How Seawoods Grand Central and Nexus Shape Commercial Demand

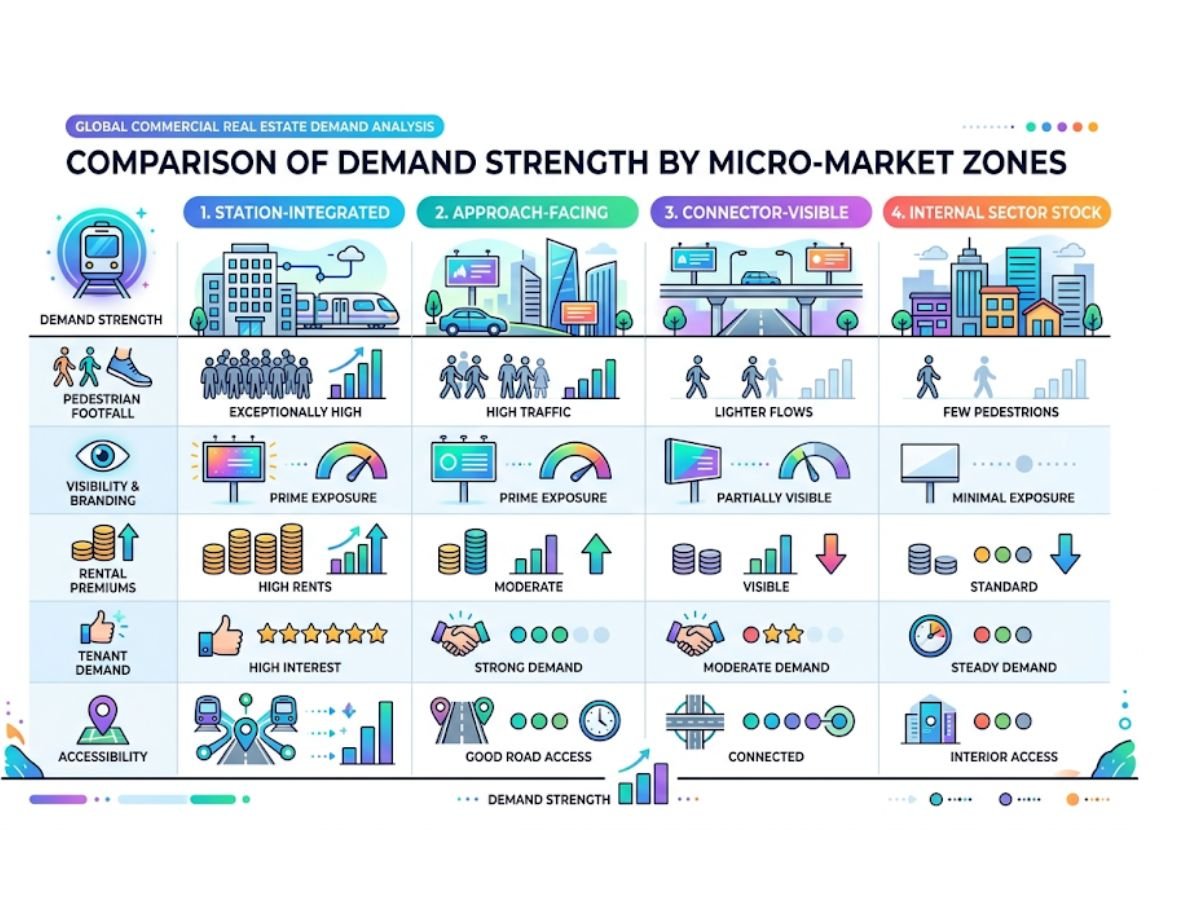

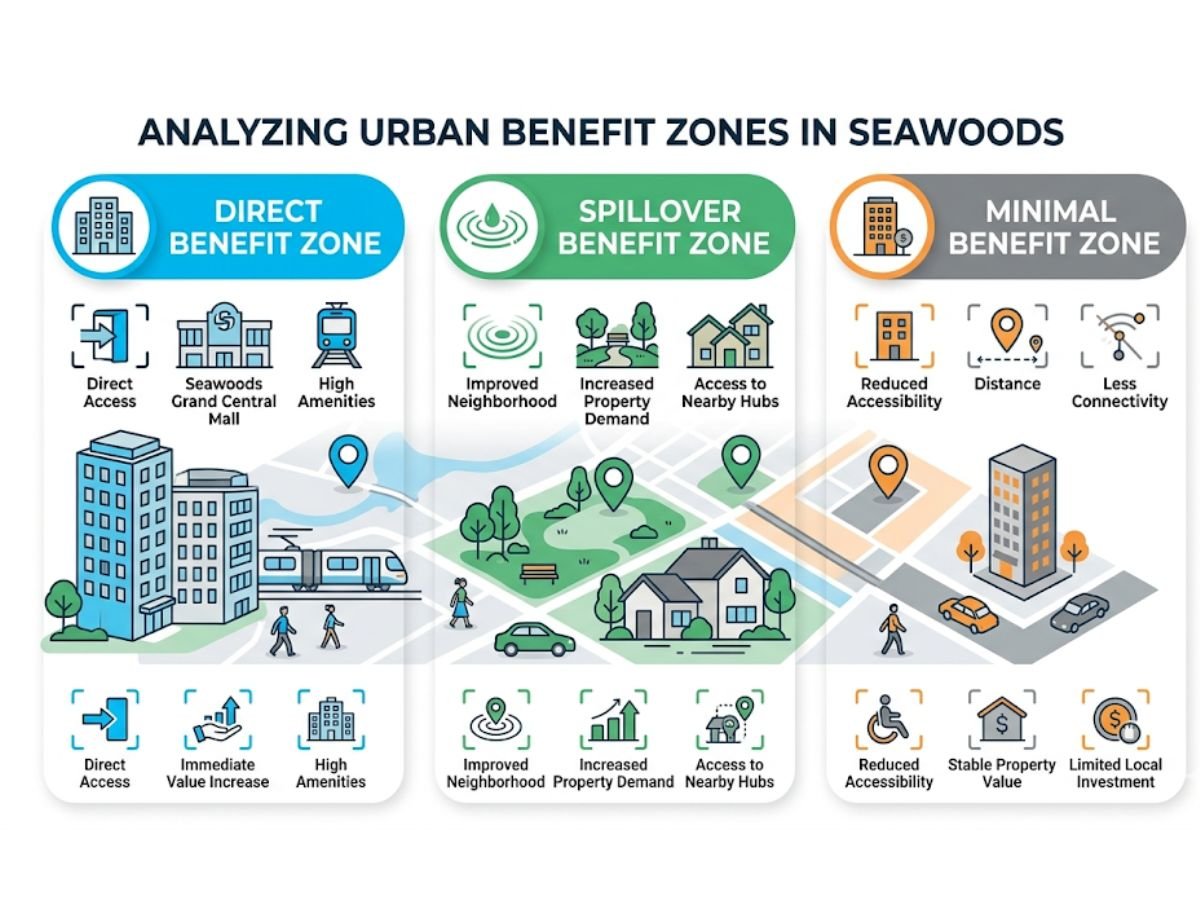

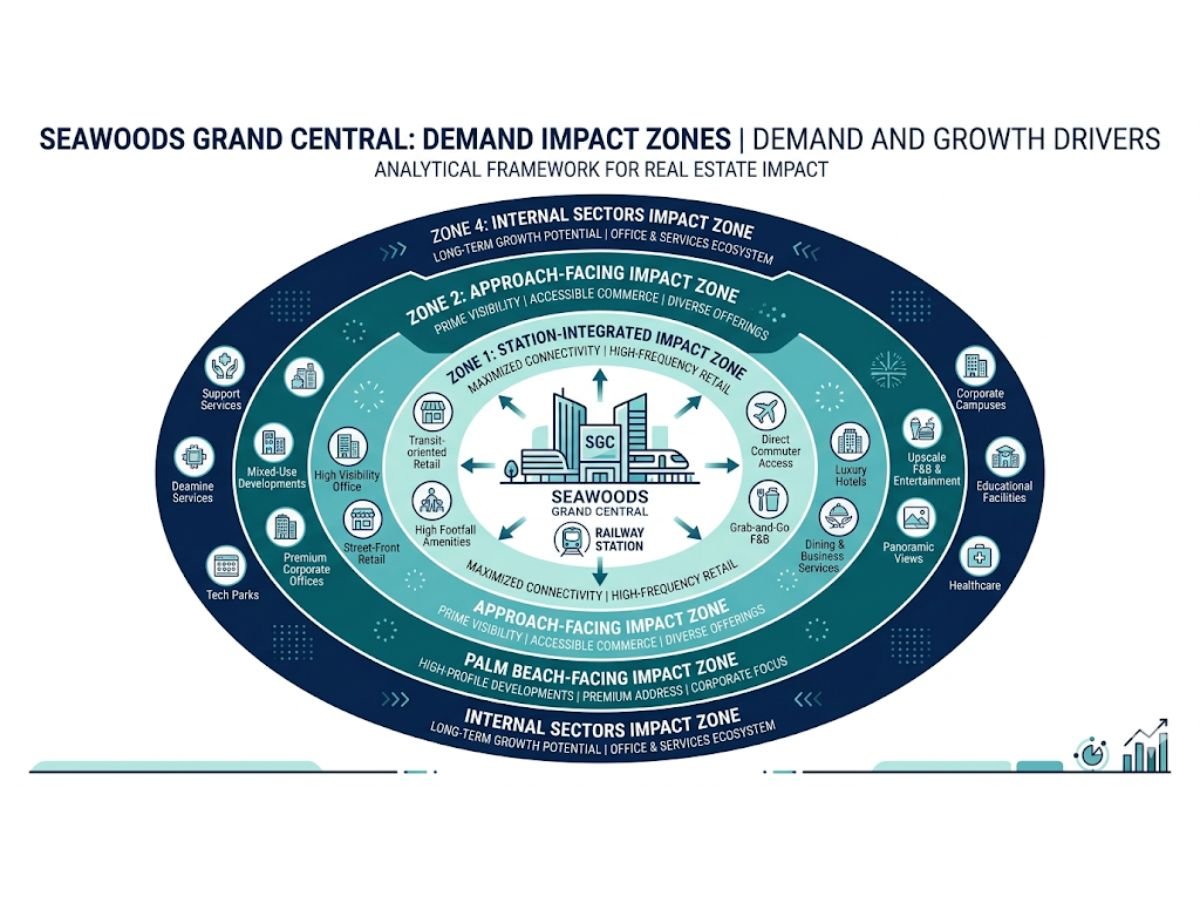

Seawoods Grand Central and Nexus do shape commercial demand in Seawoods, but not in a blanket way. The real demand premium sits in a narrow band where station integration, direct pedestrian movement, premium retail pull, and office access overlap. That means station-integrated and approach-facing properties can command a very different business reality from internal sector stock that merely shares the Seawoods pin code.

This is the biggest mistake buyers, brokers, and even some tenants make in Seawoods. They see a successful landmark and assume the whole node benefits equally. It does not. Nexus Seawoods itself is a strong, consolidated retail asset: the official property page shows 1.0 million sq. ft. leasable area, 98% leasing occupancy, 300+ stores, and about 15 million LTM footfalls as of December 31, 2025. But mall success is not the same as surrounding street success.

L&T’s official Seawoods Grand Central page also matters here because it confirms the bigger structure behind the demand story: this is a 40-acre transit-oriented development integrated with the railway station, combining commercial, retail, residential, and F&B within one ecosystem. That is why Seawoods behaves less like a normal node and more like a tightly concentrated commercial gravity point.

Quick Summary

| Micro-market zone | Main demand driver | What usually works best | Premium reality |

|---|---|---|---|

| Station-integrated ecosystem | Direct rail access, mall capture, landmark value, office ecosystem | Grade A offices, branded retail, strong F&B, destination services | Highest and most justified premium |

| Approach-facing stock near station | Spillover visibility, commuter path, brand association | Cafes, clinics, salons, convenience retail, client-facing offices | Strong premium, but only for the right frontage |

| Palm Beach visible / connector-facing stock | Vehicular visibility, prestige, easier brand recall | Corporate offices, showrooms, destination-led service brands | Selective premium, less about footfall and more about exposure |

| Internal sector stock | Local residential catchment only | Daily-needs retail, neighbourhood services, small clinics | Much lower TOD benefit than sellers claim |

What is Seawoods Grand Central and Nexus really doing to commercial demand in Seawoods?

It is concentrating movement, image, and spending power into one part of Seawoods.

That sounds simple, but the effect is very specific. A normal commercial market grows slowly around roads, residences, and legacy office activity. Seawoods Grand Central changed that pattern by stacking a rail station, large-format retail, food and leisure, and premium office infrastructure into one destination. When a place captures both weekday work movement and weekend consumer movement, it starts setting the pricing ceiling for the whole micro-market. The practical meaning is this: commercial demand in Seawoods is now anchored by one ecosystem, not spread evenly across the whole node. So if a seller says, “This is in Seawoods, therefore it will get Grand Central demand,” that statement is incomplete at best and misleading at worst.

Why this ecosystem acts like a demand engine, not just a mall

Commuter movement and station-linked visibility

Seawoods Grand Central is not only a retail destination. It is integrated with the station, and that matters because rail-linked movement creates repeat daily human flow, not only weekend crowd. L&T itself highlights that the project is integrated with the railway station and connected across the MMR region.

But there is a catch. Commuter demand is fast demand. People on a station route usually buy speed, convenience, and habit. They stop for coffee, grab-and-go food, pharmacy, ATM, utility services, maybe a salon or quick appointment business. They do not automatically support every shop type just because they pass nearby.

Premium retail pull and destination footfall

Nexus Seawoods is already a mature retail magnet, not an empty mall story. The official property page shows 300+ stores, over 280 brands, and about 15 million LTM footfalls. That scale gives Seawoods something older street-led pockets often do not have: a strong regional draw for shopping, entertainment, and leisure.

That helps surrounding property, but only in a narrow way. Premium dining, speciality services, beauty, diagnostics, and select high-street uses can benefit from being close to this ecosystem. On the other hand, a generic independent apparel store outside the project can easily get crushed because the shopper is already captured inside the mall.

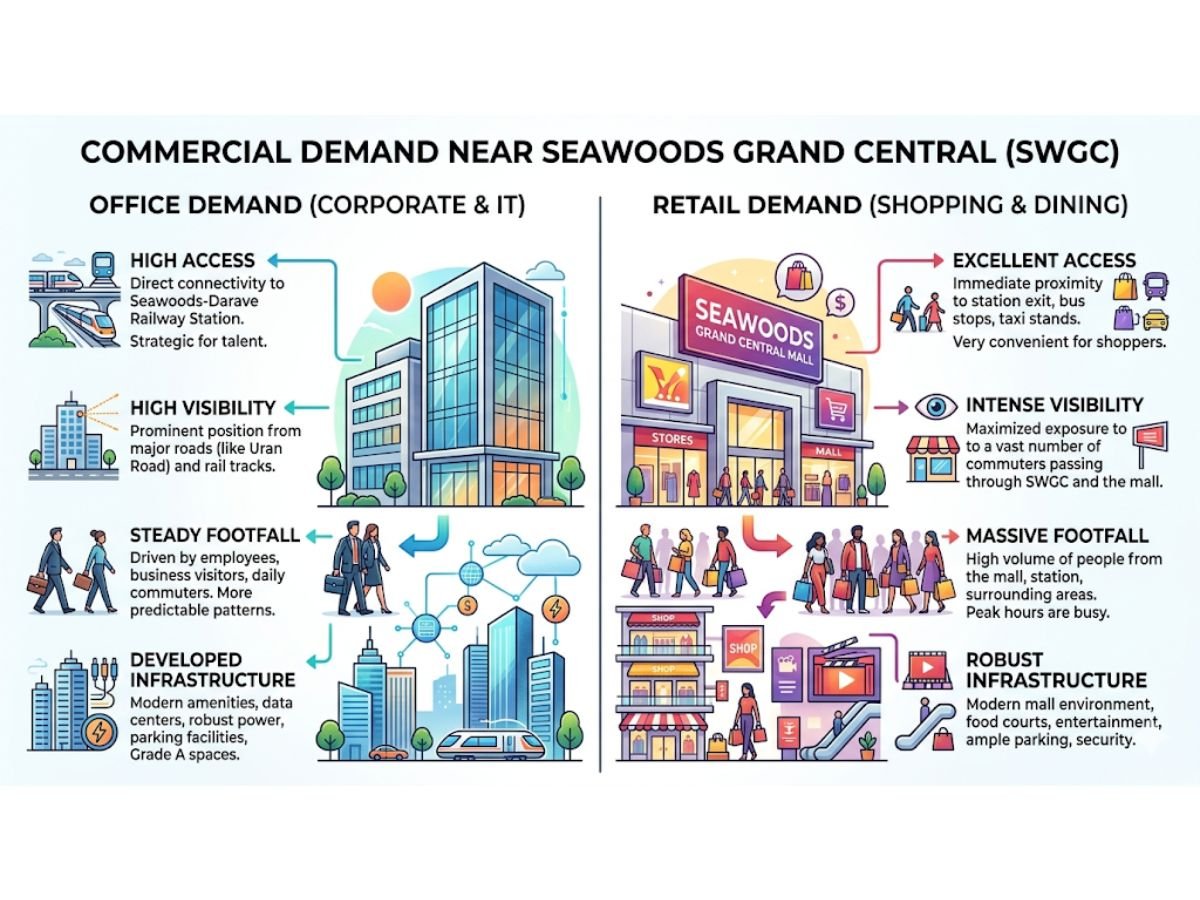

Office-support demand and business ecosystem effect

The third layer is the office effect. L&T markets Seawoods Grand Central as scalable office space with modern systems, LEED Gold certification, 100% power backup, and strong building infrastructure. That is a very different demand engine from retail. Offices do not need impulse footfall in the same way shops do. They need access, image, parking logic, and ease for employees and clients.

This is why a clinic, consultancy, financial services office, or corporate back office can do well in the Seawoods station ecosystem even if it is not sitting on a glamorous retail frontage.

What kinds of commercial demand it actually creates and what it does not create

Seawoods Grand Central and Nexus create layered demand, not one single type of demand.

For branded retail and F&B, the strongest value stays inside the integrated ecosystem or on the most visible outside approaches. The mall already houses the dominant brands, so street retail outside has to win through convenience, speciality, or a very specific service gap. Official Nexus data itself shows how strong the internal retail capture already is.

For offices, co-working, and client-facing businesses, the story is often stronger outside than many people realise. A CA office, architect, dermatologist, diagnostic centre, wealth advisor, legal office, or real estate consultancy can benefit from saying, “opposite Seawoods Grand Central” or “station-integrated Seawoods office.” That address carries practical value because clients know the landmark and can reach it easily.

For local services and convenience-led uses, the best candidates are businesses that match the actual behaviour of commuters, nearby residents, and office users: pharmacy, quick-service food, speciality salon, clinic, courier/utility-type services, and selective small-format food or beverage.

What usually does not get automatic support? Large-format independent fashion, generic electronics, and retail concepts that depend on leisurely outside browsing. The mall already absorbs much of that demand.

Which Seawoods commercial pockets benefit directly, indirectly, or barely at all

This is where the article becomes genuinely useful, because Seawoods is not one flat commercial market.

Station-integrated and directly attached stock

This is the real premium zone. Here the project’s identity, rail access, office environment, and organised retail all come together. Current listing signals also show how different this micro-market is. For example, one 99acres listing for office space in L&T Seawoods Grand Central shows ₹2.04 crore onwards for 1,200 sq. ft., which works out to roughly ₹17,000 per sq. ft. in asking value. Another rent listing shows ₹7.34 lakh for 4,894 sq. ft., roughly ₹150 per sq. ft. per month in asking rent. These are listing-led figures, not final deal values, but they show the premium logic clearly.

Station road and immediate approach belt

This is the strongest spillover zone. If a shop or office faces the natural station approach, catches real pedestrian movement, and stays visible without forcing the customer to detour, it can borrow part of the Grand Central demand. Current 99acres snippets from Sector 42 show how aggressive this band can get: one shop listing appears at about ₹38,596 per sq. ft., while a small showroom listing touches ₹68,000 per sq. ft. in asking price. That does not mean every property there is worth that much. It means the market is trying to price the spillover premium very hard.

Palm Beach visible stock

This pocket works differently. It is less about pure station footfall and more about road visibility, prestige, and brand presentation. Palm Beach-facing or connector-visible commercial property can work well for showrooms, corporate offices, premium service brands, and destination businesses. The pull here is often more vehicular and brand-led than commuter-led.

Internal sectors

This is where many buyers get trapped. Internal sector stock in Seawoods can still work, but usually on residential support demand, not on Grand Central or Nexus demand. If a shop serves societies, schools, routine healthcare, or neighbourhood daily needs, it may be perfectly viable. But it should not be priced or underwritten like station-integrated commercial stock.

> Caution: A Seawoods address is not the same as a Seawoods Grand Central demand profile. A property can be geographically close yet commercially disconnected.

Does Seawoods Grand Central strengthen office demand and retail demand in the same way?

| Factor | Office demand near the ecosystem | Retail demand near the ecosystem |

|---|---|---|

| What drives success | Access, prestige, commute ease, client familiarity, infrastructure | Frontage, pedestrian capture, visibility, impulse or repeat purchase |

| Can upper floors work? | Often yes | Usually weak unless destination-led |

| Is mall success automatically helpful? | Often indirectly yes | Only sometimes, and often not enough |

| Best examples | Clinics, consultancies, finance, legal, back-office, co-working | QSR, cafe, pharmacy, convenience retail, select speciality services |

| Common mistake | Overpaying for image without checking operations | Assuming crowd inside the mall will spill outside |

Who gains most from this ecosystem and who should stay careful

The best fit is usually the serious end-user who can convert accessibility and landmark value into business trust.

A premium clinic, consultancy, diagnostic business, financial services office, legal chamber, or boutique professional office can gain real value here. The address is easy to explain, easy to find, and easier to reach than many older Navi Mumbai commercial pockets.

The second strong fit is the disciplined office investor. If the asset is genuinely station-integrated or in the right office-support zone, the combination of rail access, organised infrastructure, and business address can support stable leasing better than a random commercial floor elsewhere.

The third fit is the selective service or franchise business that matches the human flow around the ecosystem. That means convenience, not fantasy. Coffee, beauty, diagnostics, premium quick service, or specialised services often make more sense than broad “retail” as a category.

The wrong fit is the passive buyer who hears “Seawoods,” hears “Grand Central,” and assumes any internal-sector shop will get premium yield. That is exactly how capital gets stuck.

Two simple local examples

Example 1: the cannibalised retailer A small independent fashion store takes a costly shop outside the main approach because the owner assumes mall crowd will spill over. In reality, fashion shoppers stay inside the organised brand environment, and the outside shop struggles to convert premium rent into stable sales.

Example 2: the symbiotic clinic A dermatology, diagnostics, or consulting office near the station ecosystem does well because clients value landmark recall, easier reach, and perceived quality. It is not competing with the mall’s retail engine. It is using the location differently.

Why some nearby properties are overpriced just because they use the Grand Central or Nexus halo

This is the false halo problem.

A lot of resale and leasing pitches in Seawoods quietly borrow the power of Seawoods Grand Central without actually offering its commercial advantages. The property is described as “close to Nexus” or “Grand Central facing” or “walking from the station,” but once you test the route on ground, the reality is different. The customer path is broken. The frontage is weak. The unit is not on the natural movement line. Parking is awkward. The business type is wrong for the location.

This matters even more because the official project is strong enough to create a real premium. That real premium then gets copied by weaker surrounding stock. Buyers need to separate the two.

If the property is station-integrated, directly on the approach, or highly visible on the connector, premium logic may be real. If it is tucked into an internal lane and only borrowing the landmark name, the premium may be mostly marketing.

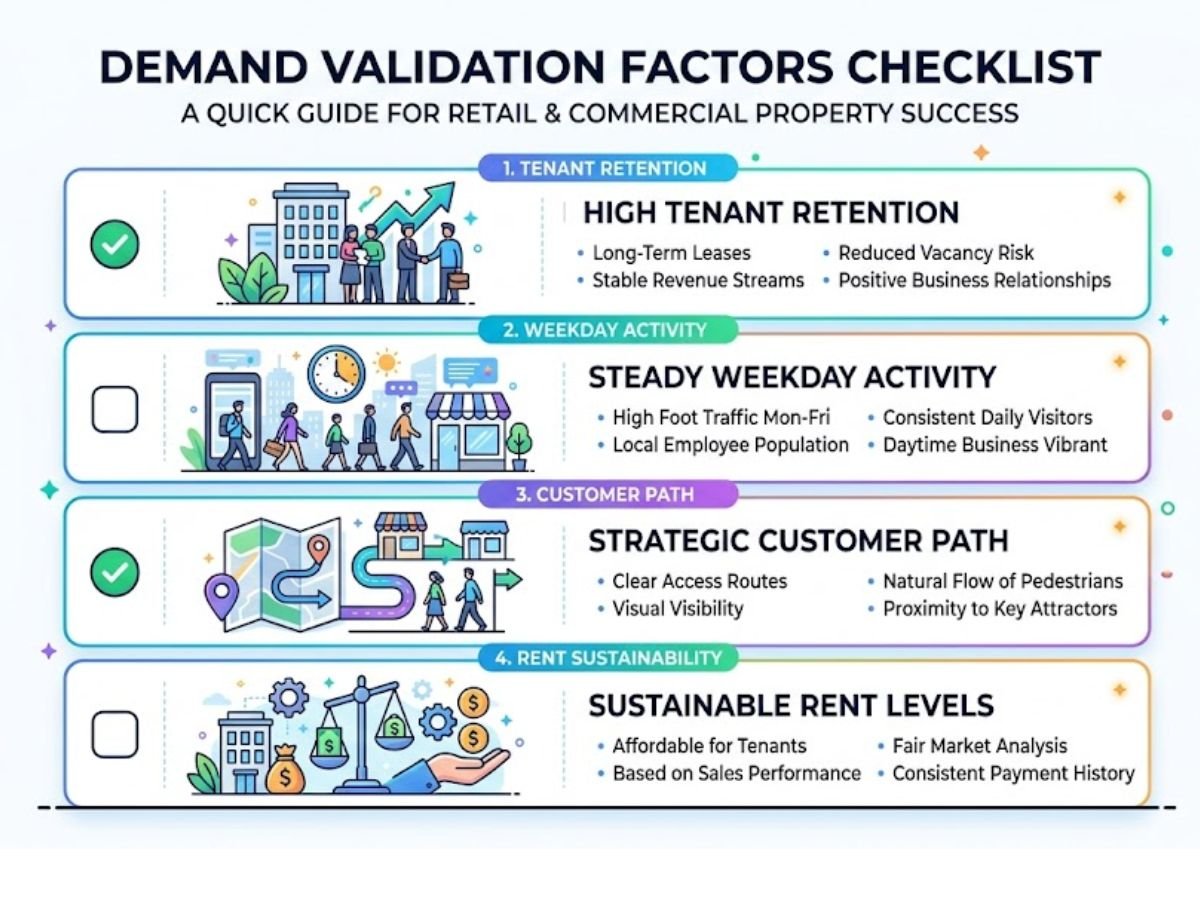

What signals show the demand is real before you pay a premium

Look for proof that the location works on normal weekdays, not only on impressive weekend visuals.

First, check tenant retention. If nearby commercial units keep changing hands or changing tenants too often, the area may be over-rented for actual sales.

Second, check time-of-day strength. A viable pocket near this ecosystem should have some life during weekday office hours, not only Saturday evening buzz.

Third, check whether the customer path is natural. If the shopper, commuter, or client has to leave the obvious route and make effort to find the unit, the location is already weaker than the brochure suggests.

Fourth, separate asking price from usable demand. Listing prices around the Seawoods station ecosystem can look very high, especially in Sector 42 and directly linked stock, but listing ambition is not the same as durable business performance.

What should buyers, tenants, and investors verify before choosing property in this ecosystem

For office users, the first checks are boring but critical: actual access hours, power backup, parking, lift quality, and whether the address works for staff and clients in daily life. L&T’s official office page highlights building systems like power backup, safety, modern lifts, and scalable office spaces, which shows why infrastructure matters so much in this micro-market.

For retail buyers, the real test is not “near station” but frontage, visibility, pedestrian capture, and business category fit. A weak frontage shop can fail even in a strong node.

For investors, the most dangerous mistake is underwriting from gross yield fantasy. Premium markets often come with premium CAM, taxes, fit-out expectations, and vacancy risk if the unit type is wrong. So the correct question is not “What is the broker quoting?” but “What is the net return after friction, and how replaceable is the tenant?”

Conclusion

A lot of it.

Seawoods Grand Central and Nexus have clearly become the commercial centre of gravity for premium Seawoods demand. Officially, the project combines a 40-acre transit-oriented development structure with station integration, organised office infrastructure, and a 1.0 million sq. ft. retail platform that is already heavily occupied and drawing roughly 15 million LTM footfalls. That is enough to reshape pricing, leasing behaviour, and business preference in the surrounding micro-market.

But the benefit is not endless. It fades sharply once the property loses direct access, visibility, or functional connection to the ecosystem. So the right conclusion is not “Seawoods is hot.” The right conclusion is this:

Seawoods Grand Central and Nexus create real commercial demand, but only the right assets in the right strips can convert that demand into sustainable business value.

FAQ's

Frequently Asked Questions