Atal Setu vs Airport Real Estate Impact: Which One Is Doing More for Navi Mumbai Property Prices?

Both the Atal Setu (Mumbai Trans Harbour Link) and the Navi Mumbai International Airport (NMIA) have driven real estate appreciation in the same corridors. But they work differently, affect different buyer profiles, and have played out across different timelines. Atal Setu, inaugurated in January 2024, delivered an immediate connectivity jolt. NMIA, operational from December 2025, is an employment and commercial ecosystem that will take years to fully mature. For buyers trying to understand which infrastructure project carries more weight for their specific decision, here is a direct comparison.

The Core Difference: What Each Project Actually Does

The starting point is understanding what each project is, at its core.

Atal Setu (MTHL) is a connectivity infrastructure project. India’s longest sea bridge at 21.8 km, it connects Sewri in Mumbai to Nhava Sheva in Navi Mumbai. Its direct output is reduced travel time: the journey between South Mumbai and Navi Mumbai dropped from two hours to 20-25 minutes from the day it opened. That is its real estate value proposition in a single sentence. Properties near MTHL exit points became viable primary residences for professionals working in Mumbai’s traditional business districts.

NMIA is an economic infrastructure project. Its real estate impact comes not from cutting commute times but from generating employment, triggering commercial development, attracting logistics hubs, and establishing a new economic center. The airport effect on real estate is broader but slower. It operates over a 5-10 year horizon rather than an immediate post-opening surge.

Neither is simply “better.” They are different types of catalysts.

Timeline: Which Came First and Why It Matters

Atal Setu opened on January 12, 2024. Its impact on real estate was visible almost immediately. Areas like Ulwe, Nhava Sheva, and Panvel saw 10-15% appreciation within six months of the MTHL’s inauguration.

NMIA’s commercial operations began December 25, 2025. However, much of NMIA’s real estate impact was priced in earlier. The announcement effect, land acquisition, and construction activity had been pushing prices in airport-adjacent zones upward since 2019-2020. The 74% appreciation in Panvel between 2021 and 2025 reflects both the airport anticipation and the Atal Setu opening rather than either in isolation.

This sequencing matters for investors. If you bought in Ulwe or Panvel before 2022, you benefited from both announcement effects. If you are entering now, the post-announcement appreciation has already occurred. The remaining upside comes from operational scale-up, NAINA development, and the airport’s employment ecosystem maturing.

Geographic Impact Zones: Where Each Project Hits Hardest

Atal Setu’s impact is concentrated along the Sewri-to-Nhava Sheva corridor. The areas that benefit most are those near MTHL entry and exit points: Nhava Sheva, Ulwe, and Panvel on the Navi Mumbai side. The bridge effectively merged these nodes with South Mumbai for daily commuters.

NMIA’s impact zone is broader and airport-centric. The primary beneficiaries are Ulwe (closest to the runway), Panvel, Dronagiri, and Pushpak Nagar. The secondary impact zone extends to Kharghar, Taloja, and Karanjade as employment-driven rental demand spreads outward.

There is significant geographic overlap. Ulwe and Panvel benefit from both. However, the mechanism is different even in overlapping zones. MTHL made these areas commutable to Mumbai. NMIA is making them self-sufficient economic hubs. Together, this dual positioning is rare in the MMR: a location that is both well-connected to existing business districts and developing its own economic gravity.

Appreciation Numbers: Breaking Down the Contribution

Separating MTHL’s contribution from NMIA’s in the same zone is difficult because they operate simultaneously. But data points allow rough attribution.

Immediately after MTHL’s opening (January 2024 to mid-2024), areas in the direct connectivity corridor saw 10-15% appreciation. This is largely attributable to Atal Setu, as NMIA had not yet opened.

In Kharghar, which benefits significantly from MTHL and metro connectivity but is slightly further from the airport, 5-year appreciation is tracked at around 24%, with 15-20% recorded over the past two years. The airport spillover effect on Kharghar is visible but measured: the primary driver here has been connectivity (MTHL + Metro), not airport adjacency.

In Ulwe, where both infrastructure projects converge most directly, appreciation has been in the 40-80% range over five years. Here, both MTHL and NMIA contributed. MTHL enabled the commuter use case. NMIA created the employment and commercial demand use case. Neither alone would have produced this scale of appreciation.

The current rate benchmarks as of 2026 tell the story:

| Area | Primary Driver | Current Rate (Per Sq Ft) |

|---|---|---|

| Ulwe | NMIA + MTHL | Rs 14,500 – Rs 16,600 |

| Panvel | NMIA + MTHL + Highways | Rs 13,350 – Rs 15,000 |

| Kharghar | MTHL + Metro + ICP | Rs 11,000 – Rs 18,000 |

| Nhava Sheva | MTHL dominant | Moderate appreciation |

| Dronagiri | NMIA future-focused | Rs 6,500 – Rs 9,000 |

Source: Market reports and property consultants. Verify current rates with [MahaRERA](https://maharera.maharegistration.gov.in) registered projects.

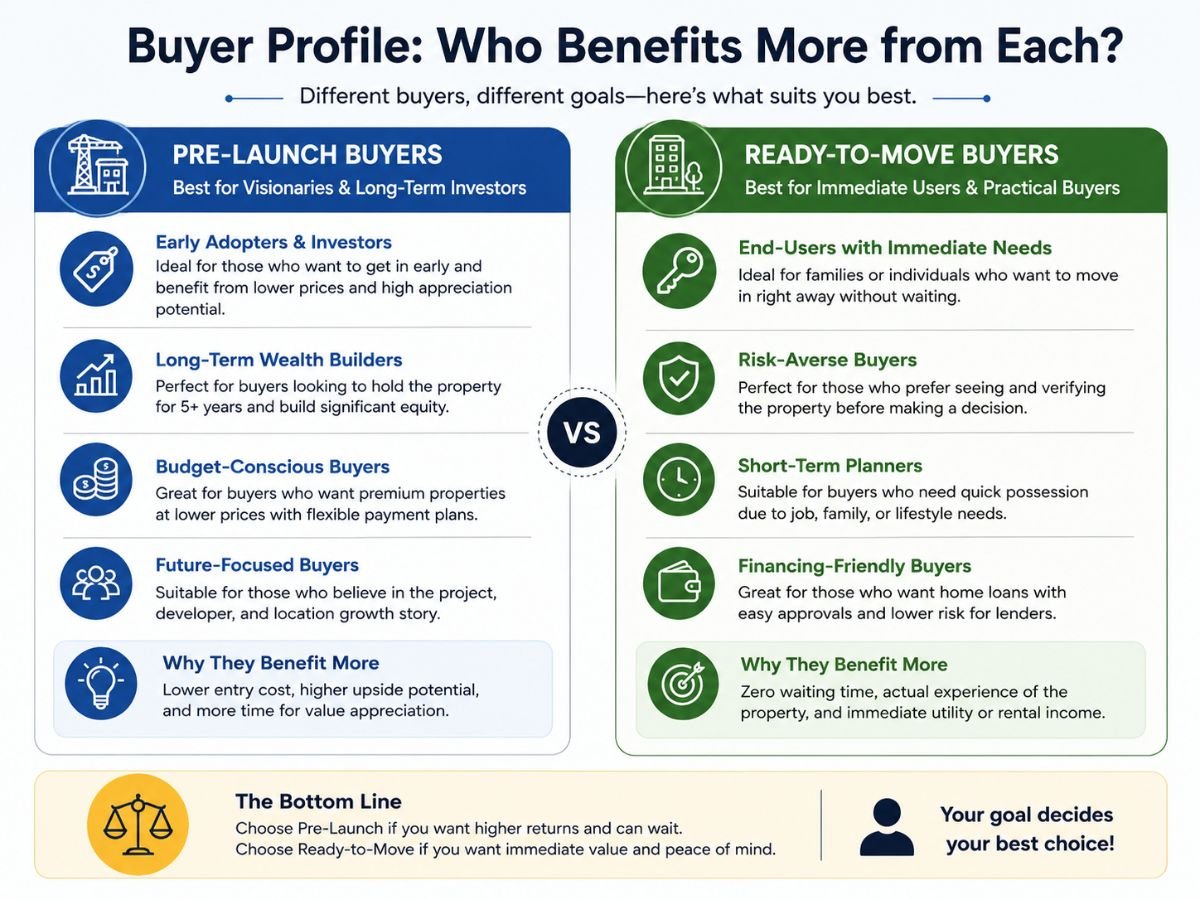

Buyer Profile: Who Benefits More from Each?

MTHL is more immediately useful for end-users who work in Mumbai.

If you work in South Mumbai, BKC, or Nariman Point and want to live in Navi Mumbai, Atal Setu is the direct enabler. What was previously a 2-hour commute is now under 30 minutes with the bridge. This is a permanent lifestyle upgrade that justifies immediate action. For this buyer, the MTHL’s impact is already locked in and not speculative.

NMIA is more relevant for investors with a longer horizon and employment-driven tenants.

If your investment thesis is rental yield from airport-linked professionals, or capital appreciation as the employment ecosystem builds, NMIA is the primary driver. The airport is expected to generate over 1 lakh direct and indirect jobs. Add the 667-acre Aerocity under development by CIDCO and the NAINA infrastructure buildout, and the employment-driven demand is a 7-10 year story.

The overlap zone (Ulwe, Panvel) suits buyers who want both. These are the locations where a working professional can live, commute to Mumbai via MTHL, and also be positioned to benefit from rental demand generated by airport employment. This is why these two nodes have seen the highest combined appreciation.

Infrastructure Maturity: Where Each Project Stands in 2026

Atal Setu is fully operational. Its connectivity impact is immediate and consistent. Traffic volumes have been at or above projections since opening. The only variable is congestion management as volumes increase over time.

NMIA is operational but early-stage. Phase 1 capacity is 20 million passengers annually. The airport is expected to scale to 90 million over multiple decades. Each phase of expansion brings more employment, more commercial activity, and more demand for surrounding real estate. The airport that exists today is a fraction of the economic ecosystem it will become.

This maturity gap is what creates the continued investment case for airport-adjacent zones even after initial appreciation. Investors who entered Bengaluru’s airport zone in 2008-2010 saw the real compounding gains between 2015 and 2022 as the airport scaled and the Devanahalli corridor built economic density. Navi Mumbai is at a comparable stage now.

Risk Profile: Which Carries More Uncertainty?

Atal Setu’s real estate impact is largely realized. The bridge is open, commute times are permanently reduced, and prices in MTHL-adjacent zones have adjusted. The risk of significant downside from MTHL is low. The risk of dramatic additional upside from MTHL alone is also limited.

NMIA’s real estate impact is partially realized, with significant upside contingent on execution. The airport’s ability to drive further appreciation depends on: how fast it scales operations, how quickly the NAINA and Aerocity infrastructure develops, how many jobs are actually created versus projected, and how commercial development in the airport influence zone progresses.

This creates a different risk-return equation. For risk-averse buyers, MTHL-adjacent zones with established livability (Kharghar, established Panvel sectors) offer a more predictable profile. For growth-oriented investors, NMIA-adjacent zones (Ulwe, Dronagiri, Pushpak Nagar) offer higher upside with higher execution dependency.

Combined Effect: Where Both Converge and What It Creates

The most important analytical insight is that for Ulwe and Panvel, the two projects are not in competition. They are compounding.

Atal Setu solved the historical disadvantage of Navi Mumbai: the long commute to Mumbai’s established business districts. NMIA is solving the second historical disadvantage: the lack of self-sufficient economic activity within Navi Mumbai itself.

A location that is within 20-25 minutes of South Mumbai via sea link AND within 10-15 minutes of a 20-million-passenger international airport AND within a planned aerocity zone is, by any reasonable analysis, infrastructure-rich to a degree rarely seen in Indian real estate.

According to [CIDCO](https://cidco.maharashtra.gov.in), the NAINA framework and Aerocity plans are designed to ensure that airport-adjacent development follows a master plan rather than uncontrolled sprawl. This planning oversight reduces the risk of the infrastructure without the matching urban development that has plagued some other airport zones in India.

Market observers are forecasting 10-20% annual appreciation in Ulwe and Panvel through 2027, anchored by the combined infrastructure effect. [Verify current forecasts and project-specific approvals with a RERA-registered agent before investing.]

Which Should Drive Your Decision?

The framing of “Atal Setu vs Airport” is most useful when you are deciding between two specific locations that each benefit from one project more than the other.

Choosing between Kharghar (MTHL + Metro dominant, established market) and Dronagiri (NMIA future-focused, emerging market) is a cleaner version of this tradeoff. Kharghar gives you current livability and steady appreciation. Dronagiri gives you lower entry and higher growth potential, with the airport as the primary long-term driver.

If you are looking at Ulwe or Panvel, the vs. framing dissolves. Both projects matter in equal measure, and the combined infrastructure depth is the investment thesis.

FAQs

Frequently Asked Questions