How Data Center Growth Is Changing Industrial Land in Navi Mumbai

Data center growth is changing industrial land in Navi Mumbai, but not in a simple “all prices are rising” way. The real impact is concentrated in a few infrastructure-ready belts where power depth, fiber connectivity, parcel scale, and approval practicality actually support this use. That is why some land parcels in Airoli, Rabale, Mahape, Ghansoli, and parts of the Panvel-side story are becoming more strategic, while many ordinary industrial plots are only riding borrowed hype.

What data center growth is actually doing to industrial land in Navi Mumbai

The first thing to understand is that this is not a normal industrial upswing. Data centers do not choose land the way a warehouse, workshop, or small factory does. They need unusually deep power access, reliable network paths, stronger resilience, and larger planning logic. Because of that, the boom is creating two industrial land markets inside the same city-region.

One market is for operator-grade strategic land. This is the land that can realistically support a serious digital infrastructure play. The other market is ordinary industrial land that now gets marketed using data center language even when the actual parcel is too small, too weak on infrastructure, too restricted in title, or too impractical to support such a project.

Quick summary

| The Structural Change | Navi Mumbai Ground Reality |

|---|---|

| Selective Demand | Not every MIDC plot benefits; the shift is surgical, not a blanket boom. |

| TTC Strategy Shift | Airoli, Mahape & Ghansoli win due to infra depth, not just branding. |

| Parcel Value Growth | Contiguous land with power/network relevance beats fragmented plots. |

| The "Premium" Hype | Sellers quoting "Data Center Premiums" on ordinary plots without real basis. |

| Occupier Pressure | Traditional manufacturing gets priced out of prime TTC corridors. |

| Built-Stock Paradox | Old sheds only gain value if the underlying land is redevelopment-worthy. |

Which parts of Navi Mumbai are truly benefiting, and which parts are mostly riding the data-center halo?

The biggest mistake in this topic is treating Navi Mumbai like one uniform industrial geography. It is not. Each belt has a different logic.

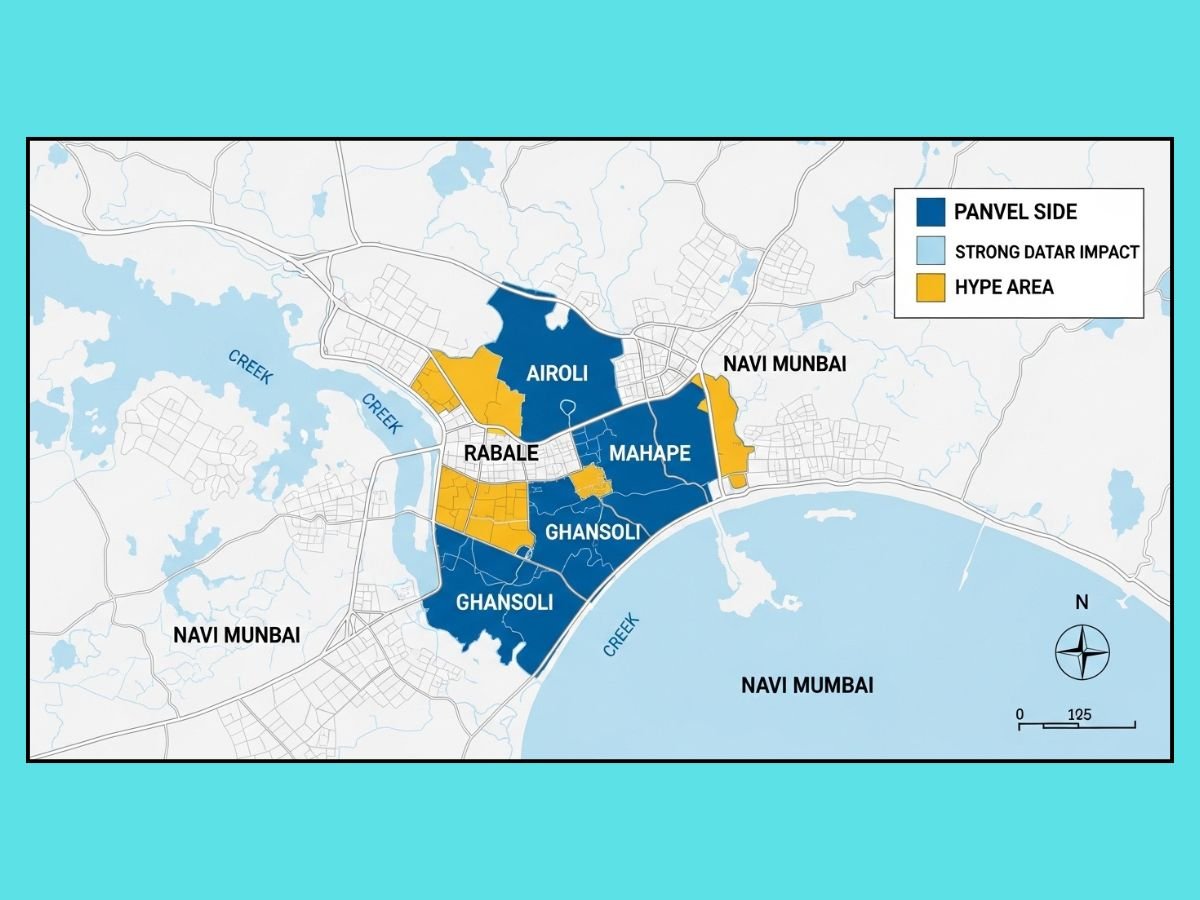

Airoli–Rabale–Ghansoli: where the cluster story is strongest

This is where the strongest cluster narrative sits. The reason is not commuter buzz, not station branding, and not general “tech area” perception. The reason is corridor depth.

These belts already have stronger digital infrastructure presence, serious operator interest, and a market memory that matters. When large operators, hyperscale campuses, or AI-ready facilities choose a belt, that location starts behaving differently. Sellers become more aggressive. Assemblies become harder. Small industrial users start feeling cost pressure. Brokers start stretching the story to nearby stock.

Rabale in particular now has a much stronger credibility than a normal industrial node because real operators are already present there. That matters far more than brochure language. A land parcel near such a corridor may deserve closer attention, but only if the parcel itself can pass the actual operator test.

Mahape: why campus-scale supply and infrastructure depth matter

Mahape is important for a slightly different reason. It supports a campus-style reading of the market. This is where the conversation is less about one isolated industrial plot and more about whether the micro-market can sustain multi-building, high-load, long-horizon infrastructure.

That changes land behavior. A seller in a campus-worthy belt starts thinking less like a normal industrial owner and more like a strategic landowner. But again, this only works for the right land. Mahape does not magically turn every old industrial property into a data center candidate.

Panvel-side large-campus logic: where the story changes

Panvel-side and the wider southern growth story should not be mixed blindly with TTC logic. The appeal here is not identical. The Panvel-side narrative is more about scale, larger campus possibility, and future-oriented land assembly rather than the dense vertical cluster logic seen in TTC belts.

This makes the Panvel story interesting, but also more vulnerable to over-marketing. Many locations get sold using airport, future growth, and hyperscale language. Some of that is valid. Some of it is halo. A large parcel with clean land logic and execution feasibility is one thing. A random industrial plot being called “next data center zone” is another.

Belts that may sound industrial but do not automatically become data-center plays

This is where buyers lose money. An area can be industrial on paper, industrial in appearance, and industrial in local conversation, yet still fail the real operator-grade test.

A small fragmented plot. A parcel with weak power practicality. A low-lying site with resilience problems. A leasehold structure with difficult transfer conditions. A belt too far from meaningful network depth. Any of these can break the premium story.

So the correct question is not, “Is this in an industrial belt?” The correct question is, “Is this actually infrastructure-ready for a serious data-center-grade use?”

Why some industrial plots become strategic in a data-center cycle while others do not

This is the heart of the topic. A parcel becomes strategic not because the owner says “data center potential,” but because the land can support the real requirements behind that use.

Power depth and upgrade practicality

Power is the first filter. If the site does not have serious high-capacity power logic around it, the rest of the conversation becomes weak very quickly.

This is why ordinary industrial economics and data center economics are not the same. A plot that works for a workshop, storage unit, or small manufacturing use may still be useless for a data center story. Buyers must think in terms of actual upgrade practicality, not theoretical possibility.

Fiber density and network relevance

The second filter is connectivity depth. Data centers need robust network logic, not just one cable story and not just “good internet in the area.” The market premium becomes more believable when the corridor has real network relevance.

That is why cluster belts matter. Once multiple serious operators enter a belt, the location gains institutional credibility. Nearby landowners then try to price off that credibility. But unless the parcel itself can tap into that ecosystem meaningfully, the premium remains borrowed.

Parcel size, shape, frontage, and internal movement

Scale matters much more than many local sellers admit. The smaller and more fragmented the parcel, the weaker the real operator case usually becomes.

This is why land assembly is such a big hidden theme in this market. In many cases, the story is not about one magic plot. It is about whether multiple neighboring plots can be combined into something institutionally useful.

Water, flood, and 24x7 operational resilience

This point gets ignored far too often in local property discussions. Navi Mumbai’s industrial geography is not risk-free. Some low-lying pockets and monsoon-sensitive areas carry resilience questions that become much more serious for 24×7 digital infrastructure than for basic industrial use.

A site can look attractive on a rate-per-acre basis and still fail the resilience test. For a true operator-grade buyer, that matters.

Title, lease, and land-use fit

This is where many premium stories collapse. Industrial appearance is not legal proof of sanctioned suitability. Leasehold conditions, transfer permissions, development obligations, and land-use fit all matter.

In Navi Mumbai, that means MIDC and CIDCO context cannot be treated casually. A good-looking parcel with a messy authority-side structure can become expensive dead stock for the wrong buyer.

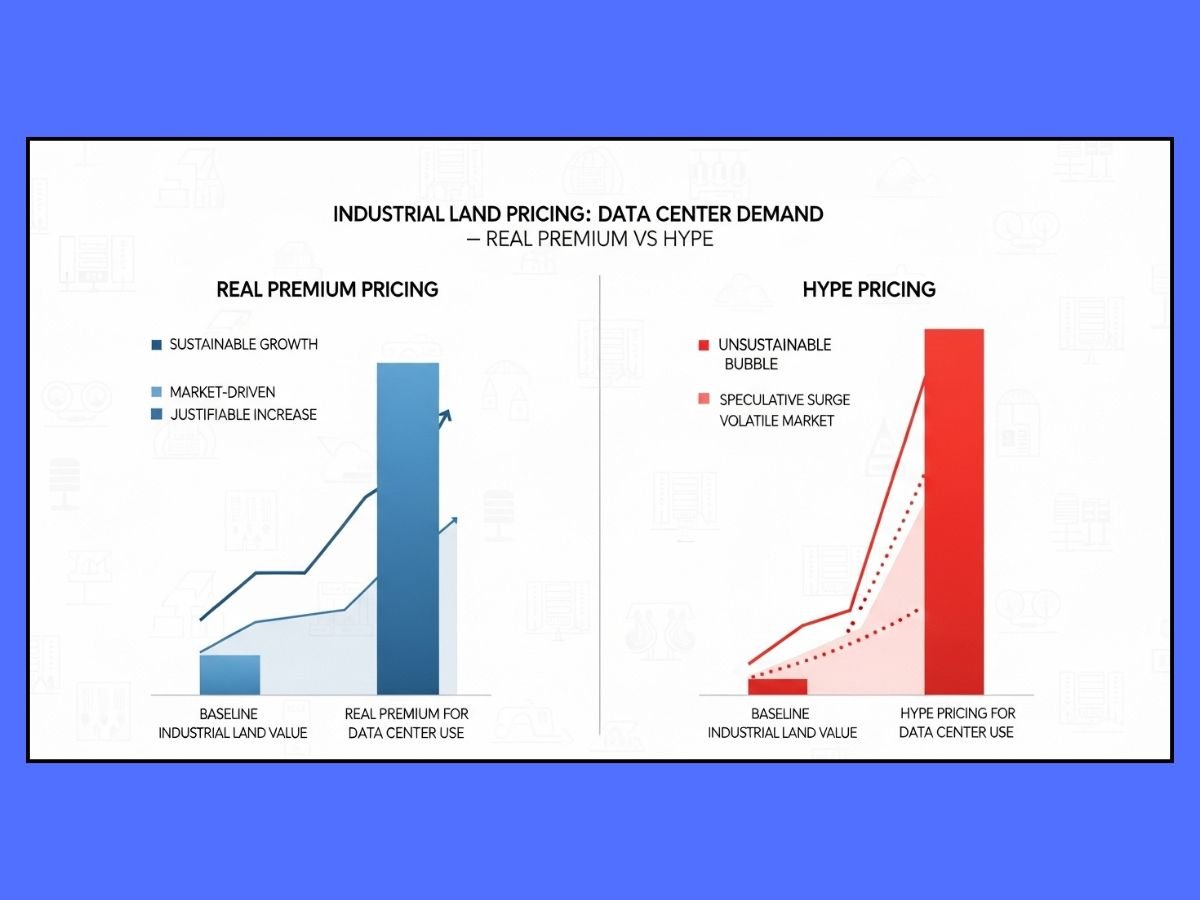

Is this trend pushing up all industrial land prices, or creating a narrow premium band?

It is creating a narrow premium band, not a universal repricing.

That premium is strongest where five things come together: serious infrastructure, genuine cluster credibility, usable parcel size, cleaner execution path, and believable operator-grade suitability. When these align, land can become meaningfully more strategic.

But outside that band, many owners are simply raising expectations because they have heard about hyperscale investment, AI demand, or big operator names nearby. That creates a dangerous pricing gap between seller fantasy and buyer reality.

The practical reading is simple. Large, infrastructure-ready, execution-friendly parcels may command stronger attention. Smaller resale plots, weakly connected land, or old built stock with legal or technical limitations usually do not deserve the same valuation logic.

How data center growth changes the math for landowners in Navi Mumbai

Landowners now have to think more carefully. The old logic of hold, sell, or lease is no longer enough.

If the parcel is genuinely strategic, holding may make sense for some time, especially if the corridor is deepening and nearby infrastructure is strengthening. If the parcel is already attractive to institutional buyers, selling into the premium may be the smarter move.

If the owner has a smaller or awkward parcel, joint development or assembly may become more valuable than a direct sale. In many cases, the biggest value unlock does not come from one owner alone. It comes from combining land into a scale that finally becomes relevant.

At the same time, many owners must accept a less glamorous truth. A lot of land will still be better suited to normal industrial or logistics use. Trying to force a data center story onto every parcel can delay decisions, distort pricing, and ultimately reduce liquidity.

What ordinary industrial buyers and occupiers should worry about when data-center demand enters the same belt

This trend is not automatically good news for everybody. In fact, for many normal industrial buyers and occupiers, it creates fresh problems.

The first problem is rising seller expectation. Even when a plot is not truly operator-grade, owners start quoting as if it is. That can distort acquisition math for normal industrial users.

The second problem is shrinking availability of good land. Once strategic belts get tighter, ordinary occupiers have fewer practical choices. That can push them into weaker locations or force them to compromise on operations.

The third problem is mismatch. A data-center-driven premium does not always match warehouse, workshop, or light industrial economics. A business may end up paying a land cost that its own use case cannot justify.

This is why ordinary occupiers should not buy into corridor hype. They should buy only if the land works for their own business model first.

Can every industrial plot be turned into a data-center opportunity? Usually no

This answer should be blunt: usually no.

Sanctioned use is not the same as marketing language

A seller can call a site future-ready, hyperscale-ready, AI-ready, or tech-infra-ready. None of that is enough. Marketing language is cheap. Sanctioned use, legal fit, and execution feasibility are what matter.

Lease conditions, title structure, and transfer restrictions matter

A large part of Navi Mumbai’s industrial land ecosystem sits inside leasehold and authority-controlled structures. That means transfer conditions, NOCs, charges, and compliance history can materially change feasibility.

Many speculative buyers ignore this until late. That is a mistake.

Infrastructure upgrade cost can kill the premium story

Even if a plot looks promising, the required upgrades may be so expensive or slow that the premium disappears in practice. This is one of the most common gaps between headline value and usable value.

Small fragmented plots often fail the real operator test

A small industrial plot may still be a fine industrial asset. But it is usually not the same thing as a serious data center land opportunity. In this topic, scale is not a minor detail. It is a core filter.

How this trend is changing older sheds, galas, and built industrial stock nearby

Older built stock is affected, but not in the way many people assume.

A forty-year-old shed does not become data-center-grade because the corridor has become hotter. In many cases, the building itself is obsolete for that use. Ceiling height, structural capacity, circulation, services, and resilience may all be wrong.

What changes instead is the value of the underlying location. Some old sheds and galas become more strategic as land-bank plays, redevelopment plays, or assembly pieces. Others simply get overquoted without real redevelopment logic behind them.

So buyers should separate building value from land value. In a rising digital corridor, the land may become more interesting even when the existing structure does not.

What to verify before paying a “data center premium” for industrial land in Navi Mumbai

| Verification Point | Why It Matters (The "So What?") |

|---|---|

| Actual Power Feasibility | Without stable power, the premium story for data centers or mfg weakens instantly. |

| Fiber & Connectivity | The corridor must support meaningful network depth for modern digital-linked businesses. |

| Parcel Size & Assembly | Fragmented land often fails operator logic for large-scale warehousing or campuses. |

| Flood Resilience | Low-lying sites (especially in coastal belts) can become expensive operational mistakes. |

| MIDC/CIDCO Title | Leasehold restrictions or transfer hurdles can kill viability late in the deal. |

| Sanctioned Use Fit | Industrial-looking land is not automatically suitable for all niche uses (like Data Centers). |

| Evidence vs Asking Price | Asking rates are often inflated by "Airport Halo"; demand actual market proof/closed deals. |

Who should act on this trend now: investor, landowner, occupier, or broker?

Landowners with larger, cleaner, strategically placed parcels are in the strongest position. They should think carefully, not emotionally. The right buyer, the right timing, or the right assembly strategy can create real value.

Brokers can benefit too, but only if they understand the difference between real operator-grade land and overmarketed stock. In this market, shallow hype may win attention for a few weeks, but informed buyers eventually ask harder questions.

Ordinary investors should be much more careful. Buying a small industrial plot just because the area has data center buzz is not a strong strategy. The risk of overpaying is high.

Occupiers should be defensive and practical. If their belt is getting hotter because of tech-infra demand, they need to review affordability, lease security, and future expansion options early.

Conclusion

Data center growth is definitely changing industrial land in Navi Mumbai, but the real story is selective advantage, not blanket appreciation. The winners are not “all industrial plots.” The winners are the parcels and corridors that can genuinely support deep power, strong network relevance, workable scale, and practical execution. Everyone else is operating somewhere between partial spillover and pure halo.

That is the key market takeaway. In Navi Mumbai, data center-led land value is now a serious theme, but it is still a precision story. Buyers who understand the difference between operator-grade strategic land and ordinary industrial land riding borrowed hype will make better decisions. Buyers who do not will end up paying a premium for a headline, not for a usable asset.