, if applicable

- Token refund clause written

- Payment made only through bank channel

Near the conclusion, link to Verify Property Documents Before Token Money.

Conclusion

Buying property near a creek, mangrove, sea-facing belt, gaothan area, CIDCO node, or NAINA zone can be profitable only if the documents are clean.

Before paying token money, verify CRZ status, title, land records, NA/development permission, RERA, CC, OC, and authority approvals.

Need help checking a Navi Mumbai property before token money? Start with Verify Property Documents Before Token Money.

This is an educational guide. Verify the latest position with the relevant authority or a property lawyer before making a transaction.

FAQs

Frequently Asked Questions