Navi Mumbai Airport Rental Demand Impact: Which Areas Are Seeing the Biggest Surge

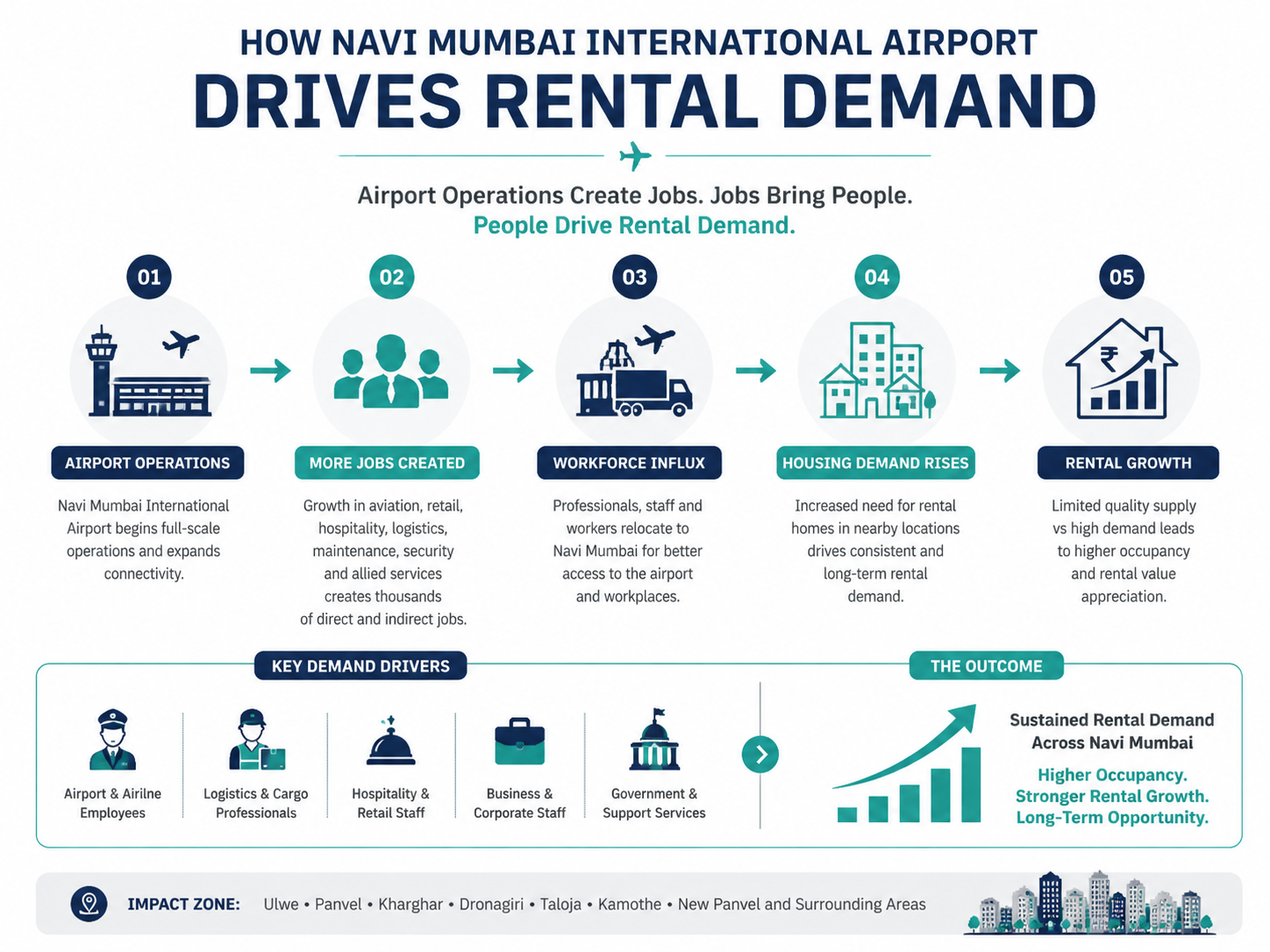

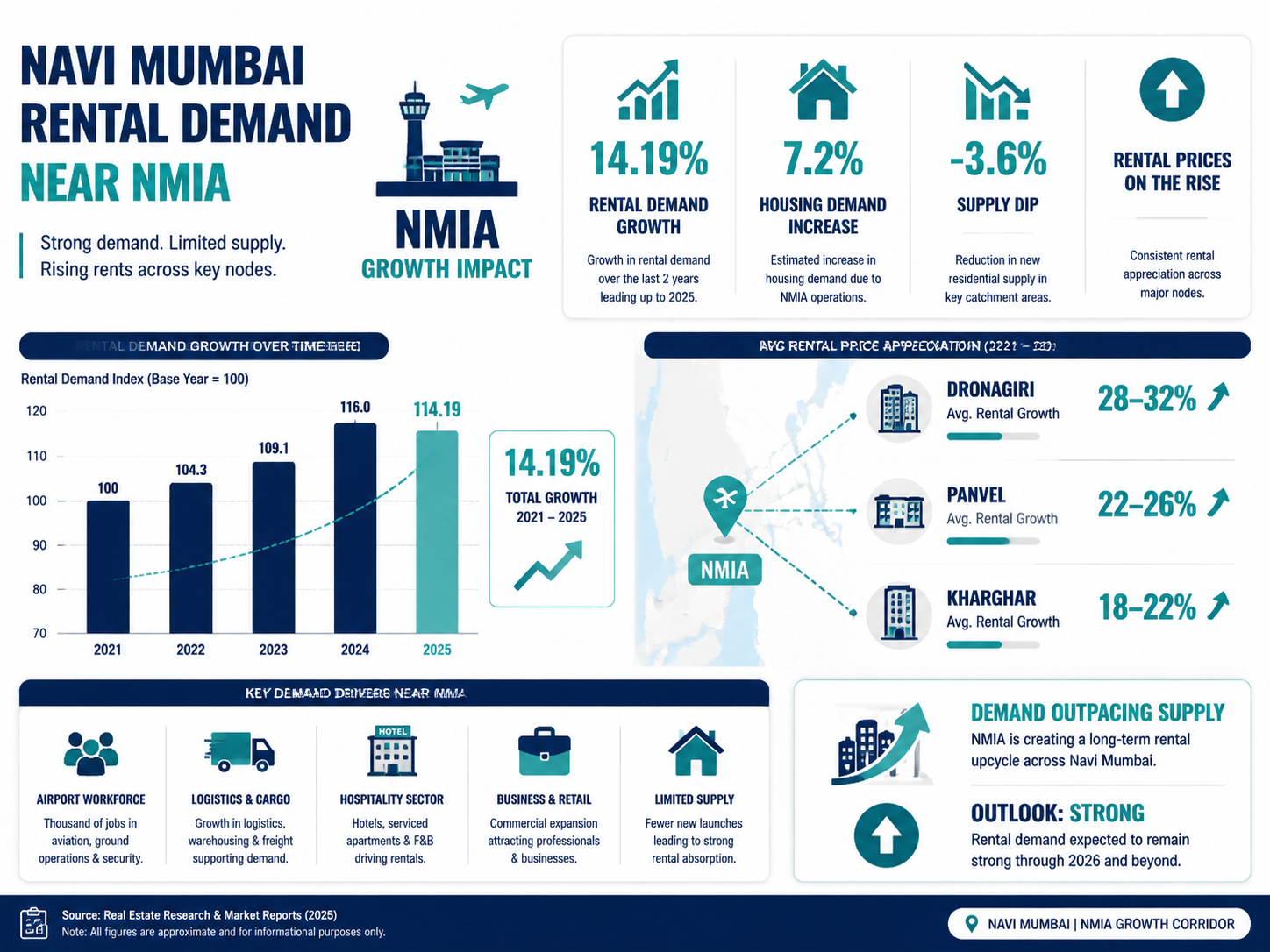

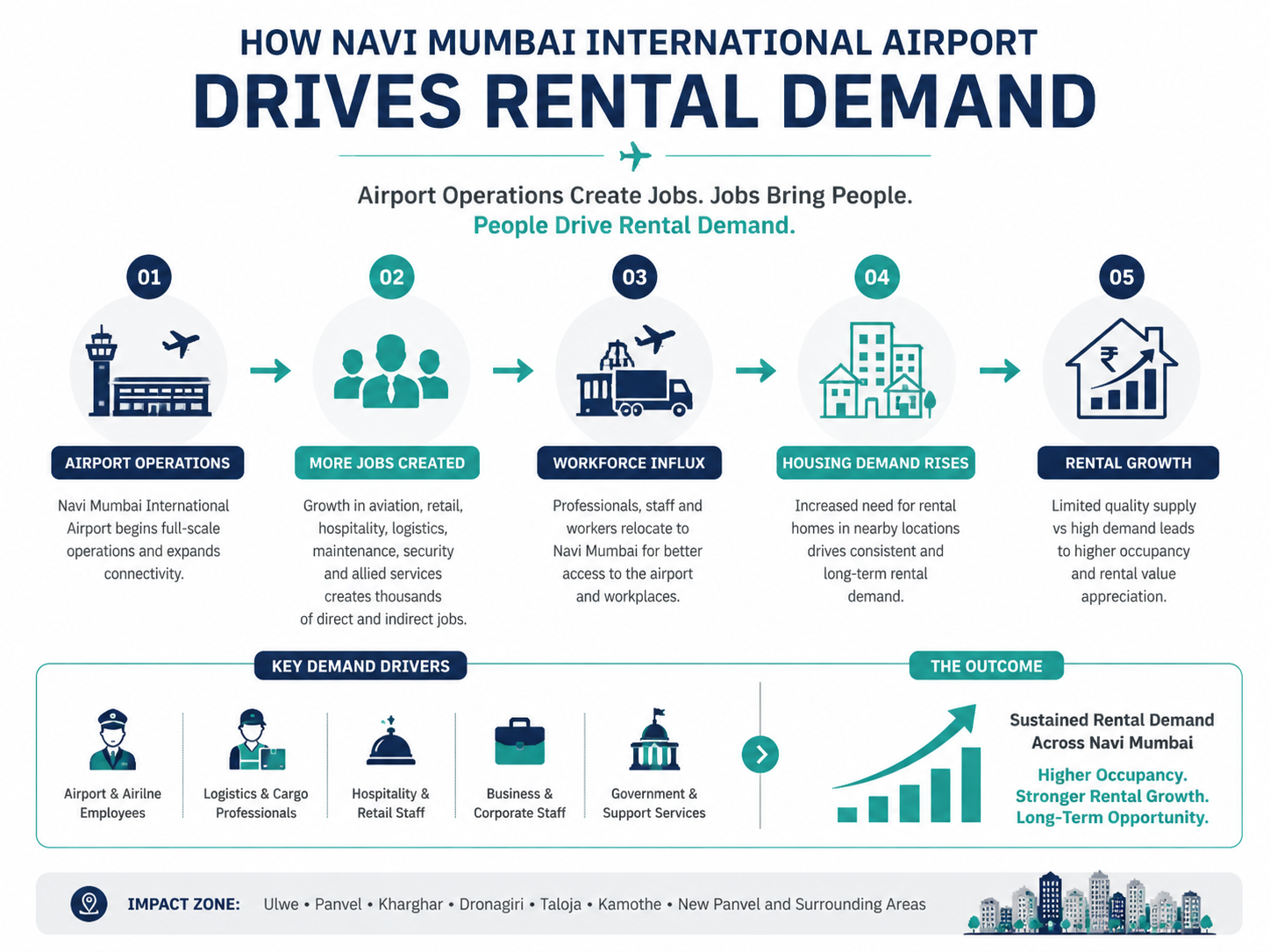

Rental demand in Navi Mumbai rose 14.19% over the two years leading up to 2025, with the Navi Mumbai International Airport (NMIA) emerging as the dominant driver of that growth. As operations scale through 2026, the rental market across Ulwe, Panvel, Kharghar, and surrounding nodes is entering a demand-led expansion phase that property analysts expect to sustain through at least 2030.

This is no longer speculative. NMIA commenced commercial flights on December 25, 2025, and moved to 24/7 operations in February 2026. The airport economy is now generating real jobs, real workers, and real rental demand.

Why NMIA Is Driving Rental Demand

Every operational airport creates a workforce catchment zone. The larger the airport, the wider and denser that zone becomes.

NMIA is designed to handle 20 million passengers annually in Phase 1, scaling to 90 million by 2032. That growth trajectory implies a corresponding expansion in airport staff, ground handlers, airline crew, logistics workers, customs officials, hospitality employees, and the broader service economy that clusters around major aviation hubs.

Add to that:

- The FedEx Rs 2,500 crore cargo hub generating over 6,000 direct and indirect jobs

- Planned Aerocity development with office parks, hotels, hospitals, and retail

- Logistics parks, warehousing clusters, and ancillary service companies relocating to the NMIA corridor

The result is a sustained pipeline of professionals needing housing within practical commuting distance of the airport. That is the foundation of rental demand growth, and it is compound in nature: more airport activity creates more jobs, which creates more rental demand, which attracts more housing investment.

Rental Demand Data: What the Numbers Show

According to [Magicbricks data reported by BusinessToday], rental demand in Navi Mumbai increased 14.19% over the two years to late 2025. That figure covers the broader Navi Mumbai market.

Within the airport-linked micro-markets specifically (Dronagiri, Kharghar, Panvel, Ulwe, and Uran), overall housing demand rose 7.2% even as supply dipped 3.6% on average. Supply-demand compression in rental markets typically precedes rental yield expansion.

Property price appreciation in the same zone during this period:

- Dronagiri: 41.9% price increase

- Panvel: 26.05% price increase

- Kharghar: 19.75% price increase

Demand for plotted developments in the same corridor surged sharply: Panvel +209.85%, Uran +205.43%, and Dronagiri +160.87%. While this reflects investor activity as much as rental demand, it signals the depth of conviction in the long-term rental income potential of these areas.

Micro-Market Breakdown: Where Rental Demand Is Concentrating

Ulwe: The Primary Airport Residential Catchment

Ulwe is geographically the closest major residential node to the NMIA terminal. Five years ago, residential prices in Ulwe averaged Rs 5,500 to Rs 6,500 per square foot. By 2026, established sector prices range from Rs 9,000 to Rs 13,000 per square foot, representing 60 to 80% capital appreciation.

According to [Housivity’s January 2026 market analysis], Ulwe is expected to emerge as the primary residential catchment near the airport. The profile of incoming tenants is shifting toward airport and logistics sector workers who need proximity to the terminal without the premium pricing of central Navi Mumbai.

For landlords, this creates a reliable mid-market rental base with relatively low vacancy risk. As airlines scale operations and logistics clusters around NMIA mature, the tenant pipeline deepens.

Current market rates in Ulwe (2026) have stabilized at Rs 10,500 to Rs 12,500 per square foot for negotiated deals, with premium airport-view projects asking Rs 15,000+.

Panvel: The Long-Term Rental Hub

Panvel’s rental story is different from Ulwe’s but equally compelling.

The area’s strength comes not from airport proximity alone, but from infrastructure depth. Panvel sits at the intersection of the Mumbai-Pune Expressway, the Atal Setu corridor, and the future metro expansion, making it viable as a primary residence for professionals working across the broader MMR region.

According to [The Propertyist’s 2026 analysis], this gives Panvel a relatively balanced investment profile with strong rental potential and steady appreciation. The airport has accelerated demand, but Panvel’s broader advantage lies in becoming a transport and logistics hub for the larger MMR region.

Property prices in Panvel have moved from approximately Rs 6,000 per square foot to Rs 9,500 to Rs 11,500 per square foot over five years, a 50 to 60% appreciation. [According to Godrej Properties], with improved connectivity through the Atal Setu, Mumbai-Pune Expressway, and future metro lines, Panvel is fast becoming a prime investment zone.

The Atal Setu specifically has been transformative for Panvel’s rental appeal. By cutting commute times from South Mumbai to the Panvel region to approximately 20 to 45 minutes, the 21.8-kilometer sea bridge has made Panvel viable as a primary residence for professionals working in traditional Mumbai business districts.

Kharghar: Premium Rentals, Established Infrastructure

Kharghar operates at a different segment of the rental market. It already had a well-developed residential base before the airport boom began, with solid social infrastructure: schools, parks, hospitals, and the operational Metro Line 1.

According to [Housivity], the upcoming Metro Line 1 expansion is expected to further boost rental yields in Kharghar, making it a prime target for HNI (high-net-worth individual) rental portfolios. Current prices range from Rs 15,000 to Rs 18,000 per square foot for premium locations.

The rental demand in Kharghar is driven by a more senior corporate tenant base: executives, expats, senior logistics professionals, and families who prioritize liveability alongside connectivity. Airport-linked demand here is a secondary driver; established residential quality is primary.

Dronagiri: Early-Stage but High Conviction

Dronagiri is the highest-risk, highest-potential node in the airport rental corridor. Located within the JNPT-SEZ zone and adjacent to the airport influence area, it has recorded 41.9% price appreciation over two years.

Demand for plotted development in Dronagiri surged 160.87%, which reflects investor conviction in the long-term rental income potential of the area as JNPT and NMIA cargo operations scale. However, Dronagiri’s social infrastructure is still developing, which limits near-term tenant demand to logistics-sector workers rather than a broad professional base.

Prices in Dronagiri currently range from Rs 6,500 per square foot on the lower end, offering an entry point for investors with a 5 to 7 year horizon.

What Kinds of Tenants Are Coming

Understanding the tenant mix helps investors calibrate what to build and where.

Airport and airline workforce: Cabin crew, ground staff, airline operations employees, and airport services workers need housing within 20 to 30 minutes of the terminal. Ulwe and Pushpak Nagar absorb most of this demand.

Logistics and warehousing professionals: As logistics parks around NMIA mature, a substantial workforce of operations managers, supply chain professionals, and warehouse staff will need housing within commuting range. Panvel and Taloja are likely primary destinations.

Corporate and expat tenants: As the planned Aerocity develops with office parks and commercial zones, senior corporate tenants and expats will add to premium rental demand in Kharghar, Panvel, and Seawoods.

Healthcare workers: With Medicity developments planned in the NAINA zone, a cluster of healthcare professionals will add a stable, long-term rental cohort to the market.

Transit workers: NMIA’s multimodal connectivity plan, including the planned Gold Line Metro connecting NMIA to CSMIA, will draw professionals who work across both airport zones, with rental demand following the metro corridor.

Rental Yield Outlook: What Investors Can Expect

[Analysts quoted by Tharwani Constructions] forecast sustained annual growth of 15 to 20% in Ulwe, Panvel, and Kharghar corridors until 2030 as airport-linked infrastructure matures. Rental yields are expected to rise as incoming professionals and the airport-linked workforce increase occupancy rates.

The broader market context supports this:

Historically, global twin-airport cities including London and Dubai show that the steepest price appreciation often happens 2 to 5 years after an airport opens, as the surrounding ecosystem of hotels, logistics facilities, malls, and offices matures. NMIA opened commercially in late 2025. By that logic, 2026 to 2030 represents the highest-return window for rental-yield investors.

The supply-demand dynamic also favors landlords. Supply in airport-linked micro-markets dipped 3.6% on average over the two-year period to 2025, while demand rose 7.2%. That imbalance, if it persists as job creation accelerates, will compress vacancy rates and provide upward pressure on rents.

Infrastructure Catalysts Still Ahead

Several infrastructure projects will add further rental demand momentum as they complete:

Gold Line (Metro Line 8): Will connect NMIA directly to CSMIA, creating a new corridor of residential demand between the two airports. Properties along this Metro 8 corridor are currently considered undervalued.

Metro Line 1 Expansion (Kharghar): Will improve commute options for Kharghar residents and add to the area’s rental premium.

NAINA Aerocity Development: The planned aerocity zone adjacent to NMIA will add large-scale commercial and hospitality development, generating sustained professional rental demand in surrounding nodes.

CIDCO Planned Infrastructure: Roads, utilities, and civic infrastructure under NAINA’s Town Planning Schemes are rolling out in phases, progressively making underdeveloped areas more livable and rental-ready. [Verify current TPS approval status with CIDCO before investment.]

Key Considerations for Rental Investors

Before investing for rental income near NMIA, assess these factors:

Connectivity over proximity: Being closest to the airport is less important than being well-connected to where tenants work. A flat in a well-connected node 15 minutes from the terminal will rent more consistently than one 5 minutes away with poor road access.

Developer quality and possession timeline: Multiple new launches have hit the market simultaneously. Verify MahaRERA registration, developer track record, and realistic possession dates via [MahaRERA’s official portal].

Project quality relative to price: With multiple micro-markets seeing simultaneous launches, the risk of purchasing an over-priced unit in an underdeveloped node is real. Match project quality to the likely tenant profile for that area.

Absorption timeline: Rental income depends on actual occupancy, not airport operations starting. Allow for 12 to 24 months of ramp-up time between airport scaling and full rental market absorption.

This article is for informational purposes only and does not constitute financial or investment advice. Verify all facts with a registered property advisor and consult MahaRERA records before any investment decision.

FAQ

Q: How much has rental demand increased near Navi Mumbai Airport? A: According to Magicbricks data, rental demand in Navi Mumbai increased 14.19% over the two years to late 2025, with airport-linked micro-markets seeing the strongest demand growth.

Q: Which area near NMIA has the highest rental demand growth? A: Uran and Kharghar have recorded the highest demand growth at 39.33% and 16.21% respectively within the airport-linked corridor. Ulwe is expected to be the primary residential catchment for airport workers.

Q: What rental yields can investors expect near NMIA? A: Analysts forecast sustained annual appreciation of 15 to 20% in Ulwe, Panvel, and Kharghar corridors until 2030. Actual rental yields will vary by location, property type, and occupancy rates. [Verify with a registered property advisor.]

Q: What types of tenants are expected to drive rental demand near NMIA? A: Airport and airline workers, logistics and warehousing professionals, corporate and expat tenants in the future Aerocity zone, and healthcare workers in the planned Medicity development are the primary tenant cohorts.

Q: What is the current price range for properties in the NMIA rental corridor? A: Prices range from Rs 6,500 per square foot in developing areas like Dronagiri to Rs 18,000 per square foot in premium Kharghar locations, with Ulwe sitting at Rs 9,000 to Rs 13,000 per square foot.

Q: How does the Atal Setu affect rental demand in the NMIA corridor? A: The Atal Setu (Mumbai Trans Harbour Link) reduced commute times from South Mumbai to the Panvel-NMIA region to approximately 20 to 45 minutes, making the corridor viable as a primary residence for professionals working in traditional Mumbai business districts. This significantly expanded the potential tenant base.

Q: Is it too late to invest for rental income near NMIA? A: The speculative phase (2018-2024) has passed. The airport entered its utility phase in 2025-2026, with prices now rising on real job creation and occupancy. Historical data from global twin-airport cities suggests the steepest appreciation and rental yield growth typically occurs 2 to 5 years after an airport opens.