How to Negotiate Industrial Land or Shed Prices in Navi Mumbai

If you want to negotiate industrial land or shed prices in Navi Mumbai properly, do not negotiate only on the quoted rate. The real deal is decided by title quality, leasehold restrictions, transfer cost exposure, BCC status, subletting history, structural condition, usable area, truck access, power readiness, and total acquisition cost. In simple words, the best industrial buyers here do document-first negotiation, not emotion-first bargaining.

That is the first thing to understand. A plot in Turbhe, a legacy shed in Rabale, a unit in Pawane, and a land parcel in Taloja may all be called “industrial property,” but they should not be negotiated in the same way. One can be overpriced because of future-story hype. Another can look cheap but carry lakhs in arrears, repairs, or transfer-related burden.

This is why many buyers make a costly mistake. They focus on what the seller says the property is worth. They do not focus enough on what it will actually cost to own, regularize, upgrade, and use. In Navi Mumbai’s industrial market, that gap matters a lot.

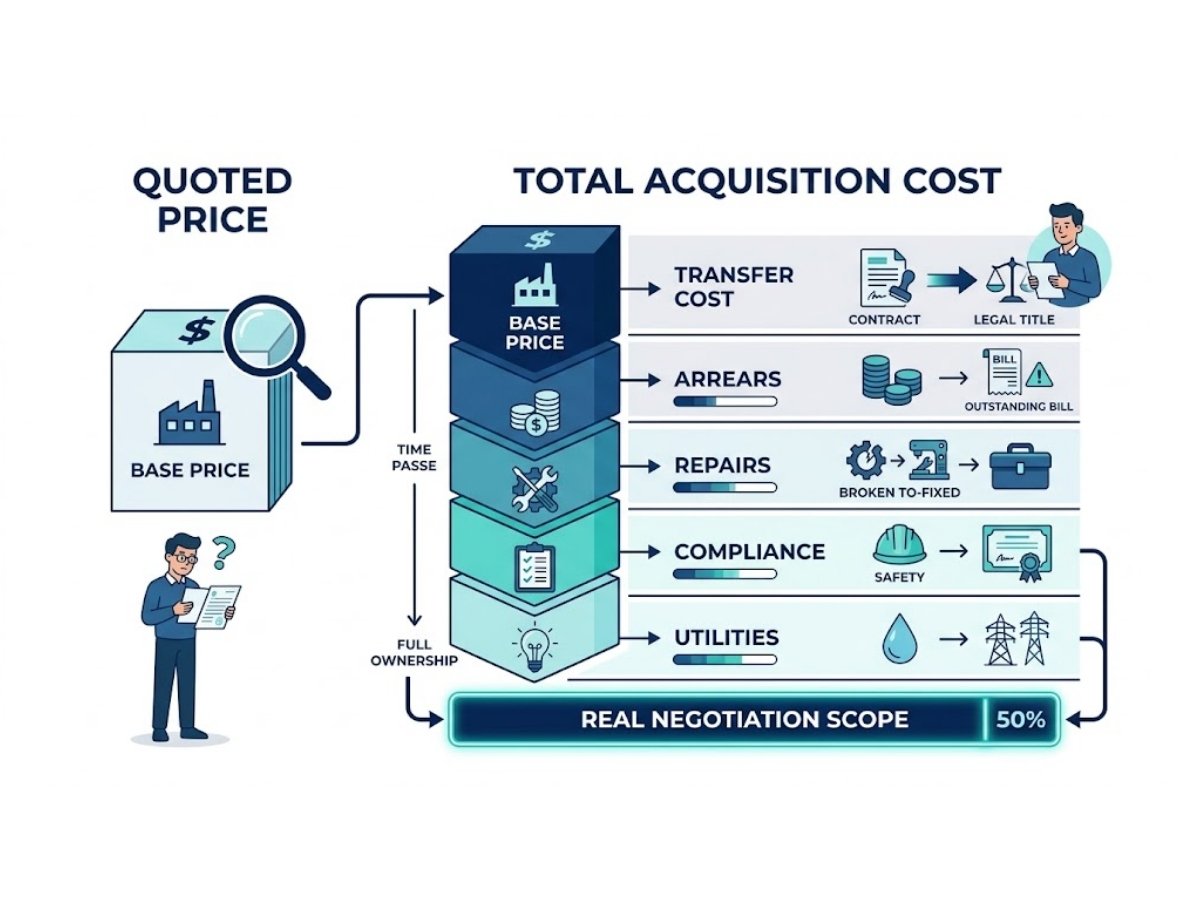

What are you actually negotiating: quoted price, usable value, or full acquisition cost?

You are not just negotiating the seller’s number. You are negotiating the full cost of making that industrial asset safe, transferable, and usable for your real business need.

A professional buyer breaks the deal into parts before discussing price. That changes the conversation from loose bargaining to fact-based adjustment.

Quick summary: what usually affects the real deal cost?

| Price component | Usually quoted openly? | Negotiable or not? | Why it matters |

|---|---|---|---|

| Base land or shed price | Yes | High | This is the main lever, and often includes seller expectation or broker cushion |

| MIDC differential premium | Often hidden or pending | Medium | Can materially change the economics depending on development status and transfer conditions |

| CIDCO transfer-related burden | Often not discussed clearly early | Low on rate, negotiable on allocation | The amount or process may vary, but who bears the burden becomes a negotiation point |

| Stamp duty and registration | Standard | No | Fixed outflow and must be budgeted separately |

| Power and water arrears | Often hidden | High | Must usually be deducted from seller-side settlement logic |

| Structural repair or retrofit | Rarely quoted honestly | High | Old roofs, poor floors, low height, fire compliance gaps can cost lakhs |

| Compliance rectification | Often hidden | High | Missing approvals or certificates reduce value and delay operations |

| Subletting or permission-related issues | Usually hidden | High | Can affect transferability, regularisation, and actual usability |

| Brokerage | Visible late in many deals | Medium | Can often be pushed back on or split differently |

| Utility upgrade cost | Often underestimated | High | Insufficient power, poor water setup, or heavy retrofit can change the real value |

The practical takeaway is simple: asking price is not the same as fair value. In industrial deals, the quoted price is only the opening number.

Industrial land and industrial shed should not be negotiated the same way

This is where many generic articles fail. They talk about “industrial property” as if land and built-up stock are one category. They are not.

Land is usually negotiated on development potential, restrictions, and future cost to make it usable. A shed is negotiated on functional utility, structural life, and retrofit burden.

| Comparison point | Industrial land | Industrial shed or factory unit |

|---|---|---|

| Main value anchor | Location, lease conditions, development timeline | Replacement cost, rental utility, structural usability |

| Main negotiation risk | Transfer restrictions, extension cost, soil or development burden | Low height, weak flooring, roof issues, old utilities, obsolescence |

| Typical buyer mistake | Paying for future story too early | Paying market rate for a structure that needs major capex |

| Best negotiation lever | Idle plot risk, pending development cost, time loss | Repair cost, clearance height, truck movement, power readiness |

| When seller is stronger | Rare well-located clean plot | Operational factory with strong utilities and good access |

| When buyer is stronger | Idle plot with document or development friction | Legacy shed with age-related inefficiency |

When land usually gives more negotiation room

Vacant land in industrial belts often looks attractive because it offers flexibility. But the negotiation becomes stronger for the buyer when the plot has sat idle for years, when development timelines have slipped, or when future use requires significant groundwork.

In practical terms, an idle industrial plot is not always a premium asset. Sometimes it is simply undeveloped land carrying a future burden. That is especially important where the seller is pricing based on scarcity but the buyer still has to absorb time, permissions, soil preparation, and operational delay.

When an old shed looks cheaper but is actually costlier

This is common in legacy belts. A shed may look cheaper than a modern building on a headline rate basis, but once you factor in roofing, floor reinforcement, drainage, fire safety, ventilation, power upgrades, and layout inefficiency, the math changes.

A 12-foot or 15-foot clear-height shed may be acceptable for some small industrial use. But for many modern warehouse, machinery, loading, or racking requirements, that is a functional discount point. So is cracked flooring. So is poor truck turning. So is a weak loading bay arrangement.

When a working factory commands a stronger seller position

If the property is already operating smoothly, has usable power, decent access, acceptable structure, and cleaner paperwork, the seller naturally has more negotiating strength. You may still negotiate, but the discounts will usually come from deal terms, possession structure, fixtures, or speed of closure rather than from a dramatic base-rate cut.

Before discussing price, which 7 checks decide your negotiation power?

Price discussion should start only after a leverage audit. This is where you find the facts that justify your offer.

The 7-check negotiation checklist

- Title quality and leasehold nature

Check whether the property is leasehold, how much lease term is left, and whether the chain of title is clean enough for finance and transfer comfort.

- Transferability and assignment conditions

Some properties look tradable on paper but carry practical transfer friction. That changes the risk and the price.

- Actual usable area versus stated area

Industrial buyers should care about usable ground efficiency, loading space, movement corridors, and internal practicality, not only paper area.

- Truck access and turning practicality

Internal lanes, turning radius, frontage, and entry-exit movement matter far more than a sales pitch about “prime location.”

- Power load and utility strength

A unit with insufficient load or with major upgrade needs can become expensive very quickly.

- Structural condition and retrofit need

Roofing, flooring, drainage, clear height, fire systems, and general wear should be evaluated like cost items, not afterthoughts.

- Approvals, completion trail, and local compliance position

Missing completion-related documents, delayed compliance, or unsettled authority-side requirements often become one of the strongest bargaining levers.

A good negotiation starts when you turn each defect into a cost or risk line item. Without that, the conversation remains emotional. With that, it becomes measurable.

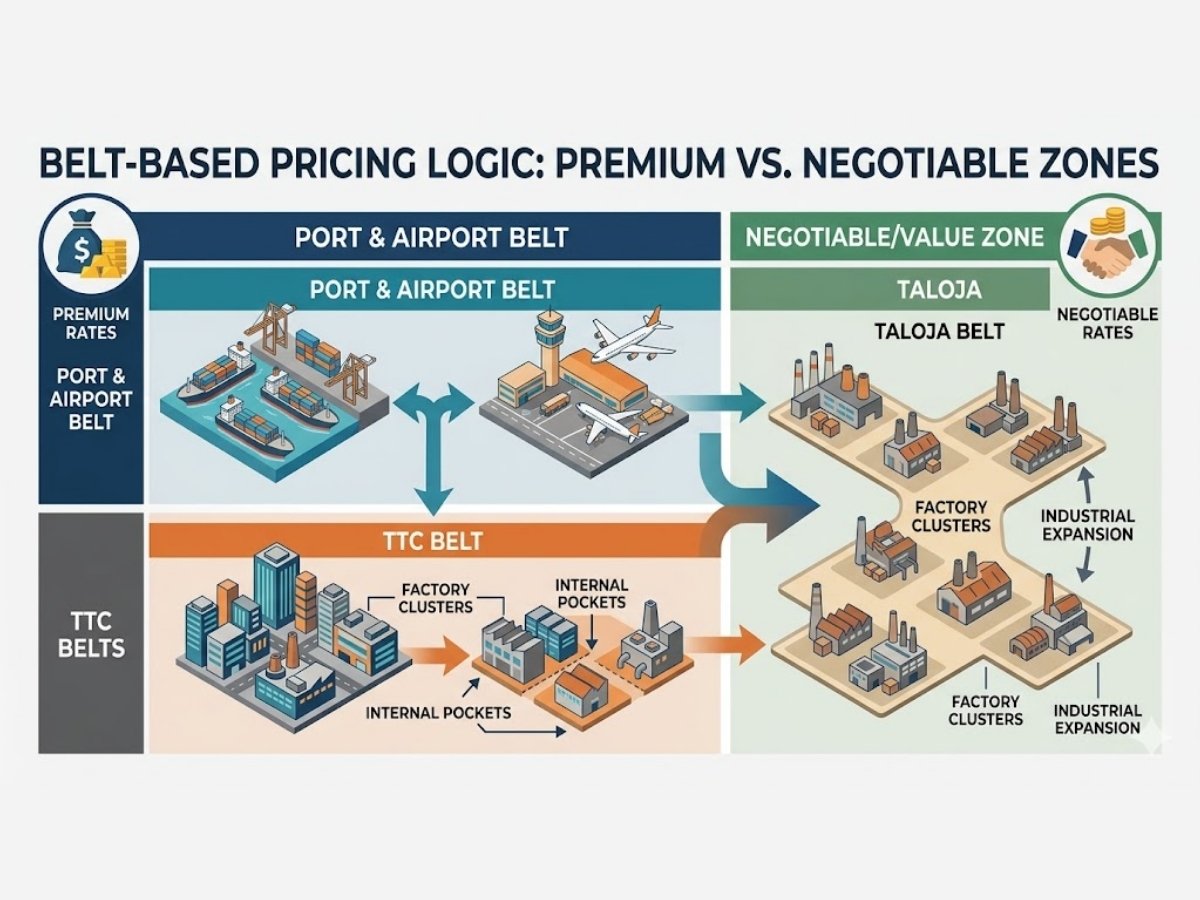

Which Navi Mumbai industrial belts usually deserve a premium and which do not?

Navi Mumbai’s industrial market is not one flat map. Belt logic matters. And this is exactly where weak pages give bad advice.

A quote in Mahape is not automatically comparable to a quote in an internal pocket of Pawane. A rate in Turbhe with strong movement advantage is not equal to an older internal-lane shed with poor trailer handling. A Taloja deal cannot be judged with TTC logic alone.

Area logic that should influence negotiation

| Belt type | Why sellers ask a premium | What buyers should verify before accepting it | Where negotiation room usually opens |

|---|---|---|---|

| Established TTC-style belts such as Turbhe, Rabale, Mahape, Airoli, Pawane | Mature ecosystem, better access, stronger industrial identity, sometimes conversion or redevelopment narrative | Internal road quality, actual access, structure age, utility strength, lane practicality | Older stock, internal lane units, weak functional layout |

| Internal-lane or legacy industrial pockets | Seller may still quote near main-belt rates | Turning radius, loading practicality, frontage weakness, retrofit burden | Usually higher, especially when modern logistics use is compromised |

| Taloja and similar lower-entry industrial stretches | Affordability and growth story | NOC trail, environment-side practicalities, actual operational fit, oversupply pressure | Often better than premium TTC if supply is available |

| Airport-port influence belts such as Ulwe, Dronagiri, Panvel-side influence zones | Future growth, airport, connector, long-term corridor story | Current utility, current cargo practicality, present-day industrial usability | Stronger where seller quote depends too much on future hype |

TTC-style established belts may deserve firmer pricing, but not blindly

The TTC belt remains the most mature industrial cluster in the region. That gives some properties real value. Ecosystem depth, existing industrial activity, labour familiarity, access linkage, and business continuity all matter.

But even inside TTC, not every unit deserves the same rate. Internal-lane stock in Rabale or Pawane with weak trailer movement is not equal to stronger-access stock. Old sheds in Turbhe with layout inefficiency should not be priced like cleaner operational assets.

Internal-lane and older-pocket stock usually gives more negotiation room

This is where buyers often get the best value. Not because the seller is weak by default, but because the property’s functional gap is harder to hide. When the lane is narrow, the frontage is poor, or the truck movement is awkward, the property may still work for some users, but it does not deserve a blanket area premium.

Port-airport influence zones can get overquoted on future story

The airport and major connectors have changed sentiment. That is real. But in negotiation, sentiment is not the same as present-day utility.

If a seller is quoting based mainly on what the belt may become later, bring the conversation back to what the property does today. Can it support the user’s current industrial need? Is cargo movement easy? Is the plot truly ready? Is the price based on actual operational value or only projection? That is a very important distinction.

How should you build your negotiation anchor before making the first offer?

Never start by throwing a random low number. Build an anchor first. A strong anchor is rational, documented, and explainable.

Use local comparable listings carefully, not blindly

Listing portals are useful for spotting asking-price spread, but they are not proof of achieved transaction value. That matters a lot in industrial real estate. Two sheds in the same node may have very different practical worth because one has proper access and another does not. One may be structurally usable; another may be a repair-heavy asset in disguise.

So use market listings as a starting signal, not as your final valuation.

Use ready reckoner as a benchmark, not market truth

The IGR Maharashtra eASR or Ready Reckoner can help you understand valuation floor logic and statutory reference comfort. But it should not be treated as the live market truth for every industrial deal.

In stronger belts, actual market expectations may sit well above it. In weaker or burdened assets, even the seller’s quoted rate above the ready reckoner may still be unjustified. The smart use of ready reckoner is this: it gives you one disciplined anchor, not the full answer.

Discount heavily for legal friction and physical burden

If a seller quotes a strong area rate but the property has access weakness, pending repairs, poor structural efficiency, or unclear transfer-related exposure, your job is not to “argue” emotionally. Your job is to move those defects into price logic.

Example of a rational anchor

Suppose two sheds are quoted at nearly the same rate in a TTC-side belt.

- Shed A has decent entry, acceptable roof condition, functional power, and cleaner document position.

- Shed B has weak internal approach, pending repair burden, unclear transfer-related exposure, and a low clear-height problem.

A generic buyer sees “same area, same rate.” A practical buyer sees “same quote, different value.”

That difference is where negotiation starts.

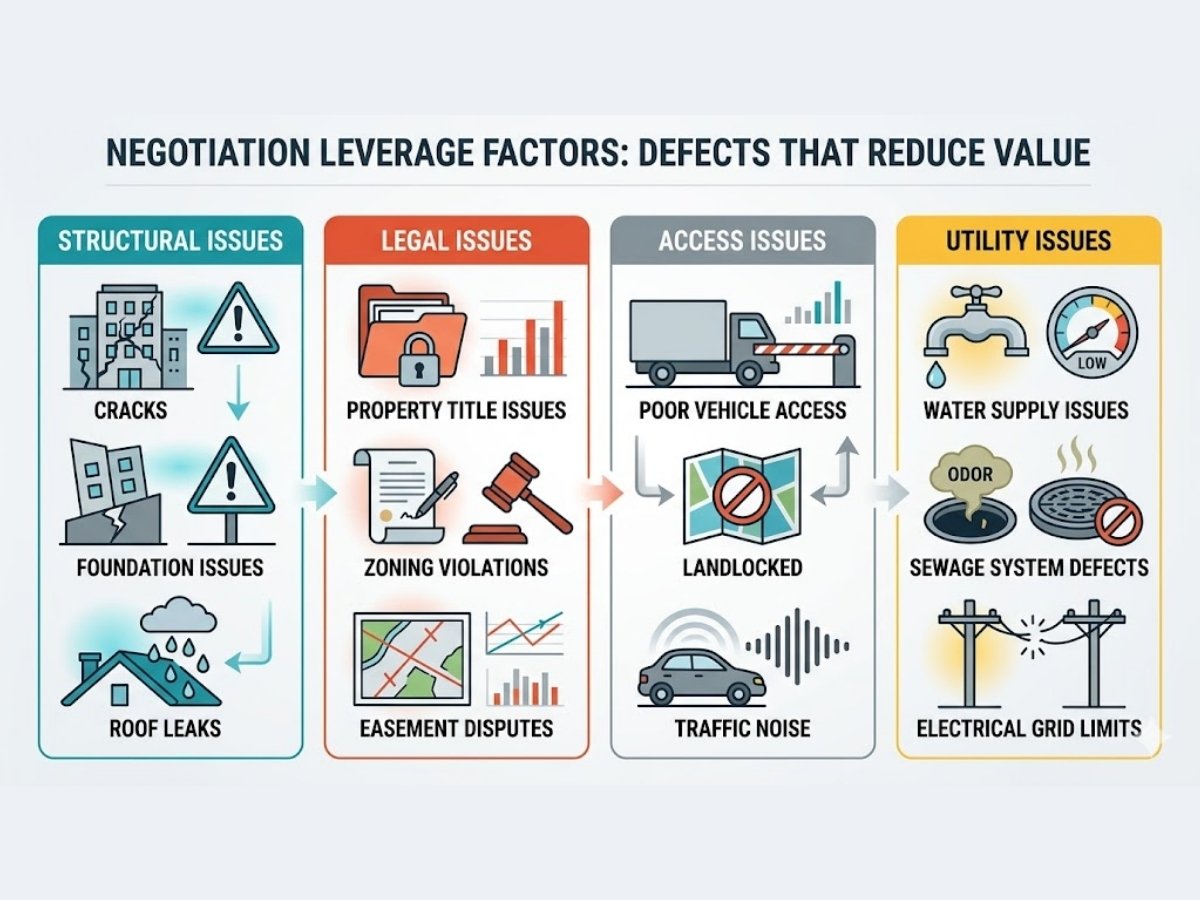

What defects justify a real price cut in Navi Mumbai industrial deals?

Not every issue deserves a dramatic discount. But some defects absolutely change the value. The best way to negotiate is to rank defects by impact.

Negotiation leverage matrix

| Issue | Why buyers should care | Likely impact on value | Negotiation strength |

|---|---|---|---|

| Missing or weak completion-related status | Can trigger extra burden and uncertainty | High | Strong |

| Leasehold transfer friction | Reduces clarity and finance comfort | Medium to high | Strong |

| Subletting complications or unauthorized history | Can create regularisation burden | Medium to high | Strong |

| Weak truck turning or loading practicality | Affects real industrial usability | Medium | Moderate to strong |

| Low clear height or poor shed efficiency | Makes the unit functionally outdated for many uses | High | Strong |

| Roof, drainage, flooring, structural repairs | Immediate capex burden | High | Strong |

| Poor frontage or internal-road weakness | Limits movement and efficiency | Medium | Moderate |

| Power arrears or insufficient utility setup | Direct cost and operational delay | High | Absolute deduction logic |

| Non-comparable location pitch | Seller is using better-area logic for weaker stock | Medium | Moderate |

The key here is simple. Do not say, “Please reduce.” Say, “This issue carries a real cost or real usability loss, so this is the value adjustment.”

How should you negotiate with different types of sellers?

The same offer line does not work with every seller. Industrial negotiation is also about seller psychology.

Direct owner anchored to an old peak price

This seller often values memory more than present utility. They may remember what another property sold for, what the market felt like at its peak, or what someone once told them the land was worth.

With this seller, calm logic works better than aggression. Show why the current structure, access, compliance trail, or market comparability does not support that number.

A useful tone is: “We are not questioning the location or the history of the asset. We are pricing the current condition, current transfer path, and current usable utility.”

Business-exit seller who values speed and certainty

This is often the most practical seller to negotiate with. They care less about “winning the number” and more about closing without drama.

Here, certainty becomes your leverage. A cleaner payment schedule, faster diligence, serious intent, and a milestone-based structure can help secure better economics. Sometimes the seller gives on base price. Sometimes they absorb burden elsewhere.

Broker-led inflated seller

This is very common. The seller quote may already include optimism, negotiation cushion, and future-story inflation. In such cases, the best response is not anger. It is anchoring.

Bring the conversation back to current comparability, current utility, current defects, and actual fit. If the seller is quoting because of airport talk, commercial conversion talk, or highway-adjacent storytelling, ask what the asset is proving today, not what the belt may become later.

What should your first offer look like, and how low is too low?

Your first offer should look reasoned, not reckless. A random low number can shut the conversation. A line-by-line justified offer can keep it alive.

How to avoid insulting the seller

Do not open with a price and no logic. That makes you look unserious. Start with findings first, then your band.

For example:

- access limitation

- roof and floor repair burden

- utility gap

- document-side friction

- comparable weakness versus stronger nearby stock

Then state your number as a result of those deductions, not as a negotiation stunt.

How to justify your offer line by line

A strong industrial offer often sounds like this in plain English:

> “We have priced this as an industrial asset with usable value, but we have deducted for structural retrofit, access limitation, pending utility burden, and transfer-related risk. So our offer is based on actual acquisition cost, not just your headline quote.”

That one framing changes the whole conversation.

Why best-and-final should come after document review

Many buyers rush here. That is a mistake. Your best-and-final number should come only after document review and physical inspection. Otherwise, you may commit to a number before discovering the very things that should have reduced it.

Which costs should you push back on besides the base price?

This is where many buyers leave money on the table. Even if the seller resists on base rate, there are other areas where the deal can improve.

Non-price items that often deserve negotiation

- Pending power or water dues

- Repair or rectification cost

- Demolition or clearing burden

- Utility restoration

- Brokerage allocation

- Possession timeline

- Vacating timeline for occupied premises

- Inclusion of fixtures, cranes, racks, or useful industrial fit-outs

- Allocation of authority-side or permission-related cost where contractually relevant

This is especially important when the base number is sticky. A deal can still become much better if the seller absorbs more of the hidden burden.

When should you stop negotiating and walk away?

Not every industrial property deserves a second round. Walking away is also part of negotiation discipline.

Walk away when these signs appear

- The seller refuses to share basic title papers

- The transfer path is still vague after repeated discussion

- The quote depends mainly on future hype, not present utility

- The property is being compared to stronger pockets that it does not match

- Access weakness or utility weakness is being hidden

- Repair burden is so large that the “cheap” deal stops being cheap

- The seller wants a large commitment before proper diligence is completed

- There is serious pollution, environmental, or legacy compliance risk beyond normal tolerance

A lower price does not automatically make a risky property a good buy. Some assets are cheap for a reason.

A simple industrial negotiation formula buyers can actually use

Most buyers do not need a complicated valuation model. They need a practical decision formula.

Use this simple working formula

Rational purchase range = fair comparable value minus document-risk discount minus access and utility discount minus structural or retrofit cost minus immediate arrears or hidden burden

That is the real logic.

If you want to make it more disciplined, think in this sequence:

1. Start with a realistic comparable value for that exact kind of asset in that exact kind of belt 2. Reduce for title, transfer, or leasehold friction 3. Reduce for physical inefficiency or repair capex 4. Reduce for access, loading, and truck movement limitations 5. Reduce for arrears, compliance, or utility burden 6. Arrive at a negotiation band, not just one heroic number

That last part matters. A band is better than a single number because industrial deals often shift after document confirmation.

Example: negotiating an old industrial shed in a TTC-style belt

Let us take a simple illustrative scenario.

A buyer is shown an old industrial shed in a mature TTC-side location. The seller quotes a strong rate because the belt is established and demand is decent. On the surface, the quote sounds believable.

But during review, the buyer finds:

- the shed has lower clear height than current market preference

- part of the roof needs replacement

- truck movement is not smooth for larger vehicles

- there is utility-side burden that must be clarified

- the stock is being pitched like stronger-access nearby stock even though it is not equally functional

At that point, the negotiation changes.

The buyer should not argue that the area is bad. The buyer should say that this specific asset does not deserve the same valuation as better-functioning comparables. Then the offer should be built around:

- fair belt-level comparable value

- minus structural inefficiency

- minus roof repair burden

- minus movement limitation

- minus any unresolved utility or transfer-side uncertainty

That is how a professional buyer creates price logic. Not by sounding aggressive, but by sounding measurable.

Conclusion

The best way to negotiate industrial land or shed prices in Navi Mumbai is to stop thinking like a normal property buyer and start thinking like an operational buyer. Do not negotiate only on the quote. Negotiate on title clarity, transferability, BCC or completion position, access quality, power readiness, structure condition, and total acquisition burden.

That is the real edge in this market. A seller may quote one number. But your job is to find the number behind that number.

And in industrial real estate, that is where the real savings usually happen.