How JNPA, NMIA and Freight Corridors Affect Industrial Property Prices in Navi Mumbai

JNPA, NMIA and freight corridors do affect industrial property prices in and around Navi Mumbai, but not in one flat, city-wide way. JNPA creates the strongest premium where port-linked cargo movement is real. NMIA helps assets suited to air cargo, fast distribution and clean logistics. Freight corridors strengthen inland distribution belts that can move goods efficiently. The premium becomes real only when access, sanctioned use, truck movement, utilities and occupier demand actually support the property.

In one answer, how do JNPA, NMIA and freight corridors affect industrial property prices in Navi Mumbai?

| Infrastructure Engine | Core Impact | Best-Fit Assets | Priority Belts | Pricing & Risks |

|---|---|---|---|---|

| JNPA (Port) | Heavy logistics & container movement | CFS Land, Container-linked sheds | Uran, Dronagiri, JNPT Road belts | Land repricing first Risk: No true drayage advantage |

| NMIA (Airport) | Time-sensitive & clean cargo | Grade-A, Cold Chain, Pharma, E-com | Ulwe influence, Airport logistics pockets | Faster asking-rate rise Risk: "Airport Halo" hype vs quality |

| Freight Corridors | Multimodal inland distribution | Large campuses, Road-Rail linked land | Kalamboli, Panvel, Strategic truck nodes | Institutional rent support Risk: Last-mile bottlenecks |

JNPA raises prices fastest where port dependence is real, not where a seller just says “near port”

JNPA remains the biggest hard logistics anchor in this entire story. If the occupier depends on heavy container movement, import-export handling, faster terminal access and lower drayage costs, port-linked land becomes strategically valuable.

That is why the strongest JNPA effect is not emotional. It is operational.

JNPA reported record throughput in FY 2025-26, crossing 102 MT and over 8.17 million TEUs. That matters because it confirms that the port story is not brochure language. Cargo is moving at scale. When that happens, the market starts rewarding land and built stock that reduce logistics friction.

Which asset types usually feel JNPA-led demand first

Port-driven pricing usually shows up first in assets that can genuinely support freight operations. This includes large open plots, container-linked logistics yards, heavy-duty warehouses, compliant storage facilities and land parcels where truck turning, approach roads and loading movement are practical.

It does not automatically show up in every small industrial gala or random interior parcel in Raigad district.

A buyer should be careful here. A cheap plot can sound attractive because it is “JNPA side,” but if trailer movement is weak, if the route adds costly drayage, or if the land use is not clean for logistics, the port premium becomes mostly narrative.

Which belts are most logically port-linked in the Navi Mumbai-Raigad side market

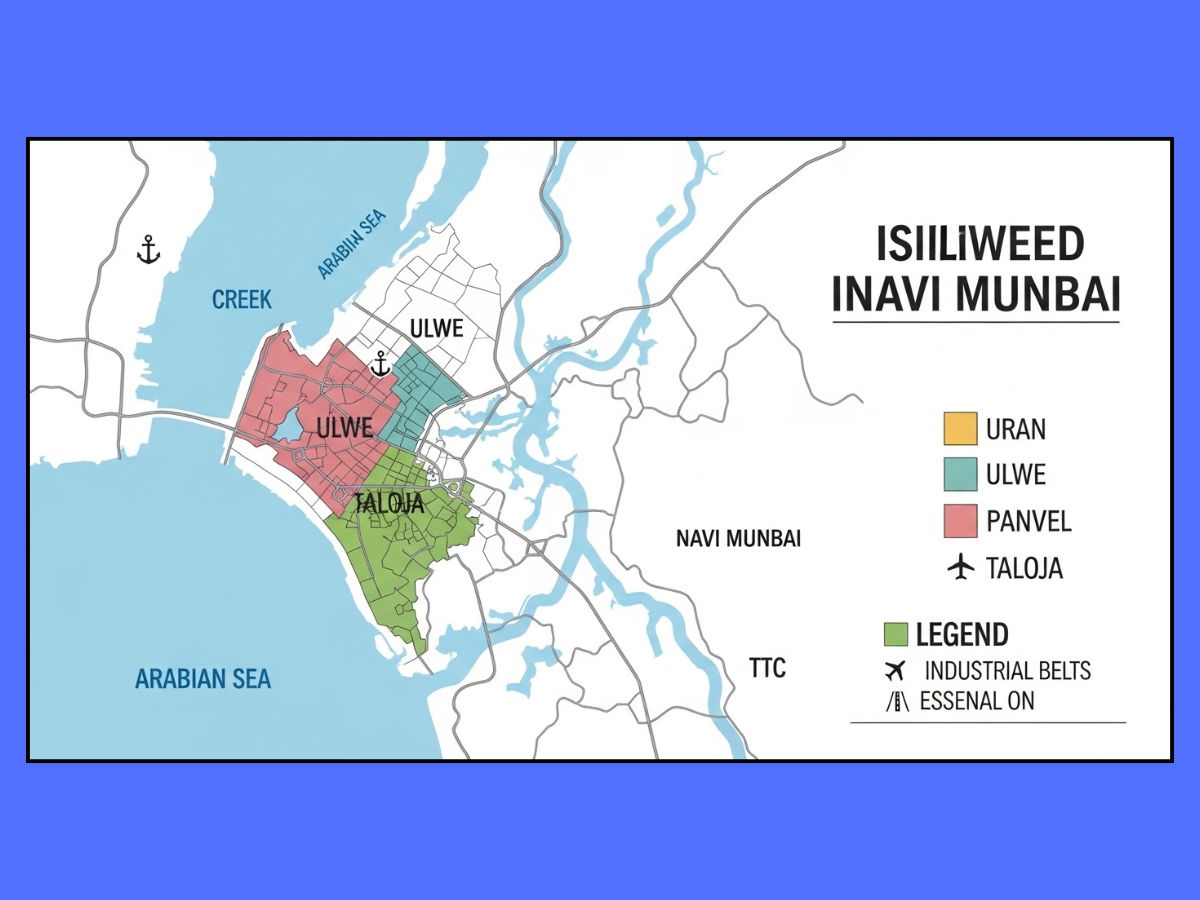

In practical market terms, Uran, Dronagiri and immediate JNPT-linked corridors are the clearest port-edge belts. These are the places where the JNPA logic is strongest because the occupier benefit is direct, not theoretical.

This is also where the market can become dangerous for uninformed investors. In Uran and Dronagiri, pricing variation is extremely wide because sanctioned use, CRZ context, road approach, parcel quality and title clarity change the answer completely. A plot may be geographically close and still be commercially weak.

A useful local test is simple: would a serious EXIM user save meaningful time and transport cost by operating here, or is the property merely using the JNPA name as a sales hook? If the answer is the second one, the premium should be discounted.

One important clue is JNPA SEZ pricing itself. When compliance-ready, strategically located industrial land is reportedly commanding a major premium over reserve expectations, it shows that real infrastructure-linked value does exist. But it exists where zoning, access and institutional usability are already aligned.

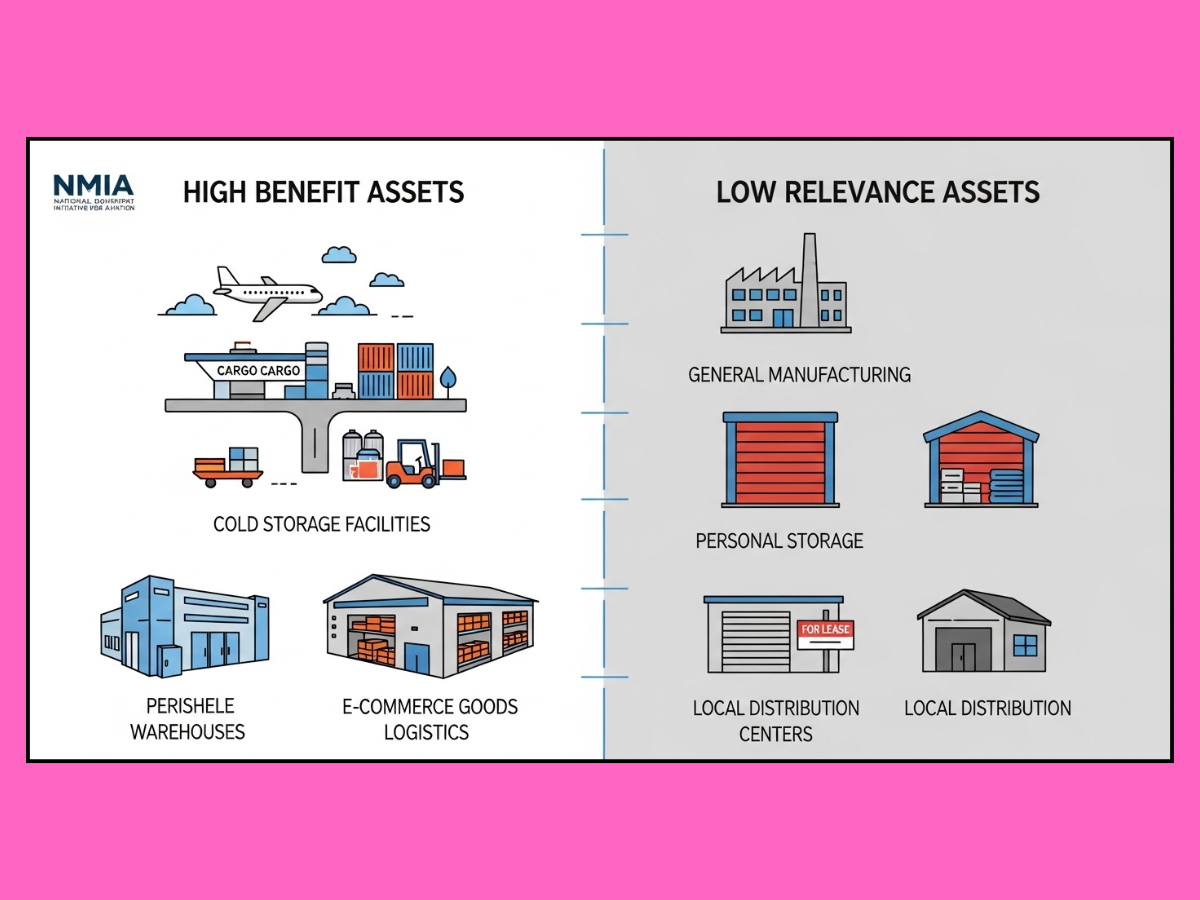

NMIA does not lift every industrial asset equally. Which properties gain the most from airport-led demand?

NMIA became operational on 25 December 2025. That date matters because the airport story is no longer proposal-stage speculation. It has moved into an active market phase.

But airport impact is the most misunderstood part of this subject.

NMIA does not automatically make every nearby industrial parcel more valuable. It benefits assets that fit airport-linked logistics. That usually means clean, fast, high-value, time-sensitive movement, not heavy industry.

Air-cargo, perishables, high-value distribution and time-sensitive logistics

Air cargo works differently from port cargo. The goods are usually lighter, more valuable, more time-sensitive and more dependent on speed, reliability and handling quality.

That is why the strongest NMIA-linked industrial demand is more likely in Grade-A warehousing, cold chain, pharmaceutical support, express distribution, e-commerce staging and value-dense cargo ecosystems. The FedEx automated cargo hub announcement is important because it turns airport-led cargo demand from a pure future story into an operationalizing one.

Still, this does not mean every surrounding plot deserves a premium.

Why being “near the airport” is not enough

Straight-line distance to NMIA is one of the biggest traps in the market. A tired old gala with poor loading, low clear height, weak fire systems and bad access does not become premium industrial stock just because the airport is nearby.

This is where many buyers confuse passenger halo with cargo halo.

Passenger halo can support residential, retail, hospitality and office stories. Cargo halo supports specialized warehousing and logistics stock. Those are not the same market. In fact, heavy or polluting industrial uses are often the wrong fit near a modern international airport ecosystem.

So when sellers push airport-led appreciation, ask a sharper question: which occupier exactly will lease this asset, at what rent, and why would they choose this property over a compliant modern facility with better access?

What freight corridors change in pricing terms: speed, reach, distribution logic, and occupier confidence

The Western Dedicated Freight Corridor changes pricing less through excitement and more through logistics mathematics. Once the final JNPT-connected leg became fully completed and commissioned in March 2026, the corridor shifted from a future promise to a live network advantage.

This matters because freight speed, network reliability and rail-road integration directly influence where distribution activity wants to sit.

How rail freight connectivity changes long-haul logistics economics

A freight corridor improves the line-haul side of logistics. It helps cargo move faster and more predictably over long distances. In theory, that reduces pressure to keep everything extremely close to the port because supply chains can now move goods inland more efficiently.

In price terms, this can redirect value away from only coastal storage and toward stronger inland hubs that work as break-bulk, sorting and distribution points.

Why road-linked inland belts can rerate even if they are not right beside the port or airport

This is why inland logistics belts such as Kalamboli and Panvel matter. They do not need to be right beside JNPA or NMIA to gain value. They gain value when they can sit at the intersection of highway movement, rail-linked confidence and broad regional distribution logic.

But this comes with a big warning. Freight-corridor logic only becomes real if last-mile access works. A belt can have great macro connectivity and still underperform because local truck movement is painful, junction delays are severe, or cargo turnaround gets killed at the last 3 to 5 kilometres.

Kalamboli is a good example of this two-sided story. It benefits from inland logistics positioning, but the Kalamboli Circle bottleneck remains a real friction point. In this market, the correct side of the bottleneck can matter more than a glossy corridor narrative.

Which belts in and around Navi Mumbai usually feel the strongest pricing effect first?

| Industrial Belt | Primary Engine | Best Asset Fit | Market Effects | The Risk Factor |

|---|---|---|---|---|

| Uran & Dronagiri | JNPA (Port) | Container logistics, Heavy warehouse | Strong price rise if access is clean | CRZ & Title Issues |

| Ulwe & Airport Belts | NMIA (Airport) | E-com, Cold Chain, Clean Cargo | Fastest land appreciation (Headline-led) | Hype vs Real Utility |

| Panvel-Kalamboli | WDFC + Highways | Grade-A Logistics, Large Campuses | Strong rental depth & distribution logic | Traffic Bottlenecks |

| Taloja Belts | Mfg. Utility | Industrial plots, Process units | Steady demand for utility assets | Compliance & Water |

| TTC-Side (Turbhe, Mahape) | City Logistics | Urban logistics, Last-mile units | Strongest rent support (Off-peak staging) | High Entry Cost |

Sale prices, rents, and speculative asking rates do not move together

This is where many industrial buyers get trapped.

Asking rates usually rise first because infrastructure headlines travel faster than occupier commitments. Sale prices may then rerate in pockets where confidence deepens. Rents only strengthen properly when actual users take possession and start paying for the operational advantage.

So a location can look expensive on paper and still be a weak income asset.

This is especially common in airport-influence belts. Land prices may jump 20% or more in a speculative cycle, but if the actual rentable product is not ready, yields stay thin. On the other hand, an inland warehouse belt with less glamour may produce better rent depth because occupiers actually need the space today.

For practical decision-making, always separate three numbers: the broker’s asking rate, the realistically transactable value, and the rent an occupier will genuinely support.

If these three are too far apart, the market is telling you the premium is still ahead of the cash flow.

Which asset types rerate fastest when infrastructure improves?

Not all industrial assets respond equally to infrastructure upgrades.

Ready Grade-A warehouses usually rerate fastest where logistics demand is already visible because they can be leased immediately. There is no delay caused by approvals, construction or major capex.

Bare industrial plots can show the sharpest percentage appreciation in a hot cycle, but they carry the highest execution risk. Zoning, CRZ restrictions, access width, NA status, approvals, construction cost and leasehold transfer conditions can all destroy the upside story.

Ready industrial sheds perform well where the built form genuinely matches user demand. In Taloja, for example, market ranges can vary sharply between bare plots and ready engineering or chemical sheds because utility and readiness matter.

Older gala stock often lags in the modern infrastructure cycle unless it has one special advantage, such as strong urban access, good last-mile location or a mid-sized staging role. This is why some TTC-side stock still holds relevance even though it is not glamorous. Operational usefulness can beat a bigger macro story.

Large logistics land parcels become attractive when institutional users want scale, expansion options and multimodal confidence. But these buyers are also the least forgiving on title, access and compliance.

When does infrastructure create a real premium, and when is it just a marketing premium?

Infrastructure creates a real premium only when the asset can convert macro advantage into daily operational savings for the occupier.

That means the property should pass a practical test. Is the use sanctioned? Can a 40-foot trailer reach it comfortably? Is the road width workable? Is turning radius manageable? Is there stable power, enough service depth, and room for loading movement? Can labour and supervisors reach the site without friction? Is the title or leasehold position clean enough for transfer, mortgage and future exit?

If these answers are weak, the premium is probably marketing-led.

This point matters even more in Navi Mumbai because straight-line closeness can be misleading. A property 10 kilometres from JNPA or NMIA can still be operationally inferior to another one farther away if approach roads are poor, local movement is slow, or the land use is not truly suitable.

In industrial real estate, usable distance matters more than map distance.

Where buyers and investors usually misread the JNPA-NMIA story

The first mistake is paying airport prices for land that has no airport-fit occupier base. This is common around developing belts where land banking gets sold through future storytelling.

The second mistake is assuming port influence and airport influence are interchangeable. They are not. JNPA supports bulk, containerized and EXIM-heavy logistics logic. NMIA supports speed, value density and cleaner logistics formats.

The third mistake is ignoring the hidden cost side. CIDCO leasehold transfer conditions, revised transfer charges, title restrictions and area-specific approvals can materially change returns. A deal can look cheap until these costs are added.

The fourth mistake is reading news as rent proof. A port throughput record, airport launch or corridor completion proves the infrastructure story is real. It does not prove your exact plot, gala or shed has already earned a justified premium.

The fifth mistake is underestimating local friction. Taloja’s water and utility realities, Kalamboli’s movement bottlenecks, CRZ-linked constraints in some coastal belts, and zoning mismatch in airport-side areas all affect the actual price an occupier will support.

How to judge whether today’s industrial price already includes tomorrow’s infrastructure upside

A simple five-part decision framework works well here.

First, check whether current rent support is healthy. If the property is already priced so high that the achievable yield looks weak, a lot of tomorrow’s upside may already be priced in.

Second, check occupier depth. Is there real demand from logistics, manufacturing or distribution users in this exact belt, or only investor excitement?

Third, check local vacancy and product fit. A market full of mismatched or obsolete stock can still have strong headline appreciation but weak income performance.

Fourth, check land-use and transfer clarity. If leasehold restrictions, approvals or sanction issues remain unresolved, then pricing may be running ahead of legal usability.

Fifth, check access readiness now, not in theory. A corridor or airport may be live, but if your site still fails the last-mile movement test, the upside is not truly yours.

A blunt rule helps: if you are paying future-grade pricing for present-day weak yield, you are not buying infrastructure upside. You are prepaying for hope.

What should a buyer verify before paying an infrastructure premium in Navi Mumbai?

Before booking or closing any industrial asset, verify the structure of the rights first. In many cases, this is not freehold in the ordinary sense. CIDCO typically allots land on a leasehold basis, and transfer conditions matter.

Then verify sanctioned use through the relevant development framework and records. Do not rely on broker language like “commercial-industrial use possible” unless it is backed by actual documents. IGR Maharashtra can help as a benchmark layer, but it should not be treated as proof of real transaction value or full legal usability.

Also identify the authority context properly. NMMC, PMC, CIDCO and NAINA-side planning realities do not behave identically. Tax burden, development control, approvals and service conditions can vary.

Finally, inspect the asset like an operator, not a speculator. Check road width, loading practicality, trailer access, turning radius, parcel shape, power depth and labour movement. Infrastructure premium is only worth paying when the asset can be used without daily friction.

Conclusion

JNPA, NMIA and freight corridors are absolutely reshaping industrial property pricing in and around Navi Mumbai, but they do so through different channels and at different speeds. JNPA is strongest where port dependence is real. NMIA is strongest where speed-driven cargo logic exists. Freight corridors help inland logistics belts that can convert connectivity into daily throughput.

The market mistake is to pay one blended “infrastructure premium” everywhere. The smarter approach is to ask four practical questions every time: which engine is driving this location, which asset type actually fits that engine, whether rents support the price, and what local friction still remains. In Navi Mumbai industrial real estate, infrastructure creates value only when the property can use it, not merely advertise it.