Industrial Property Mistakes First-Time Investors Make in Navi Mumbai

The biggest mistake first-time investors make in Navi Mumbai is treating industrial property like a simple passive asset. It is not. In most cases, you are buying into a leasehold, authority-driven, compliance-heavy system where the wrong location, wrong asset type, poor approvals, weak access, or hidden transfer costs can damage returns badly. In this market, cheap does not always mean smart, and future growth does not fix a bad industrial asset.

Industrial property in Navi Mumbai can work very well for the right buyer. But beginners usually lose money in very predictable ways. They buy based on brochure pitch, headline rate, or “airport aa raha hai” style excitement without checking what really matters: authority records, development status, operational usability, transfer liability, utility fit, and exit quality.

That is why this guide is not about theory. It is about the mistakes that actually trap first-time buyers in TTC, Taloja, Kalamboli, Dronagiri, and similar industrial belts.

What are the biggest industrial property mistakes first-time investors make in Navi Mumbai?

Here is the short version before we go deeper.

| Mistake | Why it happens | What it can cost | What to check instead |

|---|---|---|---|

| Treating all industrial belts as one market | Buyers hear “Navi Mumbai industrial” and assume same logic everywhere | Wrong area selection, weak tenant demand, poor resale | Match the asset to TTC, Taloja, Kalamboli, or Dronagiri ground reality |

| Buying the wrong asset type | Plot, shed, gala, warehouse, and factory-use unit get mixed up | Vacancies, wrong occupier fit, compliance issues | Check who will actually use the property |

| Buying only by low price | Cheap stock looks attractive on paper | Poor truck access, weak building specs, transfer burden | Visit physically and test operational usability |

| Trusting future growth stories blindly | Airport, port, bridge, metro, and highway stories sound convincing | Dead capital, slow absorption, holding cost pressure | Check present-day demand, not just future buzz |

| Ignoring title and authority-side risk | Buyers think registration alone is enough | Transfer rejection, dues, closure risk, delay | Verify MIDC/CIDCO status, BCC/OC, tax, no-dues, approvals |

| Not checking transferability and financeability | Buyers assume every unit can be sold or financed later | Exit problems and buyer pool shrinkage | Check document cleanliness and formal transfer path |

| Underestimating total cost | Only base price is discussed | Big extra outflow after token | Add stamp duty, cess, transfer premium, repair, utility, legal cost |

| Buying for rent without leasing logic | Yield is imagined, not tested | Vacancy and fit-out burden | Understand who the likely tenant is and what specs they need |

| Ignoring power, water, pollution, and compliance fit | Non-operators miss these details | Useless asset for intended user | Check sanctioned load, water, MPCB fit, fire norms |

| Assuming resale will be easy | Strong location name creates false confidence | Long listing period, discount exit | Check usability, age, title, layout, demand depth |

Mistake 1: Treating all industrial property in Navi Mumbai as one market

This is the first and biggest strategic error. Navi Mumbai industrial property is not one uniform market. TTC, Taloja, Kalamboli, and Dronagiri do not behave the same way, and a beginner who buys with a city-level mindset usually overpays or buys the wrong kind of risk.

Why TTC, Taloja, Kalamboli, and Dronagiri behave differently

TTC is the older, more mature belt. It benefits from better Mumbai-side access and a stronger urban-industrial ecosystem, but older stock, tighter internal movement, redevelopment complexity, and higher tax exposure can make a “premium” purchase look better than it really is.

Taloja is more manufacturing-oriented. It can suit serious industrial users, including heavier categories in the right sectors, but that also means utility, pollution, and effluent-related checks matter far more.

Kalamboli is often read through a logistics lens. That can be correct, but only in the right pockets. A warehouse without proper road logic is not automatically a good logistics asset just because it sits in the Kalamboli side.

Dronagiri is the future-story market in many conversations. Port adjacency and airport narratives create interest, but present-day labor ecosystem, support infrastructure, and actual occupier depth still matter.

Why the same budget can buy very different risk profiles

A first-time investor may compare two similarly priced units and think they are comparable. They are not. One may be in a mature but technically outdated pocket. Another may be in a growth corridor with lower current usability. The price may look similar, but the risk is completely different.

That is why area logic must come before rate discussion. In industrial property, the wrong micro-location can destroy leasing, operations, and resale even if the headline rate looked attractive.

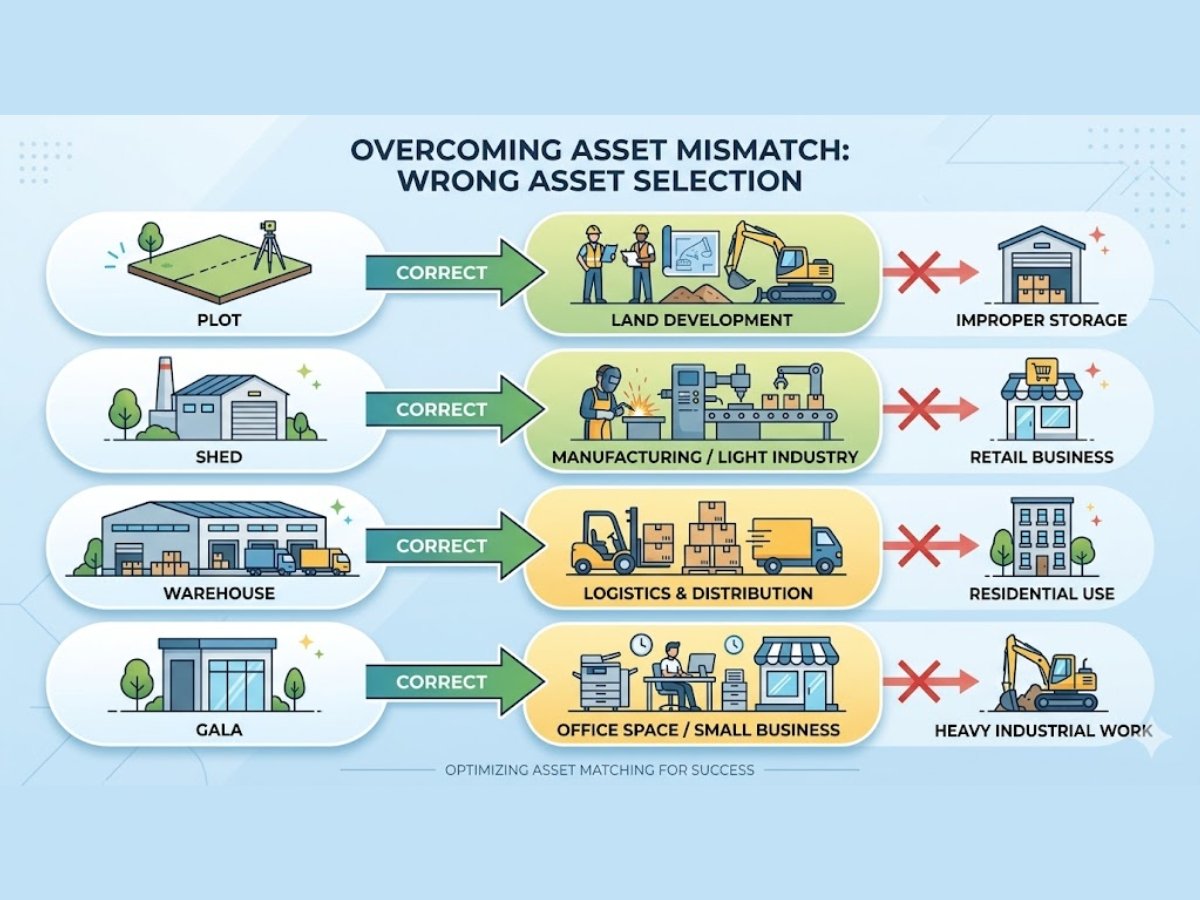

Mistake 2: Buying the wrong asset type for the actual demand

Many beginners say they want to “invest in industrial property” without being clear whether they mean a plot, a shed, a gala, a warehouse, or a manufacturing-ready unit. That confusion leads to wrong buying.

Where beginners confuse plot, shed, warehouse, and factory-use property

A plot is not the same as a ready unit. A small industrial gala is not the same as a logistics warehouse. A warehouse is not automatically suitable for manufacturing. A shed may look large, but if the structure, power, or layout is weak, the actual demand may be narrow.

The right question is simple: who will use this asset, and for what exact purpose?

If the answer is vague, the purchase is already on weak ground.

Why leasing demand changes by asset type

Industrial tenants do not rent only on square footage. They care about height, floor loading, truck movement, loading bays, sanctioned power, water availability, and compliance fit. Modern logistics users think in cubic volume, not just carpet area. Manufacturing users may care more about floor strength, effluent handling, and power infrastructure.

So the same investor who buys a low-height older structure hoping for premium warehouse rent may discover that the real tenant pool is much smaller than expected.

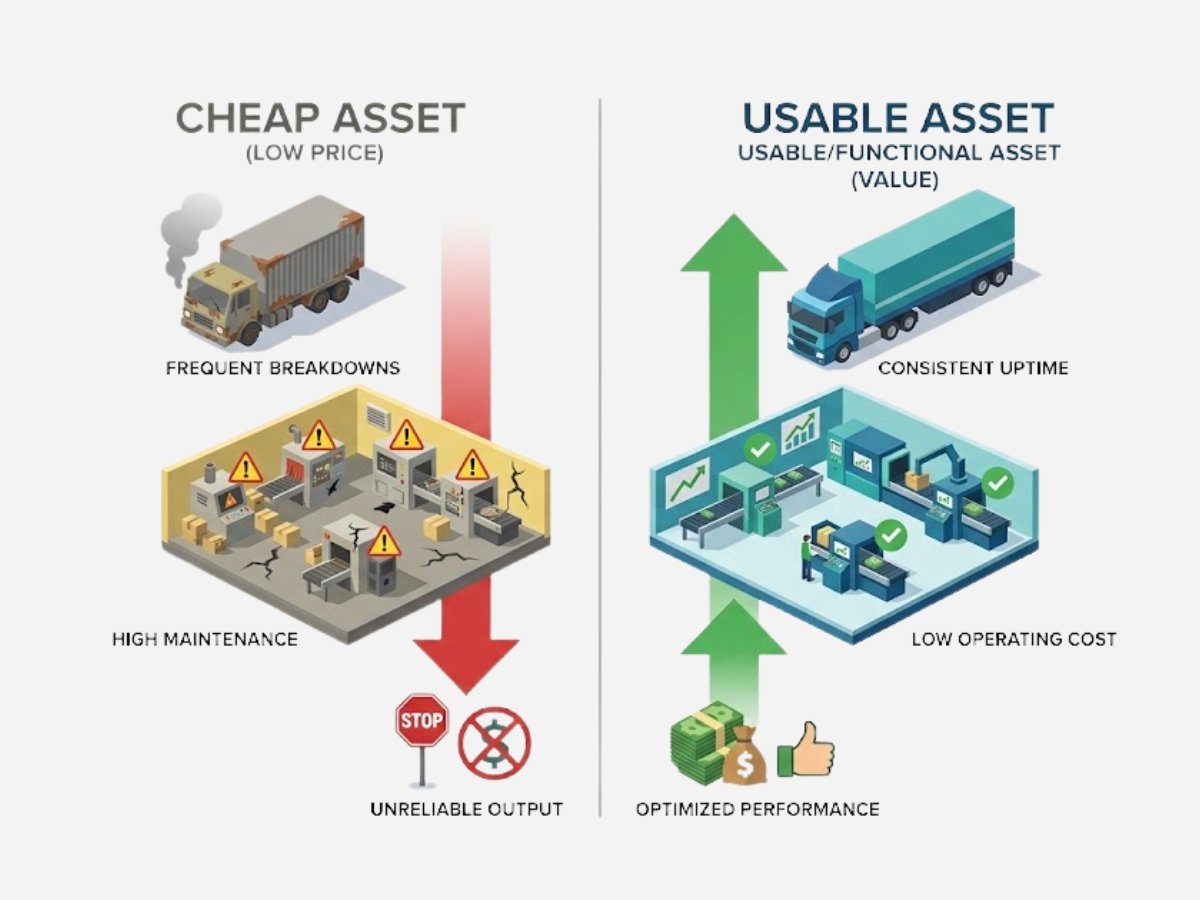

Mistake 3: Choosing only by low price and ignoring operational usability

This is where first-time industrial investors often make a “cheap deal” that becomes expensive later. A low rate can hide operational weakness.

Truck movement, turning radius, loading, internal roads, and access reality

Industrial property is not judged only from the gate. It is judged by whether the target user can operate smoothly. Can a larger vehicle enter? Can it turn properly? Is there enough apron depth? Are internal roads practical? Is loading easy or constantly compromised?

In many older industrial pockets, these details are the difference between a leaseable and a frustrating asset.

Why a cheaper unit can become harder to use, lease, or sell

A buyer saves on entry price but later struggles with user fit. Then comes the usual cycle: fewer tenants, harder negotiations, upgrade cost, longer vacancy, and weaker resale.

That is why “cheap” should never be read as “undervalued” automatically. Sometimes it is simply cheap because the asset is operationally weaker.

Mistake 4: Believing future growth stories without checking present-day ground reality

Future growth matters in Navi Mumbai. Nobody sensible ignores infrastructure. But first-time investors often go too far and buy only the story.

Infrastructure buzz vs current usability

Airport, port, metro, bridge, and connector road stories can influence long-term demand. That is true. But an industrial investor still needs current logic. Can the asset get the right occupier now or in the near term? Does the local ecosystem support real use? Is the area ready enough for business operations?

A future-led story cannot rescue a weak present-day asset.

When “coming soon” areas suit speculation more than stable investment

Some belts suit long-term, patient, higher-risk investors better than first-time buyers who need clearer absorption, better tenantability, and lower uncertainty. Dronagiri is a good example of where future narrative can become stronger than present operating reality in buyer conversations.

There is nothing wrong with future-led investment. The mistake is not knowing you are doing future-led investment.

Mistake 5: Ignoring title, approvals, and authority-side risk

This is one of the most dangerous mistakes in the Navi Mumbai industrial market. Many buyers behave as if registration alone solves ownership. It does not.

In most industrial transactions here, you are stepping into a leasehold structure with authority conditions, development obligations, transfer rules, and no-dues requirements. This is not the same as buying a freehold residential flat and moving on.

Where CIDCO, MIDC, local authority, and project-document issues can matter

Different nodes behave under different authority frameworks. In TTC and Taloja, MIDC has a central role in land and planning matters. In Kalamboli and Dronagiri, CIDCO-side logic becomes more relevant. Civic tax and local body responsibilities can also involve NMMC or PMC depending on the area.

The practical point is this: one authority’s paper does not automatically solve another authority’s issue.

A buyer may see clear MIDC-side records but later discover municipal tax arrears, water dues, approval mismatch, or compliance gaps. This is why industrial due diligence must be authority-layered, not single-document based.

Why first-time buyers should not rely on verbal assurances

Industrial deals are full of verbal comfort lines. “Transfer ho jayega.” “Ye sab regular hai.” “Power upgrade simple hai.” “Old owner ka issue close ho jayega.” These lines mean nothing without document support.

A beginner should especially verify:

- Leasehold status and remaining term

- BCC or OC status, wherever applicable

- Water no-dues

- Property tax status

- Whether the current physical structure matches approved records

- Whether the intended use is actually allowed

Mistake 6: Not checking whether the property is actually financeable and transferable

A strong industrial asset is not just one that can be bought. It must also be transferable later in a practical way.

Why loanability, transferability, and document cleanliness affect real value

Many first-time investors focus on current negotiation but ignore exit mechanics. Later, when they try to sell, the buyer’s lawyer, financer, or authority review becomes the real test.

If paperwork is weak, building records are mismatched, dues are pending, or transfer route is complicated, the future buyer pool shrinks.

Why exit becomes painful when paperwork is weak

Industrial resale risk is real in Navi Mumbai because the next buyer is usually more cautious than the first one. Any gap in transfer premium liability, shareholding-trigger problem, BCC absence, or authority-side record mismatch can reduce liquidity sharply.

An asset that looks profitable on Excel can become sticky in the market when formal transfer becomes expensive or uncertain.

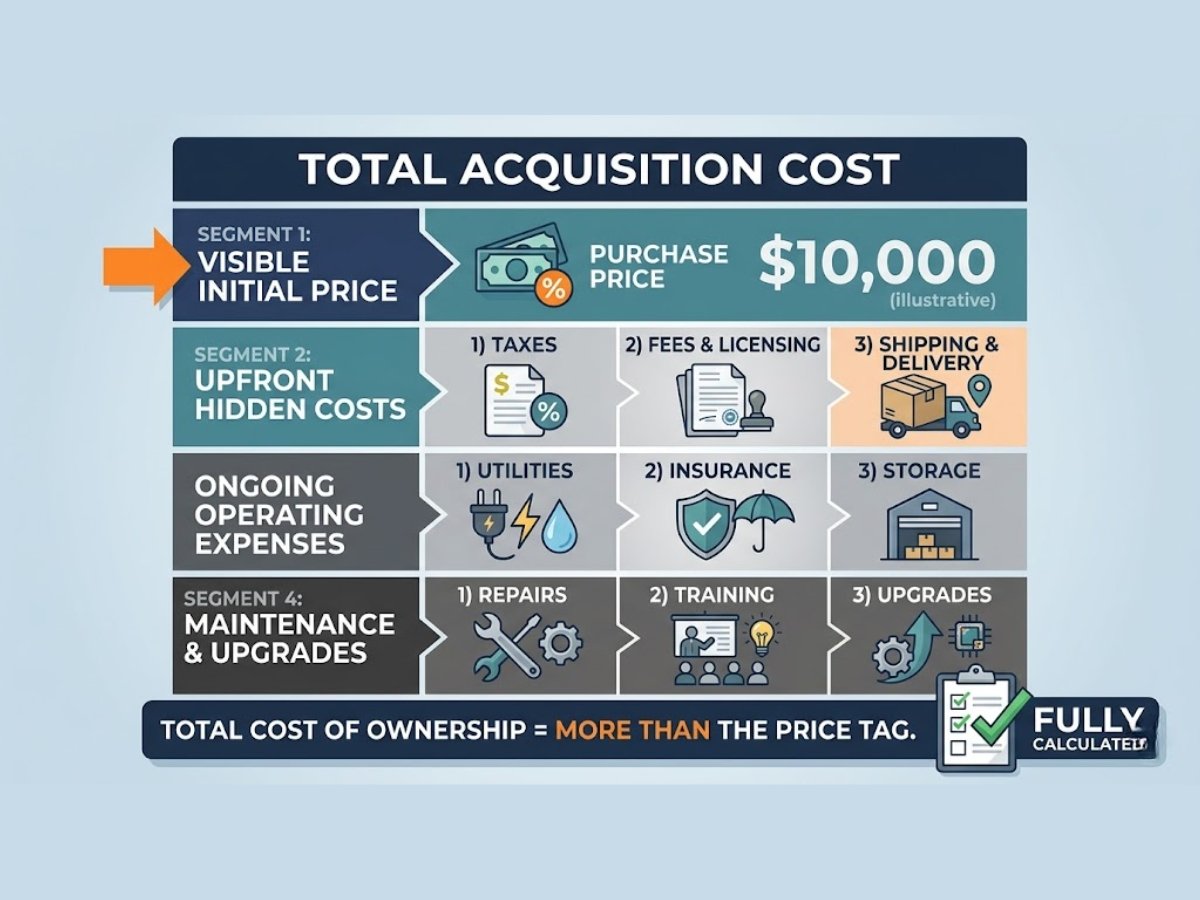

Mistake 7: Underestimating the full cost beyond the quoted rate

This is where many first-time investors get financial shock. They calculate only purchase price and forget the industrial layer of extra cost.

Base price vs total acquisition cost

In an industrial deal, the quoted rate is only the beginning. Actual acquisition cost can also include:

- Stamp duty and registration

- Local cesses and related registration-side additions

- Legal due diligence cost

- Differential premium or transfer premium liability

- Old dues

- Repair and fit-out

- Utility upgrade cost

- Fire and compliance correction cost

Fit-out, repair, compliance, utility, and transaction cost traps

One of the biggest hidden traps is the differential premium structure in authority transfers. If a plot or unit has weak development status or insufficient FSI consumption, the premium burden can be far higher than beginners expect.

The classic trap is a buyer who thinks he found a “cheap industrial plot” but later learns that formal transfer recognition itself may require a very heavy additional outflow. In some cases, the difference between a properly completed asset and an under-compliant asset can run into tens of lakhs.

That is why “What is the total landed cost after all authority-side and operational corrections?” is a far more intelligent question than “What is the last rate?”

Mistake 8: Buying for rental income without understanding tenant quality and leasing friction

Industrial rent is not like residential rent. A tenant does not come just because the area is known.

Occupier demand is not equal across every industrial belt

Demand depends on what the property allows. A warehouse user, a light engineering unit, a chemical operator, a logistics occupier, and a storage tenant all need different things. Even within a strong belt, not every unit is equally rent-worthy.

Why vacancy, fit-out cost, and user mismatch hurt returns

A beginner sees projected rent, calculates yield, and feels comfortable. But if the property needs heavy correction, if only a narrow tenant category can use it, or if the tenant must spend too much to make it workable, vacancy stretches.

A legacy unit in an older belt may appear attractive by rate but stay empty while a technically better asset in a better-fitting pocket performs more smoothly.

Mistake 9: Ignoring power, water, compliance, and use-case fit

This is where non-operator investors often get surprised. Industrial property is not just about owning space. It is about whether the space can actually function for the target activity.

Why utilities and approvals matter more in industrial property than in regular real estate

Power requirement can vary massively between warehousing and manufacturing. Water dependence also changes by use. Pollution category matters. Fire compliance matters. In some sectors, MPCB-related fit is not a side issue. It is the entire business viability issue.

A unit with weak sanctioned load may not suit the intended machinery. A property in the wrong category setting may never become genuinely usable for the target industry.

When a property looks investable but fails operationally

This happens more often than beginners think. On paper, the size looks right. The price looks fair. The belt sounds strong. But the asset fails when real operational questions begin:

- Is power enough?

- Is water secure?

- Is the road width right for the target truck movement?

- Does the building support intended loading?

- Can the target user legally operate here?

If the answer to these questions is weak, the investment is weak.

Mistake 10: Thinking resale will be easy just because the location sounds strong

A known industrial location helps, but location name alone does not guarantee liquidity.

Exit depends on usability, title cleanliness, age, layout, and buyer pool

A buyer exiting an industrial asset is selling more than land or built-up area. He is selling a problem-solving package. If the package is weak, the market discounts it.

Older structures, awkward layouts, title uncertainty, transfer premium burden, low utility fit, and poor road movement can all slow resale badly.

Why some industrial assets stay listed for long periods

Because the next buyer is doing harder math. He is not buying a dream. He is buying usage, transferability, and risk. If those do not work, the asset can remain in the market for months even in a known belt.

Which first-time investor mistakes are most common in each Navi Mumbai industrial belt?

This is where local understanding matters.

| Belt | Common beginner mistake | What usually gets missed |

|---|---|---|

| TTC belt | Paying premium for aging stock just because location is strong | Lease balance, tax burden, old structure limits, tight movement, redevelopment complexity |

| Taloja | Assuming all industrial demand here is equally safe | Pollution category, CETP logic where relevant, utility fit, exact sector quality |

| Kalamboli | Buying into “logistics” without testing the exact pocket | Road access, truck movement, actual warehouse suitability, not just map logic |

| Dronagiri | Buying too early only on future narrative | Present ecosystem depth, labor practicality, current absorption, holding patience |

TTC suits some buyers very well, but not all. Taloja can be strong for the right industrial use, but casual investors often underestimate compliance. Kalamboli works only when the transport logic is real, not assumed. Dronagiri can reward patience, but first-time investors should be honest if they are buying a long-term story rather than a stable present asset.

A practical checklist first-time industrial investors in Navi Mumbai should follow before paying token

Before any token, first-time buyers should slow down and verify at least these points:

- Check whether the property is under MIDC or CIDCO and understand the authority framework properly

- Confirm whether the land or unit is leasehold and how much lease period remains

- Verify BCC or OC status and whether the current structure matches approved records

- Ask clearly whether transfer premium or differential premium liability may arise

- Check water no-dues and other utility-side dues

- Check property tax status with the relevant local body where applicable

- Verify sanctioned power load against intended use

- Check whether the target use is allowed from a pollution and regulatory point of view

- Physically inspect road width, truck turning, apron depth, loading practicality, and internal movement

- Verify whether the asset is genuinely leaseable to the target user class

- Check whether there are labor, accident, or statutory liability risks from the previous occupant

- If under construction, verify MahaRERA status where applicable

- Get a lawyer’s title and document review before commitment

- Do not depend on broker comfort lines for technical or authority matters

- Use a strict 72-hour discipline: authority check first, physical visit next, legal verification before token confirmation

When does industrial property in Navi Mumbai make sense for a first-time investor and when does it not?

Industrial property makes sense for a first-time investor when the buyer is disciplined, patient, document-focused, and clear about use case. It suits people who understand that industrial real estate is not passive residential investing with bigger numbers. It is an active asset class tied to approvals, utilities, access, and transfer rules.

It usually makes sense when:

- The asset type matches real occupier demand

- The authority position is clear

- Transfer and dues risk are understood

- Operational usability is strong

- The investor has budget beyond just purchase price

- The holding strategy is realistic

It usually does not make sense when:

- The investor is buying only because of FOMO

- The deal is driven by rate, not usability

- Future growth story is doing all the work

- The buyer cannot absorb surprise cost

- Compliance and legal review are being treated casually

- The expected tenant or future buyer has not been defined properly

Conclusion

The real mistake first-time investors make in Navi Mumbai is not just buying the wrong property. It is buying with the wrong mindset. Industrial property here is not a simple ownership story. It is a leasehold, compliance, usability, and transfer story.

That is why the safest beginner move is not chasing the cheapest rate or the loudest future pitch. It is buying only after four things are clear: the asset fits real industrial demand, the authority-side documents are clean enough, the operational usability is proven on site, and the future exit will not depend on hope alone.

If those four things are strong, industrial property in Navi Mumbai can be a smart long-term move. If they are weak, even a famous location can become a costly lesson.