How to Value Commercial Property in Navi Mumbai: Shop, Office, Rent and Resale Guide

If you want to value commercial property in Navi Mumbai properly, do not use one flat rate per square foot. A shop, office, showroom, gala, or pre-leased unit should be valued through five layers: Ready Reckoner reference, real local comparables, rent and net income, micro-location and usability, and finally legal or transfer friction. In short, the right answer is usually a valuation band, not one magical number.

Most buyers get trapped because they compare the wrong things. They compare a ground-floor shop with an upper-floor office, or they compare a brochure rate with a resale deal, or they assume anything above Ready Reckoner means overpaying. That is not how Navi Mumbai works.

Navi Mumbai’s commercial market is also not operating in a vacuum. The Atal Setu opened to traffic on 13 January 2024, and Navi Mumbai International Airport began commercial operations on 25 December 2025, so access-led corridors, airport-linked belts, and older business districts are not being valued on the same logic anymore.

Quick Summary: What should drive value for each commercial unit type?

| Unit type | Primary valuation anchor | Biggest value trap | Best cross-check |

|---|---|---|---|

| Street-facing shop | Frontage, visibility, walk-in quality, parking practicality | Blindly paying for “main road” without checking actual access and customer stopability | Compare similar nearby ground-floor deals, not generic sector rates |

| Office space | Usable layout, building image, access, lift quality, parking, tenant profile | Pricing by super built-up area instead of real usable area | Convert everything to carpet or true usable area before comparing |

| Showroom | Road presence, signage visibility, loading practicality, catchment spending power | Assuming all wide-road locations convert equally well | Check business type suitability, road speed, stopping space, and frontage length |

| Pre-leased unit | Net operating income and tenant quality | Believing headline rent without checking tax, CAM, lock-in, and tenant strength | Value on true net yield, not gross rent |

| Vacant resale unit | Comparable sales plus downtime discount | Treating vacancy as temporary noise instead of a cost | Estimate realistic tenant-finding time and fit-out dependence |

| Gala / industrial commercial | Height, loading, truck access, compliance, operational usability | Calling every industrial-style unit “commercial” and using retail logic | Value based on operational use, not cosmetic price pitch |

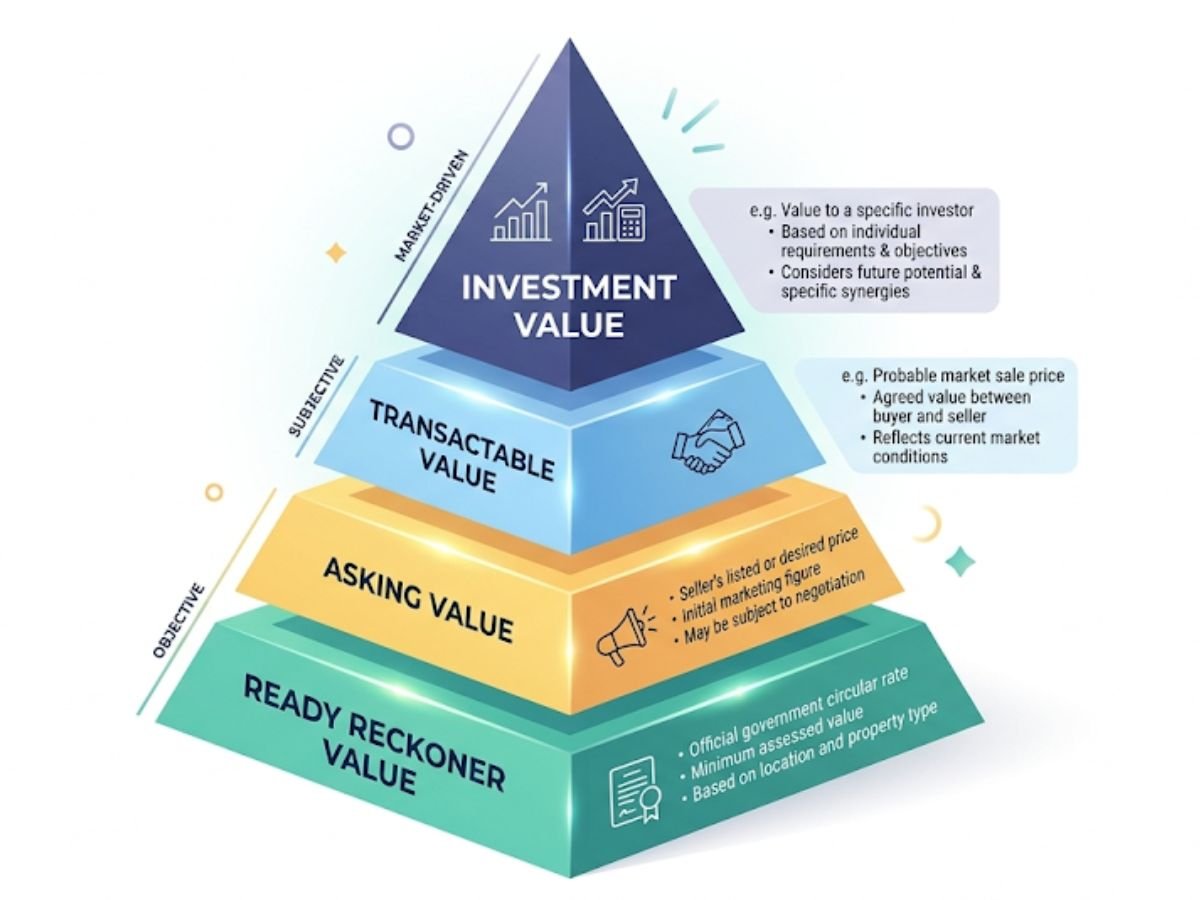

What does “commercial property value” actually mean here?

In Navi Mumbai, commercial property value usually means four different things, and people mix them up all the time.

The first is the Ready Reckoner or eASR value. This is the statutory benchmark used in the registration ecosystem. The IGR Maharashtra eASR platform itself says the system gives only a rough indication of rates and asks users to verify the rate with the department. It is a floor or reference point, not a full market valuation. The same portal currently shows annual statement cycles including 2026–27, which is why you should always pull the exact current year before relying on any RR number.

The second is the asking value. This is what sellers, brokers, and developers quote. It often includes optimism, future-story pricing, and negotiation cushion.

The third is the transactable value. This is the price a real buyer may actually pay after adjusting for building quality, access, rent quality, tax burden, transfer fees, and document friction.

The fourth is the investment value. This is what the property is worth to an income-focused buyer after looking at realistic rent, outgoings, vacancy risk, and exit quality.

That difference matters. A unit can look cheap versus nearby listings and still be overpriced if the title chain is weak, parking is unusable, or the rent is poor after expenses.

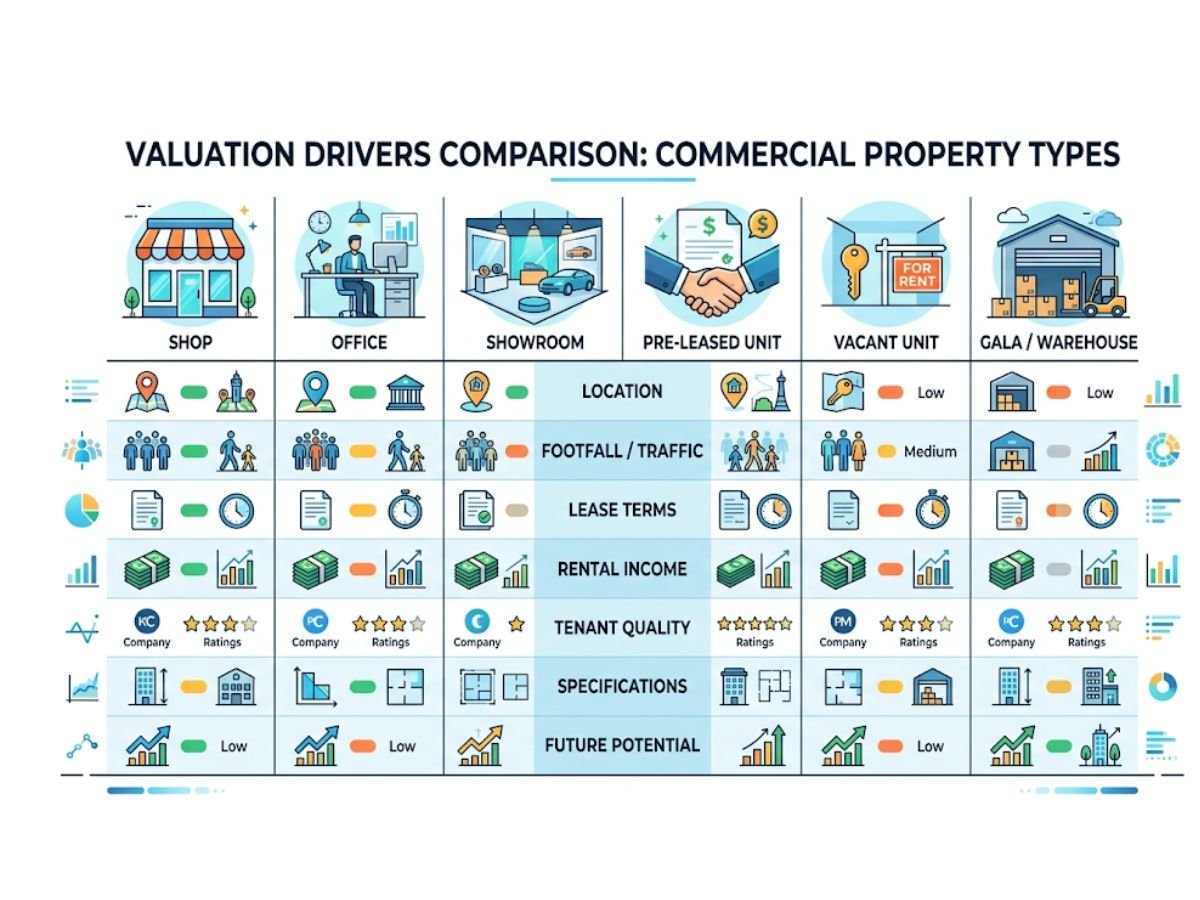

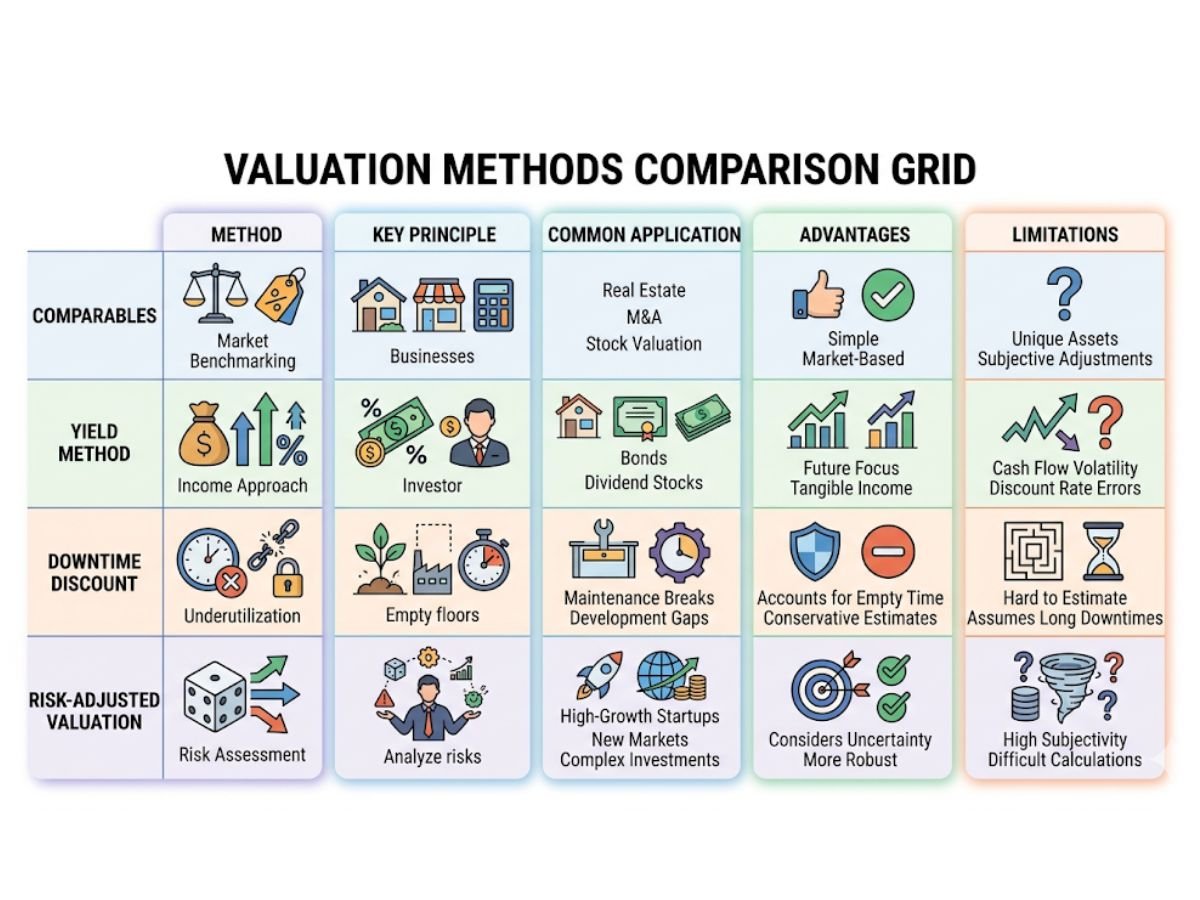

Which valuation method should you use for this unit type?

There is no single best method for every commercial asset. The right method depends on what exactly you are buying.

| Unit scenario | Best method | Weak method | What you must verify before trusting the number |

|---|---|---|---|

| Self-use shop or office | Comparable sales plus usability adjustment | Pure yield method | Carpet area, frontage, floor level, access, parking, building condition |

| Pre-leased office or shop | Net income / yield method | Raw brochure rate comparison | Actual rent received, lock-in, tenant quality, expenses, tax burden |

| Vacant resale unit | Comparables minus downtime discount | Blind rent assumption | Time to tenant, fit-out need, floor plate efficiency, local demand depth |

| Under-construction commercial | Risk-adjusted comparison | Treating it like ready stock | MahaRERA status, CC, delivery risk, carrying cost, possession realism |

For a self-use office or shop, comparable sales matter more than brochure pitch

If you are buying for your own business, the most important question is simple: what are similar usable units in that exact micro-market actually worth? A front-facing shop in Vashi or Nerul cannot be judged by the same rate as a back-side office in the same building.

For a leased asset, rent quality matters more than the headline yield story

A pre-leased property is not automatically premium. A long lock-in, clean payment history, sensible escalation, and a tenant that fits the building matter far more than a flashy sentence like “assured rental.”

For a vacant resale unit, exit and downtime matter

A vacant unit should usually be valued at a discount to an equally good, income-producing unit unless the location is so strong that absorption is genuinely fast.

For under-construction stock, risk haircut is mandatory

MahaRERA covers both residential and commercial real estate, and its FAQ also says a Commencement Certificate should be submitted for registration of a real estate project. That means under-construction valuation should never ignore compliance and delivery risk.

Where should you start: Ready Reckoner, market listings, or recent deal evidence?

Start with all three, but do not worship any one of them.

Ready Reckoner gives you the statutory base. Listings give you the market’s asking mood. Recent deal evidence gives you the closest thing to reality. The mistake is relying on only one.

> Why Ready Reckoner cannot be your final commercial valuation > The eASR portal itself says it gives only a rough indication of rates and asks users to verify the figure with the department. So RR is useful as a legal and tax reference, but it is not the same thing as transactable market value.

A practical way to use RR is this: treat it as the floor below which you should question the structure of the deal. Then treat portal listings as the ceiling of seller expectation, not proof of achieved value. Even commercial tracker pages showing Navi Mumbai asking-price bands or average prices are still tracker data, not guaranteed registry-clearing prices.

So the right starting question is not, “What is the rate in this node?” It is, “What is the RR floor, what are similar people asking, and what discount or premium does this exact unit deserve?”

How do shops, offices, showrooms, and gala-style commercial units get valued differently?

Shops are valued on visibility first, then on conversion practicality

For a shop, frontage matters. But not all frontage is equal. A visible unit on a busy road with impossible stopping, poor customer parking, and weak pedestrian pause time may look premium but convert badly. In many Navi Mumbai belts, this is the difference between a strong ground-floor asset and a stubborn resale listing that stays online for months.

Offices are valued on usability, image, and access

An office buyer should care about real working space, not lobby drama. Lift reliability, power backup, parking, floor efficiency, façade quality, and daily commuter convenience matter more than a brochure promise. In Airoli and Belapur especially, corporate users often pay for function first.

Showrooms are valued on road presence and catchment fit

A showroom is not just a bigger shop. It needs display logic, loading practicality, and a road environment where your signage is seen and understood. Fast-moving corridors can give visibility but still reduce real conversion if stopping and browsing are weak.

Galas and industrial-style commercial units follow operational logic

In Turbhe, Taloja, and similar industrial-commercial belts, ceiling height, truck movement, floor load, and legal usage matter more than polished interiors. A good gala for operations can outperform a prettier but less workable space.

This is why a blended “commercial rate” for one sector is often meaningless. Same building, same super area, completely different value logic.

How much does location change value inside Navi Mumbai?

A lot. And not just by node. By pocket.

Station-linked commercial belts in Vashi, Sanpada, Belapur, and Nerul often carry a connectivity premium because staff, clients, and walk-in users can reach them easily. At the same time, internal sectors may trade lower even within the same node because visibility, parking, and movement are weaker.

Palm Beach-facing or arterial-road-facing property can attract a premium, but only when that visibility is useful for the intended business. A clinic, coaching centre, or office may not benefit from the same exposure pattern as a quick-service retail unit.

Then comes the bigger city-level split. Mature nodes like Vashi, CBD Belapur, Airoli, and parts of Nerul or Seawoods usually behave more like yield-and-occupancy markets. Growth belts such as Ulwe, Panvel-side corridors, and some airport-influence pockets carry more story-driven upside but also more vacancy and timing risk. The Atal Setu and NMIA have strengthened this split rather than removed it. :contentReference[oaicite:5]{index=5}

So yes, location changes value. But in commercial real estate, “location” means at least five things together: node, micro-pocket, station access, road quality, and actual business usability.

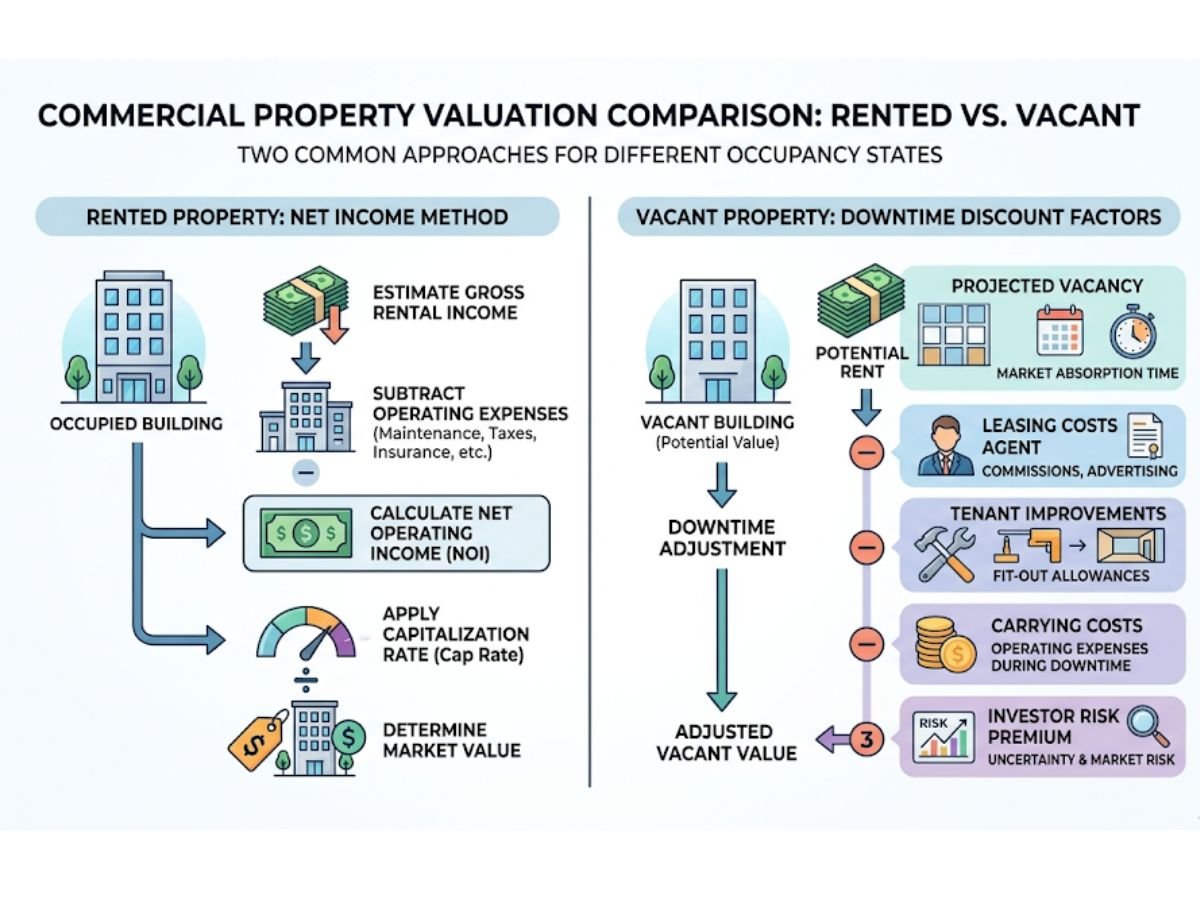

How should you value a rented commercial unit versus a vacant one?

A rented unit should be valued on true net income, not on the rent number printed in the brochure or WhatsApp forward.

That matters even more in Navi Mumbai because the commercial property tax burden is heavy. A widely cited NMMC calculation guide states that commercial and industrial properties are taxed at 68.33% of rateable value, far higher than residential property. So if you ignore tax, you can easily overvalue a so-called income property. Always verify the actual municipal ledger separately before closing. :contentReference[oaicite:6]{index=6}

A simple practical equation is:

Gross annual rent minus municipal property tax minus CAM and building outgoings minus vacancy reserve equals true net operating income

Only after that should you think about yield.

A vacant unit works differently. Here you need to ask:

- How long will it stay vacant?

- Does the next tenant need heavy fit-out?

- Is this a tenant-friendly building or just a seller-friendly story?

- Does the unit type fit actual local demand?

A weak pre-leased asset can absolutely be worth less than a good vacant asset. If the tenant is weak, the lock-in is short, the rent is below market, and the building is aging badly, the “pre-leased” tag does not rescue the valuation.

What building-level factors move value before legal checks even begin?

Before documents, look at the physical truth.

The first thing to control is area illusion. If you compare units by super built-up area without converting to RERA carpet or at least true usable area, you can fool yourself very quickly. Two offices both marketed as 1,000 sq ft can be very different if one gives you a far more efficient usable layout.

Then check:

- whether the floor plate is awkward or efficient

- whether lifts are enough for the building load

- whether customer or employee parking is truly usable

- whether washrooms and common areas are maintained

- whether façade and signage support the kind of business you want

- whether power backup and building management are reliable

This is also where mezzanine floors need caution. If a seller is trying to charge full commercial rate for an internal mezzanine or loft, do not assume it has full legal value. In many cases, the real question is not “Does it exist?” but “Is it approved?”

Which legal and authority-side issues can sharply reduce commercial value?

This is where many buyers get hurt.

Sanctioned use and commercial approval status

A unit must be approved for the use being sold to you. If the building is marketed like commercial but the sanctioned position is weak, the discount should be real, not emotional.

OC, CC, and actual readiness

For under-construction or new stock, MahaRERA matters because it allows you to verify project registration and document status. Its FAQ says the law covers commercial real estate, and a Commencement Certificate should be submitted for registration. :contentReference[oaicite:7]{index=7}

Leasehold and CIDCO transfer friction

This is one of Navi Mumbai’s most important valuation filters. CIDCO’s town services page makes clear that Navi Mumbai property has a leasehold legacy and that transfer is a formal process in this ecosystem. Indian Express reported that CIDCO increased transfer fees across Navi Mumbai from 1 April 2025, with a 5% to 10% hike depending on size and type, while flats in registered societies and commercial shops faced a 50% hike. The same report said large commercial properties above 200 sq m could attract very high per sq m charges. :contentReference[oaicite:8]{index=8}

That means a resale commercial unit with broken transfer history, unpaid CIDCO dues, or incomplete paperwork is not “cheap.” It is burdened. Your valuation should fall by the expected financial liability and by something extra for time, risk, and paperwork friction.

Parking assumptions

MahaRERA’s own FAQ says open parking area is part of common areas and sale or allotment of open parking area by the promoter is not permissible. So if a price pitch is inflated because of “open parking sale value,” that needs immediate caution.

> Why a legally weak unit can be cheaper and still be overpriced > Because the discount visible on the listing may be smaller than the hidden cost of transfer dues, missing approvals, unpaid taxes, parking mispricing, document repair, and transaction delay.

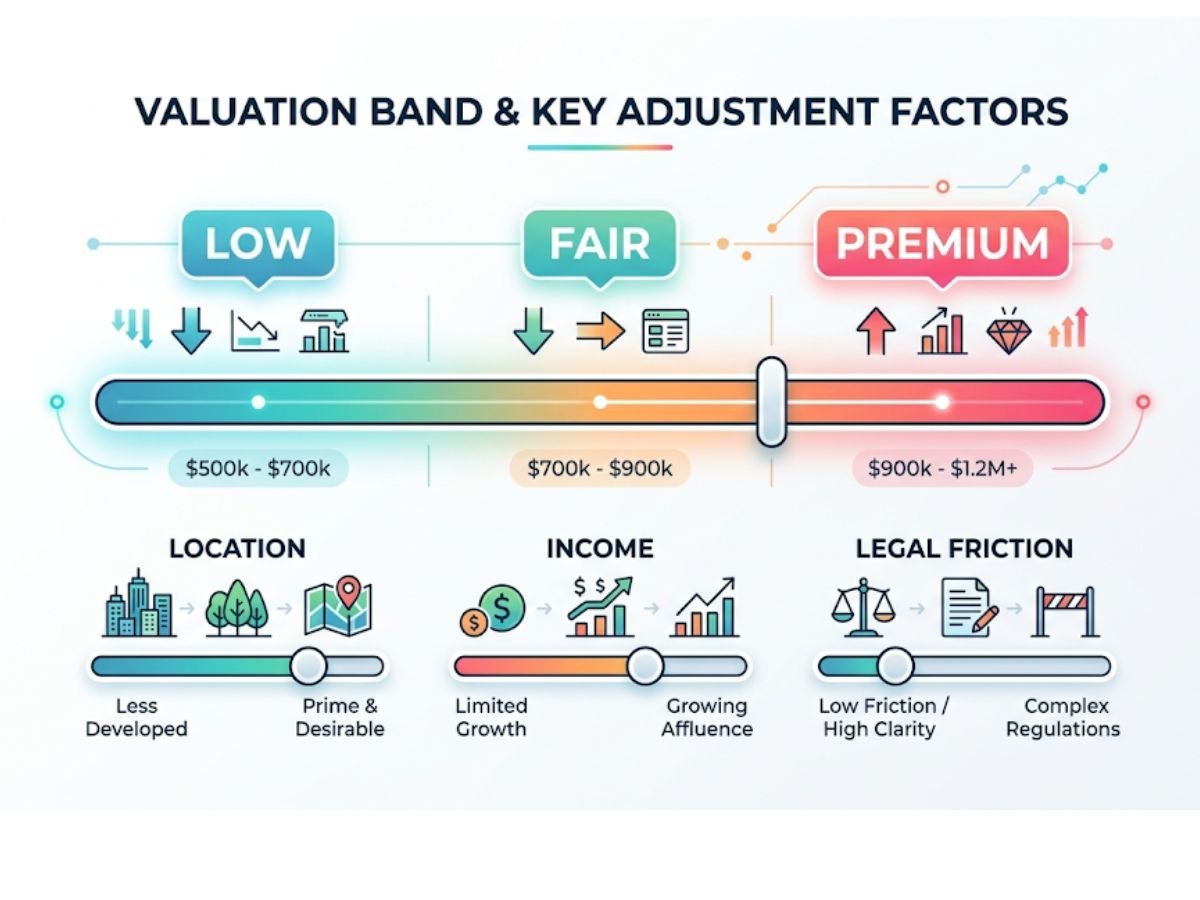

How do you calculate a realistic valuation band instead of one fake exact number?

Use this simple Navi Mumbai commercial valuation method:

1. Pull the statutory reference Check the exact current eASR zone and year. Use it as a floor, not the answer.

2. Collect 3 to 5 real comparables Same node is not enough. Try to match road exposure, floor, building age, and use case.

3. Standardize the area basis Convert all rates to carpet area or at least to a genuinely comparable usable-area basis.

4. Add or subtract usability adjustments Main-road frontage, station convenience, parking, better layout, stronger building image, or poor access.

5. Adjust for occupancy status Leased unit? Use net income logic. Vacant unit? Apply downtime discount.

6. Apply legal-friction discount CIDCO transfer history, dues, sanctioned-use mismatch, unapproved structures, tax arrears, or document gaps.

7. Create a low-mid-high band Low = cautious value Mid = fair transactable value High = justified premium only if the asset is genuinely cleaner and stronger than peers

That last step matters. Buyers who insist on a single exact number usually end up pretending the messy parts do not exist.

A simple Navi Mumbai commercial valuation workflow you can use before making an offer

Day 1: Pull the official anchors Check the current eASR year and exact zone. If the property is under construction or recently completed, check MahaRERA. Day 2: Visit the property like a user, not a dreamer Stand outside. Watch stopping space, frontage quality, internal circulation, building occupancy, lift wait time, and who is actually using the building.

Day 3: Normalize the area Do not compare one unit on SBA and another on carpet. Put everything on the same basis.

Day 4: Rebuild the income math If the unit is rented, calculate true net income after tax and building outgoings.

Day 5: Check transfer and dues Ask about CIDCO transfer history, NOC status, tax ledger, and pending liabilities. The property tax portal should also be checked for dues.

Day 6: Build your valuation band Low, fair, premium. Not one guess.

Day 7: Negotiate with reasons Do not just say “reduce the price.” Say exactly why: poor parking, weak tenant, loading issue, transfer liability, tax arrears, or low usability.

Three practical examples of how valuation changes in real situations

1) The Vashi shop that looks premium but fails on parking

Suppose two similar-sized ground-floor shops are available in Vashi. One is on a visible road but customers cannot stop easily, signage is partly blocked, and there is no practical parking. Another is inside a more organized commercial cluster with slightly lower road drama but better stopping and repeat customer convenience.

The first seller may quote more because of road visibility. But for many retail categories, the second unit may deserve the stronger valuation because it is easier to trade from. That is the difference between visual premium and operating premium.

2) The Airoli pre-leased office with misleading rent math

Suppose an office is shown at ₹2.4 lakh monthly rent. At first glance it looks attractive. But once you remove municipal tax impact, CAM, periodic vacancy, and rent weakness versus newer competing buildings, the real net income may justify a lower purchase price than the seller wants.

This is exactly why “pre-leased” is not a shortcut word. It is just the beginning of the math.

3) The Belapur resale office with CIDCO friction

A resale office in CBD Belapur may appear attractively priced versus nearby asking rates. But during due diligence, you find transfer-related gaps, delayed paperwork, or unpaid authority-side liabilities. In that case, your valuation should not just reduce by the exact dues. It should also reduce for time, uncertainty, and execution friction.

That is real commercial pricing. Not brochure pricing.

Common mistakes people make when valuing commercial property in Navi Mumbai

- Using one generic commercial rate for an entire node

- Comparing shop pricing with office pricing

- Negotiating only on Ready Reckoner

- Believing portal asking prices are executed market truth

- Calculating yield on gross rent instead of net income

- Ignoring NMMC tax burden on commercial assets

- Pricing by super built-up area without standardizing usable space

- Treating CIDCO transfer issues like paperwork noise instead of valuation damage

Conclusion

To value commercial property in Navi Mumbai correctly, stop looking for one neat rate. The better method is to build a valuation band from the bottom up: current Ready Reckoner reference, real local comparables, true income, building usability, and legal-transfer friction.

That approach is slower than asking a broker for a one-line rate, but it is also how buyers avoid paying premium prices for weak assets. In Navi Mumbai especially, a commercial property is worth what it can legally transfer, practically operate, and realistically earn. Everything else is sales language.

For any serious deal, use this article as a working framework, then get your lawyer and document professional to verify the title chain, transfer status, approvals, and dues before token money moves.

FAQs

Frequently Asked Questions